Summary

This report explores how Canada’s wealthiest billionaires have continued to become even wealthier through the pandemic, and considers what the Canadian government can do to tax extreme wealth and address our disturbing and growing levels of inequality.

While multiple factors have contributed to growing extreme levels of inequality at the very top, decades of regressive tax measures, particularly lower rates of tax on business and capital, have played the largest role, with the wealth of the top billionaires overwhelmingly held in corporate interests. Just as regressive tax policies have fuelled excessive inequality, we need progressive tax measures to reverse it.

In the recent throne speech, the federal Liberal government promised that it would “identify additional ways to tax extreme wealth inequality.” This report recommends a number of ways for the federal government to do this, with estimates of how much revenue the measures would raise, including new estimates of how much a wealth tax could generate at different rates.

Report

KEY FINDINGS

- Over the past decade, only the top 1% wealthiest Canadians—those with over $6 million in net wealth—have increased their share of total wealth in Canada, while the share of all other groups has declined.

- The number and wealth of Canada’s billionaires has more than doubled over the past decade.

- During the pandemic, the wealth of Canada’s top 44 billionaires has surged by more than $50 billion—by 28%—over the six months from early April to October, while millions of ordinary Canadians and small businesses have struggled to stay afloat. [1]

- 43 of Canada’s top 44 billionaires increased or maintained their wealth over these six months.

- In a number of cases, the same billionaires who profited during the pandemic also moved quickly to cut pandemic pay for their low-paid workers, who continue to expose themselves to significant risks at work.

- The federal government could generate significant revenues by taxing extreme wealth, as the Trudeau government promised to do in the throne speech. This report uses data recently released by the Parliamentary Budget Officer to show how a modestly graduated annual wealth tax on wealth of over $10 million could generate $20 billion annually, and how other progressive tax measures could generate many billions more to help pay for the costs of the crisis and to fund a more inclusive recovery.

- Wealth is highly unequally distributed across gender and racial lines. All Canada’s top 44 billionaires are male and the vast majority are white, while those most negatively affected by the pandemic are predominantly poor, female and/or from communities of colour. Taxing extreme wealth to fund social programs would help to reduce gender and racial inequalities.

The COVID-19 crisis has further revealed that we are not all “in this together.” The federal government now has a critical opportunity and responsibility to reverse these growing extreme inequalities and ensure that the recovery is equitable and includes all Canadians.

It's Time To Tax Extreme Wealth Inequality

Wealth inequality around the world and in Canada had already become extreme before the COVID-19 pandemic. Globally, the top 26 billionaires had as much wealth in 2018 as the bottom 50% of the world’s population [2]. Canadians do not tend to see themselves in these stories of stark inequality. However, our own billionaires club has been gaining wealth at similar rates.

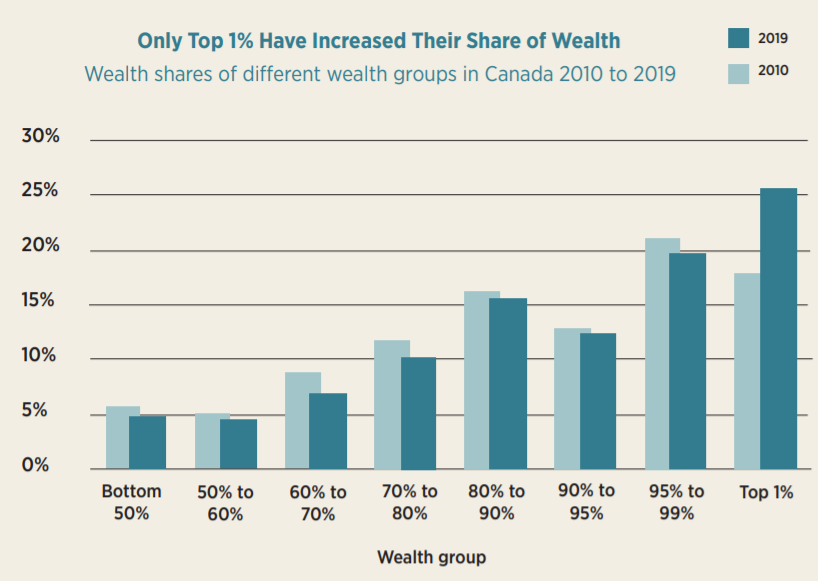

Canada’s club of 100 billionaires now has as much wealth as the 12 million poorest Canadians [3]. The wealthiest 10% hold over twice as much as the poorest 80%, and the top 1% now have almost 26% of all wealth in Canada, up from 17.9% a decade ago [4].

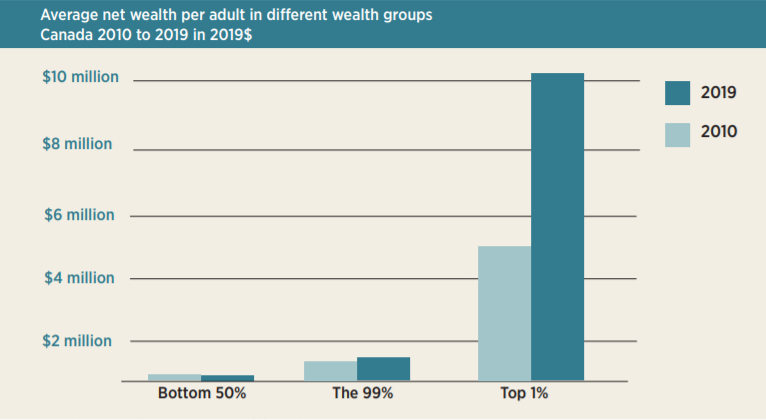

Meanwhile, the share of the poorest 50% has declined from 5.9% to just 4.7% [5]. In fact, figures from Credit Suisse show that only Canada’s top 1% increased their share of total wealth between 2010 and 2019. The share of all other groups declined or remained the same. (See chart on page 7).

After adjusting for inflation, the average wealth of each adult member of Canada’s top 1% more than doubled from $4.9 million in 2010 to just over $10 million in 2019, by 8.4% annually. Meanwhile the average wealth of the other 99% of Canadians—largely represented by the value of their homes and pensions—increased by just 3% per year, and the average wealth of the bottom 50% of Canadians increased by only 1.7% annually from $32,043 in 2010 to $37,403 in 2019.

Calculated using Credit Suisse Global Wealth Databook, 2020 and 2019

Calculated using Credit Suisse Global Wealth Databook, 2020 and 2019

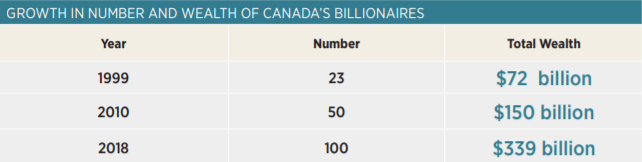

There’s a convenient fiction perpetuated that Canada hasn’t experienced the great extreme inequalities of wealth at the top end that the United States has. It’s true that our wealthiest don’t have fortunes at the same level as Jeff Bezos or Warren Buffett, but the number of Canadian billionaires has increased at a far faster rate than the number of American billionaires and their total wealth has also increased at a much faster rate.

The number of Canadian billionaires more than quadrupled in the past two decades, from 23 in 1999 to at least 100 in 2018, and their combined wealth has increased almost five times over.

Source: Canadian Business Magazine, Canada’s Richest 100 Canadians

Canada’s wealth gap did not grow this big overnight. Decades of regressive tax measures have enabled billionaires to accumulate more and more wealth while draining billions in government revenues for programs to help those at the bottom and middle, such as affordable housing and childcare.

When considering all taxes, comprehensive studies have shown the top 1% pays a lower overall rate of tax on their income than all other income groups, including the poorest [6]. Given that wealth is even more concentrated at the top, these tax rates as a share of wealth are even more favourable to the rich, and worse for the vast majority.

The wealthiest can shelter their assets and investments at low rates of tax for many years.

Most of the assets of the wealthiest are held in corporate shares or financial investments, which can increase in value at low rates of tax for many years until they are sold or ‘realized.’ Even then, only 50% of investment and capital gains are taxed, with many opportunities for further exemptions and sheltering. Meanwhile workers are generally taxed on the full value of their employment income before they receive their paychecks.

Our tax system overwhelmingly favours the wealthiest citizens who have money to spare, and to invest.

Many Canadian billionaires also exert significant political influence on legislation and policies that work in their favour while benefiting from lucrative government contracts and subsidies.

Over the past two decades, the race to the bottom in corporate tax rates has further widened the wealth gap. We were told that corporate tax cuts would stimulate the economy and create jobs, but instead corporations have amassed hundreds of billions in surpluses, engaged in record share buybacks, dividend payments, and in mergers and acquisitions, leading to even greater corporate concentration [7].

Increased corporate concentration and monopolization is intimately linked to greater inequalities of income and wealth, especially at the very top end. By far the largest assets of the wealthiest individuals are held in their businesses and corporate shares. As the businesses become larger, more dominant, and more valuable, so does the wealth of their major owners.

The absence of wealth, estate, or inheritance taxes in Canada has allowed billionaires to keep their wealth in the family as it is passed down through generations. The greater ease of avoiding taxes through tax havens has also enabled rich individuals and large corporations to hoard more of their assets offshore. At the end of 2019, Canadian corporations held a new record of over $380 billion in Canada’s top ten offshore tax havens [8].

Increased corporate and wealth concentration hurts the economy by stifling business competition, increasing economic instability and preventing Canada’s middle class—and those working hard to join it—from thriving. Inequality also has far-reaching social costs, such as higher levels of mental illness, addiction, school bullying, and crime rates [9].

Many billionaires and their businesses have profited from unfair practices that have a harmful effect on society and the economy, such as anti-competitive behavior, hiking prices on consumers, tax dodging and tax haven use, union-busting and exploitative labour practices.

It has taken some time, but economic authorities including the IMF [10], OECD [11], World Bank [12] and the Bank of Canada [13] now acknowledge that growing inequalities have been bad for the economy. Greater concentrations of wealth have also led to greater concentrations of power and political influence. As the OECD has remarked, “wealth begets wealth.”

Inequality was already hurting Canadians before COVID-19, but the pandemic has made the situation even worse. Millions lost work and many more continue to struggle with the health, social and economic challenges brought on by the crisis. It’s a different story for Canada’s richest, whose wealth flourished in the same period.

Canada’s billionaires and wealthiest are overwhelmingly male and white. Many of Canada’s tax loopholes reinforce gender as well as wealth disparities by disproportionately benefiting men while draining billions in government revenues for programs that help women, such as accessible childcare [14]. Revenue from progressive tax measures on these billionaires could be used to pay for a national child care program. This would be a very powerful way to reduce both social and gender inequalities.

While some argue that many of the wealthiest already redistribute their wealth through philanthropy and we often see media stories about their multi-million dollar donations, in reality most of the wealthy have only given away a small fraction of their wealth, even with generous incentives. A study by TaxCOOP found Canada’s top five billionaires donated a mere 0.09% of their wealth during the pandemic while their personal fortunes grew by more than 9% [15].

CANADA’S TOP BILLIONAIRES

Source: Forbes Annual and Real-time billionaire lists, converted to Canadian dollars at a rate of C$1.00 = US$0.75.

HOW CAN WE REDUCE EXTREME WEALTH INEQUALITY THROUGH TAXATION?

In a time of crisis, when so many households are struggling, it is only fair that the richest individuals and most profitable corporations pay their fair share in taxes. In its recent throne speech, the federal Liberals promised they would “identify additional ways to tax extreme wealth inequality.” Here are some of the best ways to do that:

1. Wealth tax:

A wealth tax would be a powerful way to reduce extreme inequalities that have developed in recent years while also raising significant revenues. U.S. Senators Bernie Sanders and Elizabeth Warren both proposed progressive wealth taxes at rates of up to 6% and 8% on billionaires in their bids to become the presidential candidate for the Democratic Party. Jagmeet Singh and Canada’s federal NDP have proposed a more modest wealth tax of 1% on fortunes of over $20 million. This has garnered a lot of public support. Recent polling found that 75% of Canadians of all ages and across the political spectrum were in favour of a wealth tax of 1% to 2% on the very rich [16] to help recover from COVID-19.

Some question how much a wealth tax could raise in revenue, but the Parliamentary Budget Officer (PBO) estimated that a 1% wealth tax on fortunes of over $20 million would raise $5.6 billion in the first year and $70 billion over a decade [17]. The PBO’s release of background data that it used in these calculations in its High Net-Worth Family Database allows others to estimate revenues from a wealth tax for different rates and under different assumptions. Using these data, a graduated wealth tax at a rate of 1% on wealth over $10 million, 2% on wealth over $100 million and 3% on wealth over $1 billion would generate close to $20 billion annually (see Appendix A).

2. Inheritance tax:

Many of Canada’s wealthiest billionaires were born into extremely rich families, demonstrating how wealth is passed on from one generation to the next. Canada is the only G7 country without an estate, inheritance or wealth tax. This has allowed our wealthiest family dynasties to accrue excessive amounts of wealth passed down through generations, deepening the wealth and class divide. While low and average-earning Canadians face no shortage of challenges, it’s a different picture for billionaires born into wealth. They benefit enormously from higher levels of education and elite connections into well-paying jobs, private family trusts and ultimately their largely untaxed inheritance of wealth.

Even the U.S. levies taxes on high-wealth estates that are passed on as inheritances, but Canada eliminated its federal inheritance tax decades ago. While there’s a lot of uncertainty about how much an estate or inheritance tax would generate, conservative estimates are that a 45% tax on the inheritance/ estates of over $5 million—similar to the US—would generate at least $2 billion annually [18].

3. Tax investment income like any other income and remove tax loopholes:

Ordinary working Canadians are taxed on the income they earn. But for billionaires, much of the income they generate avoids taxation altogether. Lower rates of tax on savings, investment income, capital gains, stock options and business income than rates on income from labour allow those with the means to accumulate more and more wealth. This makes it easier for the wealthy to make more money, but much harder for average working Canadians—after expenses such as housing, groceries, uncovered medical costs, and childcare—to get ahead.

The federal government should eliminate or reduce some of the most regressive and expensive tax loopholes such as the:

Preferential tax rates on capital gains and investments: The reduced tax rate on capital gains on personal, corporate and trust incomes is one of the federal government’s most expensive loopholes. Finance Canada estimates that it lowers revenues by close to $22 billion annually [19].

Stock option deduction: This billion-dollar loophole is especially bad for equality and the economy, with more than 90% of its benefits going to the top 1%20. The federal government promised, then delayed plans to restrict this tax loophole in 2019. Now more than ever, it should close it entirely, which would save federal and provincial governments about $1 billion annually.

Corporate dividend tax credit: More than two-thirds of this $5-billion tax break goes to men, with less than a third going to women [21]. It is supposed to compensate shareholders for the corporate taxes that businesses pay, but many businesses don’t pay any corporate income taxes and most pay tax at a lower rate than the dividend tax credit provides shareholders.

4. Tax on foundation assets:

The wealthy also benefit from other tax perks such as the use of foundations and charities to lower their overall tax bill [22]. Half of the top 10 billionaires have foundations in their family name. Although charitable organizations perform valuable work, they are a poor replacement for adequately taxing the rich and can reduce tax revenues by more than they distribute [23]. Foundations and charitable giving enable the very rich to direct tax dollars toward the causes they choose to support. Foundation endowments grow tax-free as well. It would be preferable to redistribute tax revenues to government public programs and services where they are needed.

5. Excess profits tax:

As more small and medium-sized businesses collapse under COVID-19, a handful of larger corporations are increasing their market share and benefiting from soaring profits. Just as it did during WWI and WWII, the federal government should introduce an excess profits tax on large corporations that have significantly profited from the pandemic. During these periods, the excess profits tax, which was at rates of up to 80% on above average profits, raised more revenue than the general corporate income tax—and that was at a time when the corporate tax rate was higher than it is now.

6. Stop the race to the bottom of corporate tax cuts:

The actual effective rate that corporations pay on their taxable income has been cut by more than half, from 40% 25 years ago to less than 20% in recent years [24]. Canadians were promised that corporate tax cuts would lead to more investment, economic growth and jobs, but instead they’ve resulted in cash hoarding by corporations, skyrocketing executive pay, record share buybacks and dividend payments for those at the top – deepening the wealth gap. Even mainstream economists are now warning that corporate tax cuts are resulting in increased corporate concentration, weakened business competition, and record levels of inequality [25]. Restoring the federal general corporate tax rate from 15% to 18% would generate over $5 billion annually, according to the PBO [26].

7. Tackle tax havens:

Tax havens cost Canadian governments at least $10 billion a year in lower revenues, and up to $25 billion, according to calculations by the Parliamentary Budget Officer. They also worsen inequality by allowing the wealthy to hide and hoard their assets at the expense of poorer countries and government funding. Corporations have increased their assets in Canada’s top tax havens by more than 135% over the past decade [27]. The federal government should take steps to eliminate this abuse by supporting fundamental reforms to international corporate tax rules, ending double non-taxation agreements with tax havens, requiring large corporations to publicly report taxes paid in each country, and treating multinational enterprises as single entities for tax purposes so they can’t avoid taxes by shuffling profits through a string of subsidiaries.

8. Reform tax rules around excessive executive compensation:

Rising compensation and tax perks for corporate executives have eroded equality. A 2020 report by the Canadian Centre for Policy Alternatives found Canadian CEO pay is now 227 times greater than average worker pay—a new and troubling record [28]. To make matters worse, corporations can deduct the cost of executive compensation for tax purposes. Canada should follow the U.S., which caps the amount that corporations can deduct for tax purposes at $1 million per executive [29].

The federal government could also curb excessive pay by applying higher rates of corporate income tax to large companies that pay their executives more than 50 times what they pay their median worker.

CONCLUSIONS

Back in January, before the COVID-19 pandemic really took hold, the head of the International Monetary Fund cautioned that inequality had become one of the most “vexing challenges in the global economy [30].” The global pandemic has worsened it.

Over the past several months of the pandemic, we have seen tragic examples of how deep these chasms of inequality are, with the most vulnerable individuals and communities suffering the most. COVID-19 has also shown how jurisdictions that invested early in the resources to protect all its citizens fared better than those that downplayed risks and turned to austerity in a crisis.

As the pandemic continues, individuals already on the edge are at risk of losing even more while many smaller businesses, already squeezed out by larger corporations, will be forced to shut their doors under the ongoing hardship. Already, we are witnessing a survival -- not of the fittest -- but of the most fortunate.

Canada needs to significantly invest in programs to restore equality and help Canadians, including better income supports, safer long-term care for seniors and those with disabilities, pharmacare, affordable childcare, safe schools, and a Just Transition to a greener economy. Now is the time for the government to introduce a range of progressive tax changes to make these programs a reality.

What we cannot afford is to ignore the widening wealth gap that has weakened our economy and collective well-being. With so many households struggling, we must finally take steps to reverse the growing concentration of extreme wealth and power at the top. Progressive tax reforms are needed to rebuild a more equitable and prosperous economy for all Canadians.

APPENDIX

Wealth Tax Revenue Potential While there is a lot of popular support for a tax on extreme wealth, there’s less knowledge, and some debate, about how much revenue a wealth tax could credibly generate in Canada, and how it could affect inequality.

Fortunately, to estimate revenues for the NDP’s wealth tax proposal, Canada’s Parliamentary Budget Officer developed a High-net-worth Family Database and published key figures from it earlier this year. This allows others to estimate potential revenues from a wealth tax at different rates for different thresholds, using different assumptions about how such a tax would affect behaviour.

These data show that:

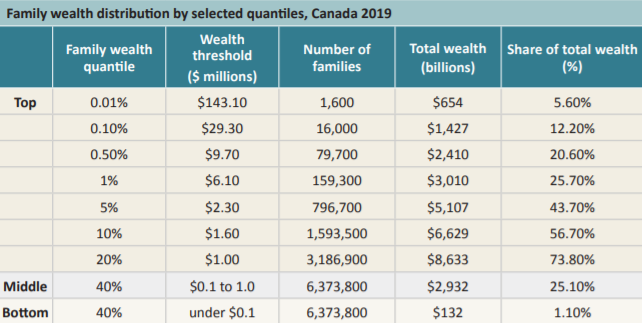

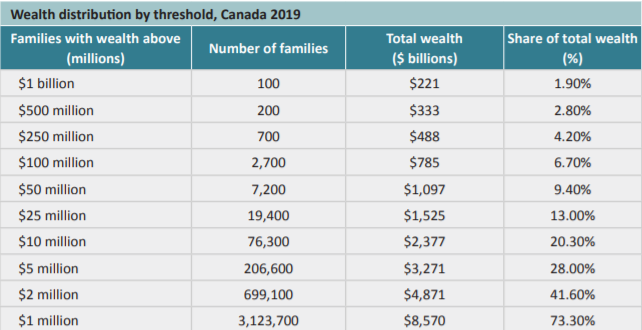

- The top 10% of Canadian families--those with net wealth above $1.6 million—own 56.7% of total family wealth

- The top 1%--those with net wealth of $6.1 million and up—have 25.7% of all wealth

- The top 0.1%--the 29,300 families with net wealth over $29.3 million—have 12.2% of all wealth.

Wealth is highly skewed to the top. The 2,700 families with fortunes of over $100 million represent less than 0.02% of all families in Canada but they have $785 billion, equal to 6.7% of all wealth in Canada. Canada’s approximately 100 billionaire families represent just 0.0006% of all families in Canada but they own about 2% of all wealth.

In calculating the net revenues that would be generated by a tax on wealth above a certain amount, a few adjustments need to be made to these figures.

First, the net wealth figure needs to be adjusted for tax avoidance/evasion and other behavioural factors. The PBO reduced these amounts by 35% on the basis of estimates from the Internal Revenue Service, but that is based on experience with the U.S. estate tax, which is at rates of 45% and less relevant for an annual wealth tax. There are more appropriate estimates that can be drawn from the experience of countries with actual wealth taxes. Economists Emmanuel Saez and Gabriel Zucman take the average of different studies—including Switzerland where wealth is self-reported—to come up with a 15% reduction behavioural response/ tax avoidance/evasion to a 2% wealth tax. We are more cautious in our estimates and use a 20% reduction for a wealth tax of 2%, and 10% for a wealth tax of 1%.

Secondly, wealth for each family below the wealth tax thresholds—e.g. of $20 million each—must be excluded.

Thirdly, costs to administer, collect and enforce the wealth tax can also be excluded to calculate the net revenues. The PBO used a 2% administrative cost, based on France’s wealth tax, although the administrative costs associated with a tax that applied to just a few super-wealthy would likely be less in Canada.

Source: PBO High-net-worth Family Database

With these data and assumptions, calculating the revenues from a wealth tax is straightforward. For example, the 76,300 families with net wealth over $10 million have total wealth estimated at $2.37 trillion. Excluding their wealth below $10 million (as that would not be taxed) reduces this amount by $763 billion to a tax base of $1.614 trillion. Assuming a 10% behavioural/ avoidance factor for each 1% wealth tax rate reduces the tax base further to $1.452 trillion. Therefore, a 1% tax on net family wealth of over $10 million would generate $14.52 billion annually. Subtracting 2% administrative costs would reduce this amount to $14.24 billion annually.

Increasing the wealth tax rate for those with even larger fortunes would be more progressive and generate greater revenues. For instance, increasing the rate to 2% for the 2,700 families with wealth above $100 million would generate an additional $4.54 billion for total revenue of $18.8 billion annually. Adding another 1% so Canada’s super rich are taxed at 3% on their wealth over $1 billion would generate an additional net amount of $1 billion annually, for a total of close to $20 billion annually.

In comparison, a wealth tax in Canada along the lines proposed by U.S. Senator Elizabeth Warren, at a rate of 2% on wealth of over $50 million and an additional 4% (for 6% total) on the net wealth of over $1 billion for billionaires would raise approximately $14 billion annually. A tax on extreme wealth as proposed by U.S. Senator Bernie Sanders, with a rate starting at 1% for wealth over $32 million, 2% on net worth above $50 million, and rising incrementally to 5% on wealth over $1 billion and up to 8% on wealth over $10 billion would generate revenues of about $22 billion annually in Canada.

ENDNOTES

[1] Impact of COVID-19 on small businesses in Canada, Statistics Canada, May 11, 2020

[2] World’s 26 richest people own as much as poorest 50%, says Oxfam, the Guardian, January 21, 2019

[3] Canadian dynasties richer than ever as wealth gap continues to widen: study, Canadian Centre for Policy Alternatives, July 31, 2018

[4] Global Wealth Databook 2010, Global Wealth Databook 2019 (Zurich: Credit Suisse, 2010 and 2019), Jim Davies, Anthony Shorrocks and Rodrigo Lluberas. The latest estimates from Credit Suisse of a 25.7% share for Canada’s top 1% in 2019 are very close to the estimates developed by the PBO, which are that the top 1% had a 25.6% share of total wealth in Canada in 2016.

[5] Estimating the top tail of the family wealth distribution in Canada, the Office of the Parliamentary Budget Officer, June 17, 2020, p.1

[6] Eroding Tax Fairness, Tax Incidence in Canada, 1990-2005, Canadian Centre for Policy Alternatives, Marc Lee, November 2007, p.3

[7] Corporate Income Tax Freedom Day, Canadians for Tax Fairness, Toby Sanger, January 7, 2020, p.8

[8] Corporate Canada top 12 tax havens report, Canadians for Tax Fairness, July 22, 2020, p.1

[9] The Spirit Level: Why Equality is Better for Everyone, Richard Wilkinson and Kate Pickett, Penguin, 2010.

[10] The IMF warns about rising regional inequality, NPR, October 22, 2019

[11] Inequality, OECD website

[12] Coronavirus: World bank warns 60m at risk of extreme poverty, May 20, 2020

[13] Uneven rebound poses risk for entire economy, Bank of Canada governor says, Canadian Press, Sept 10, 2020

[14] Are Canada’s tax loopholes sexist? Canadian Centre for Policy Alternatives, David Macdonald, March 7, 2019

[15] Top richest Canadian billionaires During the Canadian COVID-19 Lockdown, TaxCOOP, May 25, 2020

[16] Canadians want a recovery that is ambitious, fair and makes the country more self-sufficient, Abacus Data, May 22, 2020

[17] Cost Estimate of Election Campaign Proposal, Parliamentary Budget Officer, September 10, 2019

[18] Platform for Tax Fairness, Canadians for Tax Fairness, p.6

[19] Report on Federal tax expenditures 2020, Finance Canada, February 2020.

[20] Are Canada’s tax loopholes sexist? p.16

[21] Are Canada’s tax loopholes sexist? p.9

[22] COVID-19 has exposed the limits of philanthropy, the Conversation, August 13, 2020

[23] The tax regime for private charitable foundations –a threat to democracy and an infringement on government finances. Brief (summary) submitted to the House of Commons Standing Committee on Finance, Brigitte Alepin, October 21, 2014

[24] Corporate Income Tax Freedom Day, p.2

[25] US Business Investment: Rising market power mutes tax cut impact, IMF Blog, August 8, 2019

[26] Ready Reckoner revenue estimator, Parliamentary Budget Officer, accessed September 2020.

[27] Corporate Canada Top Tax Havens Report, p. 1

[28] High CEO pay shatters previous records, now 227 times more than average worker pay, Canadian Centre for Policy Alternatives, January 2, 2020

[29] New limit on $1 million executive pay deductions under the 2017 tax law, Inc.com, Barbara Weltman, Feb 27, 2019

[30] IMF boss says to raise taxes on the rich to tackle inequality, the Guardian, Jan 7, 2020

Acknowledgements: The authors would like to thank Dan Hoyer and Adam Saifer for their contributions and comments, and Mary Neumann and other funders for their financial support. The opinions in this report and any errors or omissions should be attributed to Canadians for Tax Fairness, not its members or supporters.