Report

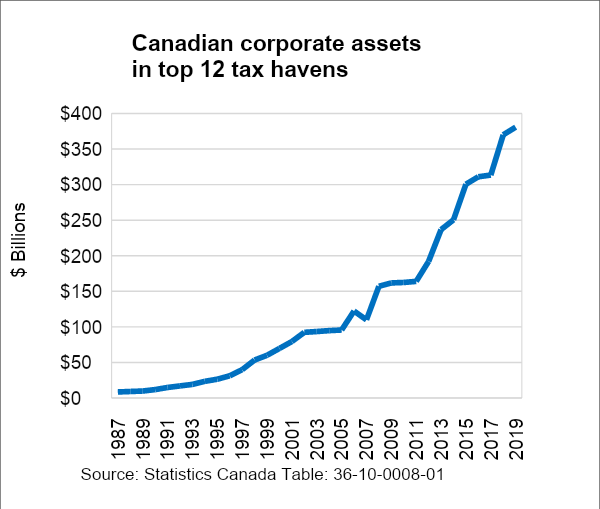

The total amount Canadian corporations reported in their top 12 tax havens soared to a record high of $381 billion in 2019. Despite political pressure following international scandals such as the Panama Papers and repeated promises from governments to get tough on tax havens, analysis of Statistics Canada’s latest foreign direct investment data shows that use of tax havens by Canadian corporations keeps on rising.

The assets Canadian corporations report in Canada’s top 12 tax havens has increased by 634% since 1999, rising as a share of total Canadian corporate foreign direct investment (FDI) abroad from 11% in 1989 to over 27% today.

Half of all Canadian FDI abroad is through the finance, insurance and management of companies sectors. These don’t represent physical productive investments, but instead are largely paper investments through shell companies to avoid taxes. This is reflected in the number of people Canadian multinationals employ in these countries in relation to their assets. Canadian multinationals have on average 360 employees per $1 billion in assets worldwide, but in tax havens they employ far less: as low as one or two in Bermuda and the British Virgin Islands (see below).

A recent study by the International Monetary Fund (IMF) found that $15 trillion or 38% of total global FDI are “phantom investments” through shell companies. Phantom investments have far outpaced the growth of genuine investments.

Luxembourg remains the top tax haven of choice for Canadian corporations (see table below), with $101 billion of “investments” reported there, followed by Bermuda ($64 billion), Barbados ($50 billion), Cayman Islands ($43) Netherlands ($36) and Bahamas ($26 billion). While the United States and the United Kingdom are the top two destinations for overall Canadian direct investment abroad, the rest of the top of the list is dominated by these tax havens: six of the 10 top destinations for overall Canadian FDI abroad are tax havens. Far more Canadian investment is located in any of these top six tax havens than in China, Germany, Brazil, France or Japan.

New to the top-12 list in 2019 is Malta, the Mediterranean island state with one of the lowest tax rates in the European Union. The otherwise lesser-known tax haven hit the headlines in 2017 after an investigative journalist who had reported on the Panama Papers was murdered in a car bomb. The Maltese businessman eventually charged with Daphne Galizia’s murder has ties to businesses in tax havens and to the country’s former prime minister, who was forced to resign. This controversy did not dissuade Canadian corporations, which increased their assets in Malta by 52% in 2019.

CANADIAN CORPORATE INVESTMENTS IN TOP 12 TAX HAVENS 2018-2019

And associated jobs per $1 billion invested

|

Country |

2018 |

2019 |

Change |

Jobs /$1B |

|

Luxembourg |

$102.5 |

$ 101.2 |

-1.3% |

31.3 |

|

Bermuda |

$58.1 |

$ 63.5 |

9.3% |

1.7 |

|

Barbados |

$50.2 |

$ 49.8 |

-0.9% |

38.9 |

|

Cayman Islands |

$41.8 |

$ 42.7 |

2.1% |

5.5 |

|

Netherlands |

$36.5 |

$ 35.9 |

-1.6% |

88.7 |

|

Bahamas |

$26.3 |

$ 26.3 |

0.0% |

70.5 |

|

Switzerland |

$9.7 |

$ 16.0 |

65.6% |

393.7 |

|

Hong Kong |

$10.8 |

$ 11.7 |

8.7% |

178.8 |

|

British Virgin Islands |

$12.2 |

$ 10.5 |

-13.7% |

1.1 |

|

Ireland |

$9.6 |

$ 9.5 |

-0.8% |

262.3 |

|

Singapore |

$9.5 |

$ 9.3 |

-2.2% |

161.8 |

|

Malta |

$2.9 |

$ 4.3 |

51.6% |

153.7 |

|

Total top 12 tax havens |

$370.0 |

$ 380.8 |

2.9% |

78.7 |

|

Total Cdn FDI abroad |

$1,357 |

$1,391 |

2.5% |

360.9 |

|

Top 12 tax haven share |

27.3% |

27.4% |

|

|

*Figures are underestimates of full extent of Canadian corporate money in tax havens (see Endnotes for details). Source: Statistics Canada Tables 36-10-0008-01 and 36-10-4070-01.

Large multinational corporations are much more likely to take advantage of gaps in international tax rules and use tax havens to give them a tax advantage over smaller and medium-sized enterprises. This has increased corporate concentration, reducing competitiveness, equality and economic growth. As our 2017 report Bay Street and Tax Havens revealed, over 90% of the large corporations represented on the TSX60 Index have at least one subsidiary in a tax haven. Increased corporate concentration has also led to greater wealth inequalities, as the prime beneficiaries are the super wealthy owners of these corporations.

While they only revealed the tip of the iceberg, the Panama Papers and other leaks illustrated how widely tax havens are used by money launderers, corrupt officials, and other criminals to hide their money and avoid taxes. These leaks also exposed how many prominent politicians, ministers and heads of state—including the Queen of England and former Prime Ministers—have used tax havens. This may help explain why there has been little progress to address the problem.

Both the IMF and the Tax Justice Network estimate that international tax dodging by corporations costs governments around the world more than US $500 billion every year. The loss of revenue to tax havens is especially acute for people in poorer countries. Their revenue losses are relatively higher and their needs to address poverty and health care, particularly in the wake of the COVID-19 pandemic, are even greater.

CORPORATE CANADA’S FAVOURITE TAX HAVENS

LUXEMBOURG: The Grand Duchy of Luxembourg is the top destination for Canadian corporate assets because it exempts certain forms of income and payments from tax. Canadian corporations that use Luxembourg to avoid tax include Husky Energy (owned by Hong Kong based multi-billionaire ) and Cargill Inc (which made headlines this spring after a massive COVID-19 outbreak shed light on unsafe labour and safety practices at its slaughterhouses). Others include steel giant ArcelorMittal and the companies that own the Golden Ears Bridge and Stoney Trail public-private partnerships.

BERMUDA: This British territory, which now guarantees multinationals that no tax will be levied on them for at least 15 years, has been home to a number of notable Canadian corporations including parts of the Irving Empire, Canada Steamship Lines, owned by former Prime Minister Paul Martin, major parts of the Brookfield real estate and infrastructure conglomerate, Accenture Consulting, Staples Canada, Pepsi, and many others.

BARBADOS: Barbados has been an attractive destination for Canadian corporations since Canada signed a treaty with the Caribbean country in 1980. This allowed assets and income to be returned to Canada tax free after being subject to taxes of just 0.25% to 2.5% in Barbados. Companies such as Loblaw and Capital Sports and Entertainment, which owns the Ottawa Senators, have used Barbados to avoid taxes in Canada. The Caribbean tax haven recently increased its low tax rate for multinationals from 0.25% to 1% in 2019, which could explain why Canadian corporate assets held there decreased slightly last year.

CAYMAN ISLANDS: The Cayman Islands are a well-known tax haven because they have no corporate, payroll, capital gains, withholding or other direct taxes on corporations. It is especially popular with finance, technology and mining firms including Brookfield, Onex, Seagate, Goldcorp, Corel, Herbalife and many others. The Paradise papers revealed the billionaire Bronfman-controlled Claridge had a $60 million trust located there.

NETHERLANDS: Hundreds of Canadian corporations have affiliated companies resident or controlled in the Netherlands: more than any other jurisdiction after the US and UK. It functions as an intermediary tax haven—known for the “Dutch sandwich”—with no tax on business income, capital gains, dividends and interest from foreign subsidiaries. It is considered one of the most harmful tax havens in terms of revenue losses.

BAHAMAS: With zero corporate income tax, the Bahamas has seen an 80% increase in Canadian corporate funds over the past decade. Canadian fashion designer Peter Nygard, who has made headlines for abusive labour practices, tax evasion and most recently, allegations of rape and sex trafficking, has his empire located there.

SWITZERLAND: Switzerland has a rich history as one of the oldest tax havens available to Canadian and global elite. To this day, it remains a refuge for hidden wealth. Saskatchewan-based uranium mining giant Cameco has used Switzerland to avoid more than $2 billion in Canadian taxes.

ACTION NEEDED

Corporate tax dodging through tax havens costs Canadian governments at least $10 billion and up to $25 billion annually, according to the Parliamentary Budget Office. They also overwhelmingly benefit larger multinational corporations and the wealthy, leading to greater corporate concentration and inequalities—all at the expense of ordinary Canadians and small and medium-sized domestic businesses. The COVID-19 pandemic has further exposed these inequalities and underlined the need for increased revenues to pay for the costs of the crisis and to rebuild our economy. A top priority should be addressing the scourge of tax havens and reforming international tax rules that allow the largest corporations and the wealthiest to avoid paying their fair share of taxes.

The federal government should take action in three different areas:

1) Increase transparency. While there has been progress in exchanging tax information between jurisdictions and reporting by corporations, much more needs to be done. Canada, in particular, has weak corporate transparency rules. This has made us a destination for shell corporations, money laundering and other corporate criminal activities. We also have a poor record in exchanging corporate tax information with other countries. We need to increase transparency by both establishing a national public registry of the beneficial or real owners of companies, and requiring multinational corporations to publish summary financial and tax accounts on a country-by-country basis.

2) Strengthen rules to prevent tax dodging. The biggest problem is that most corporate tax dodging and tax haven use is perfectly legal—and that our tax rules are fundamentally out of date, as the former head of the IMF has said. We need reforms to:

- Treat multinational enterprises as single entities for tax purposes so they can’t avoid taxes through subsidiaries or affiliated companies;

- Apportion profits of multinational corporations between countries using real economic factors—such as sales and employment, just as we do between provinces—so companies can’t avoid taxes through international transfer pricing;

- Support the introduction of a minimum international corporate tax rate and end Canada’s double non-taxation agreements with tax havens so corporations and wealthy individuals pay their fair share of tax;

- Introduce a digital services tax on the profits and revenues of e-commerce giants such as Facebook and Google;

- Strengthen anti-tax avoidance rules and eliminate loopholes—such as through excessive payments for interest deductibility and intellectual property royalties—that large corporations routinely use to avoid taxes.

3) Strengthen enforcement. Greater transparency and stronger regulations will only go so far without the muscle to enforce them. Canada should invest additional resources in the Canada Revenue Agency and prosecution services to investigate and prosecute corporate offshore tax dodging. The federal government also needs to increase penalties against corporations that evade taxes and the professional and accounting firms that promote tax evasion schemes.

ENDNOTES

The figures in this Report's chart above, for Canadian corporate assets in tax havens, are underestimates. They don’t include funds located in prominent sub-national tax haven jurisdictions, including the State of Delaware, South Dakota or the UK-Crown dependencies of Jersey, Guernsey or the Isle of Man, or in other countries considered tax havens in other lists.* They only reflect the funds that Canadian corporations officially report in these 12 tax havens. Many more billions are no doubt hidden in these or other tax havens by corporations and wealthy individuals.

*NOTE: Lists of countries considered tax havens vary considerably, with official lists frequently subjected to political pressure. The list we use is from the independent U.S. Congressional Research Service. It also doesn’t include a number of countries generally considered tax havens, including Mauritius, Gibraltar, or Turks and Caicos.