Résumé

C4TF proposes policy changes in four different areas to:

- Ensure corporations and the wealthy pay their fair share by closing regressive tax loopholes and making taxes more progressive

- Tackle international tax evasion, avoidance and tax havens

- Improve corporate transparency

- Combat climate change and support sustainable development

Rapport

Canada needs substantive progressive tax reform, not only to generate additional revenues to pay for public services, but also to reverse growing inequalities and to strengthen our economy.

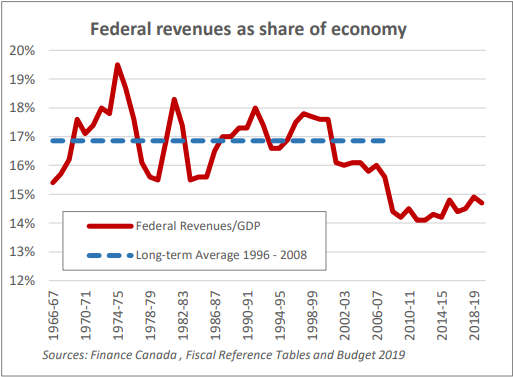

- We need higher revenues to fund the expanded public services and investments required to improve the quality of life for all and strengthen our economy. Federal government revenues are now down to a 14.7 percent share of our economy, more than two full percentage points below their long-term average of 16.9 percent. If federal revenues were at their longer-term average, the federal government would raise an additional $50 billion in revenues annually. This would be enough to properly fund initiatives such as child care, pharmacare, affordable housing, and environmental measures that are so important for Canadian families, our economy, and our future.

- Tax policy should help to reduce inequality, not increase it. The tax cuts and loopholes introduced in the past few decades have resulted in an unfair tax system that exacerbates inequality. The largest tax cuts in the past two decades have been for the wealthy and corporations, with the federal corporate tax rate cut in half over the past two decades. The top one percent of Canadians pays a lower overall effective rate of tax than all other income groups, including the poorest ten percent. And because inequality is gendered and racialized, these regressive tax changes have been relatively more detrimental to women, racialized and Indigenous Canadians. Reducing inequality would help boost domestic consumer demand, support Canadian businesses and create more jobs. This plan shows how the federal government could raise many billions more in revenues by reversing tax cuts on the wealthy and corporations so they pay their fair share and so the federal government can fund important public services.

- Tax reform to strengthen our economy. Too often our tax laws and loopholes allow large corporations to get off with paying little or no tax. Large foreign mega-corporations are especially adept at using loopholes, subsidiaries, tax havens and fighting tax authorities in court to reduce their taxes. This hurts small and medium-sized Canadian firms, and is also bad for the economy because it leads to greater corporate concentration and less competition. We need to eliminate preferences and advantages that benefit large corporations at the expense of everyone else.

- Applying taxes and removing subsidies from negative environmental, social and economic activities and providing incentives, including tax credits for positive ones. Our tax and fiscal system has a role to play in putting a price on pollution and creating disincentives and incentives on different activities to reflect their broader social impacts. However, the effectiveness of the price system on its own is limited and needs to be combined with other complementary measures and support for those negatively affected by these changes.

The fair tax plan we outline below could generate over $40 billion annually in additional revenues for the federal government (as well as additional revenues for provincial governments where they would benefit from a broader federal tax base with fewer loopholes).

These additional revenues could, for example, easily fund:

- Affordable child care for all plan, with a $1 billion investment in 2020 and an additional $1 billion each year for ten years to 2030.

- A national universal pharmacare for all plan, estimated to cost $10-$15 billion more than what federal and provincial governments now pay, providing average savings of $600 per household.

- Free university and college tuition for all Canadians. Total tuition fees amount to about $9 billion (including foreign students, net costs would be lower without the tuition tax credit).

- Elements of a “green new deal”, such as energy retrofitting of buildings and 40% of Canada’s homes, reducing homeowner energy use and bills by an average of 30% each, and improving the efficiency of other buildings by 50% at an estimated cost of $6 billion annually (and generating over 80,000 jobs annually).

Note: Estimated revenues for the major tax reform proposals are included below, both in the text and in a table at the end of this document, with some brief notes on sources for these estimates. However, estimates are not included for a number of these measures, either because the impacts are expected to be relatively smaller and/or hard to predict. While the estimated revenues are developed mostly from figures published by Finance Canada, Statistics Canada and the Parliamentary Budget Office, other estimates and forecasts will vary depending on assumptions chosen, including behavioural responses, interactions and other impacts. Some of these impacts will be positive, some negative, and much will depend on interactions with other measures implemented and their impacts. We’ve limited these assumptions on the basis that different positive and negative impacts will cancel each other out.

PROPOSALS

A. Ensure Corporations and the Wealthy Pay their Fair Share by Closing Regressive Tax Loopholes and Making Taxes More Progressive

1. Close regressive tax loopholes: Total $16 billion+

The first thing the federal government should do is close regressive tax loopholes that allow those with high incomes to pay lower rates of tax than the rest of us, and that have other negative impacts for the economy and society. The Liberals promised to do this in the last election, and immediately eliminated a number of regressive tax measures introduced by the Harper government, but they left the job half done.

a. Eliminate the stock option deduction. The stock option deduction is Canada’s most regressive income tax loophole, with over 90% of the benefits going to the top 1%. It’s also bad for the economy because it encourages corporate executives to use corporate funds to engage in stock buybacks, which increases the value of their compensation, instead of investing in the economy and creating jobs. This tax loophole costs the federal government an estimated $700 million in revenues annually, and costs provinces another $300 million for a total cost of over $1 billion. The 2019 budget announced that the Liberal government intended to limit the use of this for executives of large, mature companies. However, their proposal would still leave a lot of holes, not affect any company not considered “mature” and allow each at least $200,000 in low taxed options each year. We believe that companies should still be able to provide their employees with stock options, but don’t see any reason why they should be provided with lower, preferential tax rates. $700 million

b. Eliminate the lower tax rate on capital gains, both for personal and corporate income. The reduced tax rate on capital gains—the increase in the value of investments—is one of Canada’s expensive tax loopholes, costing the federal government an estimated $8.25 billion in personal income tax revenues and almost $9 billion from corporate tax revenues, for a total of over $17 billion annually. However, it makes sense to adjust the capital gains tax rate for inflation so those who have held a family cabin, second home or other investments for many years don’t pay tax on increases related to inflation, which could lower the rate below current rates for properties held for decades. This would be similar to the lower rates that a number of other countries, including the U.S., have for longer term investments. Eliminating this tax break that speculators benefit from will also help to reduce the rise in house prices, making housing more affordable and save the federal government $13.6 billion annually.

c. Eliminate business meals and entertainment expense deduction. This tax perk allows businesses to deduct half the cost of private boxes and tickets to sports events, concerts, restaurant meals and drinks, entertaining business partners and clients at night clubs, country and golf clubs, cruises, vacations and much more – and costs the federal government over $500 million annually. It also contributes to some unsavoury forms of lobbying and entertaining. For instance, SNC-Lavalin could no doubt have claimed many of the costs it incurred for "entertaining" Saadi Gaddafi as part of their alleged bribery scheme to obtain contracts in Libya. The tax law says that, in order to be eligible for this deduction, actual business must be conducted at these events, but there’s no way to confirm this. Not only does this cost the federal government hundreds of millions annually, but it also drives up the cost and reduces the availability of tickets to sporting events for ordinary people. Even American President Donald Trump last year eliminated their similar deduction for entertainment expenses, although retained it for meals. Eliminating this tax perk would save the federal government over $500 million annually.

d. Reduce corporate dividend tax credit. This tax break provides a credit to those receiving corporate dividends. It’s supposed to compensate shareholders for the corporate taxes that businesses pay, but many don’t pay any corporate income taxes and most pay tax at a lower rate than the dividend tax credit provides shareholders for. This tax break costs the federal government over $5 billion annually, with over 90% of its value going to the top 10% and almost half to the top 1%. More than two-thirds goes to men, with less than a third going to women. This should be limited to the tax rate actually paid by corporations. Doing this would not only be fair, but also provide less of an incentive for corporations to avoid taxes through various methods. Doing this would lead to a savings estimated at least $1 billion annually.

e. Cap lifetime Tax Free Savings Accounts at $65,000. Tax Free Savings Accounts might not cost the federal government billions up front, but they will be highly corrosive for federal and provincial revenues over the longer term if the amounts that can be accumulated keep on growing – and it’s a tax loophole that primarily benefits top incomes, who have already maxed out on their RRSPs and other pensions. While this tax break costs the federal government an estimated $1.3 billion annually now, this amount can be expected to balloon to almost $10 billion in a dozen years and to keep on growing, unless it is contained now. The total limit per individual is now up to $63,500. The federal government should cap it at this amount to stop increasing this blood flow from future revenues. This would save the federal government an estimated $200 million annually to start, and considerably more in future years.

f. Conduct an open public review of tax loopholes and expenditures and other ways high incomes and corporations are able to avoid taxes, including private family trusts and tax havens, to eliminate or limit the most unfair and expensive. In the 2015 election campaign, the Liberals promised to conduct a “wide-ranging review of the over $100 billion in increasingly complex tax expenditures that exist and reduce those that unfairly help those with individual incomes in excess of $200,000 per year.” There may have been a review, but nothing was made public about it. The federal government should have a review, but ensure that it is open and public, that it holds hearings across the country, engages diverse stakeholders, and publishes its analysis and recommendations.

2. Make our Tax System more Progressive: Total $16.3 billion

a. Restore the corporate tax rate to the rates that applied a decade ago in 2010, restoring the general corporate tax rate 15% to 18% and the small business rate proportionally from 9% to 11%. These rates are far below the rates that applied two decades ago. Deep cuts to corporate income tax rates over the past two decades—with the federal rate slashed from over 29% down to 15%—have been a hundred billion-dollar failure. They haven’t stimulated business investment—instead paralleling a similar decline in rates of business investment—but have led to record corporate profits, massive corporate surpluses and hundreds of billions in corporate cash surpluses. They’ve also contributed to increased tax avoidance as those with the means shift their personal incomes to the corporate/ business tax base to take advantage of rates at less than half that apply to the personal income tax base. According to the PBO, increasing the general rate by three percentage points would increase federal revenues by $5.7 billion annually. Increasing the small business rate by two percentage points would provide the federal government with an additional $1.6 billion annually, for a total of $7.3 billion annually.

b. Increase the top federal marginal income tax rate on incomes over $750,000 from 33% to 37%. The Trudeau government increased the top income tax rate for those with incomes over $200,000 from 29% to 33%. However, this rate is still very low compared to the top tax rates that applied up until 1981, when a federal top rate of 43% applied to income of over $120,000. Increasing the top federal rate to 37% for individual incomes above $750,000 would be reasonable, well-below the rates that applied up until the 1980s, and, combined with provincial rates, would also be well-within the revenue maximizing rates that various experts have suggested. Professor Lars Osberg has estimated that raising the top rate to 65% for those with incomes above $200,000 would generate $15 to $20 billion annually. But we’re proposing a lower increase for a smaller group: just the top 0.1%. There are about 27,000 Canadians with incomes over $750,000 and they had an average income of about $1.7 million each. This means an additional 4% tax rate would generate about $1 billion annually.

c. Level the digital playing field and stop giving foreign internet giants significant sales and other tax advantages over Canadian producers by applying the GST and HST to imports of digital services, eliminate the business deductibility for advertising expenses that foreign internet platforms also benefit from, and apply corporate tax to the business they conduct in Canada. It’s more than five years since the OECD highlighted taxation of the digital economy as the top priority action item of its Base Erosion and Profit Shifting Action Plan. The vast majority of other OECD and G20 countries have taken action on it; Quebec and Saskatchewan have also moved forward. These tax loopholes for foreign internet companies provide a significant benefit to Google and Facebook in particular, which are recipients of over 50% of the federal government’s advertising dollars and close to a third of all money spent on advertising by Canadian businesses. These tax loopholes also enable platform-based companies such as Uber to avoid sales and other taxes and provide an incentive for them to avoid other taxes as well. Additional revenues from these measures are estimated at an additional $1 billion annually.

d. Introduce a financial activities tax on the compensation and profits of the financial sector. It’s ten years after the financial crisis and the financial sector still hasn’t paid for what it caused. Many advocated for the introduction of a financial transactions tax, but a simpler solution for Canada would be to introduce a Financial Activities Tax, as the IMF had suggested a number of years ago. Financial activities were largely exempted when the GST was introduced decades ago for various reasons. A Financial Activities Tax would remedy this, by applying a tax to the compensation and profits (equivalent to the value-added) of the financial sector. At a rate of about 5%, this type of tax would generate over $5 billion annually.

e. Limit the amount that corporations can deduct for compensation to any single executive or employee to $1 million annually. The federal government should send a message to corporations that sky-rocketing corporate compensation—now up to an average of $10 million for each of the top 100 paid CEOs—and growing inequality isn’t considered acceptable, and that it shouldn’t be subsidized by allowing it to be a tax deductible expense. This should be broad-based and cover not just straight pay but also the value of stock options, other forms of compensation and performance-based pay, as is now covered in the U.S.

f. Reintroduce inheritance tax on high-wealth estates. Many countries, including the United States, levy taxes on high-wealth estates that are passed on as inheritances. Canada used to have a federal inheritance tax, but this was eliminated decades ago with the introduction of capital gains taxes. However, capital gains taxes far from cover the value of large estates. A number of provinces levy small estate taxes/ probate fees, but these can also be easy to avoid. Senator Bernie Sanders is proposing an increase in the U.S. estate/ inheritance tax to 45% for estates from $3.5 million to $10 million, 50% for estates of $10 to $50 million, 55% for estates of $50 million to $1 billion and 77% for estates of over $1 billion. We estimate that a 45% tax on the inheritance/ estates of over $5 million (similar to the U.S. has had) would generate $2 billion annually.

g. Introduce pre-filled tax forms and send them out to all Canadians who request them. It’s estimated that Canadians spend the equivalent of over $5 billion in direct expenses and time filing their taxes each year. The federal government could dramatically reduce this expense and annual hassle for families by providing pre-filled tax forms to all those who want, as a number of Scandinavian countries do. The federal government already receives a significant amount of individual tax information from employers, charities, financial institutions and others, about 80% of the information required for most tax filers. Given that the CRA already has most of the information required, it doesn’t seem right that Canadians should have to pay additional amounts to file their taxes. As governments have also moved to providing more social and other benefits (the GST credit, Canada Child Benefit, Canada Workers Benefit, Carbon Incentive Payments) through the tax system, those that don't file their taxes—often the most vulnerable—aren’t receiving the benefits they’re entitled to.

h. Introduce a threshold of $20 below which the CRA does not pursue taxes owing for individuals and small businesses. The CRA has had an annual threshold for many years of $2 below which it doesn’t require Canadians to pay income taxes owing. This amount should be raised to $20 and applied to all taxes and taxpayers, including to small businesses for the GST. There are instances of the CRA threatening to seize the assets of small organizations over a $5 tax bill. This is a waste of resources for the CRA and Canadians.

B. Tackle International Tax Evasion, Avoidance and Tax Havens: $6 billion+

1. Canada should take a lead in advocating for and implementing fundamental reform of the international corporate tax system. The head of the International Monetary Fund (IMF) recently described the international corporate tax system as "fundamentally out of date.” The IMF has estimated that governments world-wide lose over US$600 billion in tax revenue annually from use and abuse of tax havens and profit shifting, with the losses in Canada estimated at a minimum of $8 billion annually.

Important discussions now underway at the OECD, IMF and UN could either fundamentally reform and fix the system, or apply another ad-hoc patch to a fundamentally broken system. Canada could make a unique contribution to this issue because we have the best national experience with a system that should also be applied internationally. For more than 50 years, we’ve used a system of allocating the taxable income of corporations between provinces for tax purposes using a formula based on real economic factors, primarily sales and employment payroll expenses. This straightforward system of “formulary apportionment” has worked well without controversy in Canada and is now also being proposed by experts and other countries as a model to reform the international tax system. The United States uses a similar system to allocate corporate profits between states for tax purposes and India is now proposing to use this type of system to also apply taxes on multinational enterprises.

The elements of this reform should include:

a. Apportionment of taxable income/ profits of MultiNational Enterprises (MNEs) to Canada and other countries according to a fair formula that reflects real economic factors, including sales, employment/payroll and possibly capital assets. This should be combined with the adoption of a common consolidated international corporate tax base, which Europe is moving towards, so corporations and countries work with a common set of financial books.

b. Unitary taxation of multinational enterprises, so corporations can’t use affiliated corporations to shift profits. This is consistent with the Private Members Bill C-362 on economic substance.

c. Stronger limits on measures used to shift profits, including putting limits on interest deductibility and payment of royalties for intellectual property.

d. Support for a minimum international corporate tax rate to eliminate the vicious cycle of downward tax competition.

While international agreement on these issues is of course preferable, there’s no reason why Canada can’t move forward unilaterally on this. India is considering applying a system of formulary apportionment to the profits of MNEs operating in India, while other major nations—including the US, France, and the UK—are moving ahead with various measures to apply taxes to large multinational corporations.

2. Stronger enforcement and penalties to confront tax evasion and aggressive tax avoidance by high incomes and corporations, including applying much larger fines for individuals and corporations that promote and facilitate international tax evasion schemes. Canada levies relatively low penalties for those guilty of international tax evasion and against companies and professionals who promote tax evasion schemes, so there’s little deterrent. Together with stronger enforcement, the CRA also needs to increase penalties.

3. Increased funding to the Canada Revenue Agency (CRA) for investigation, audits, enforcement and prosecution of offshore, corporate and high income tax evasion. The Trudeau government restored some of the funding, programs and staff that the Harper government cut from the CRA, especially to the offshore and large corporations, but its capacity is still lower than what it was. Investments in compliance and enforcement by the CRA were estimated by the Finance department to yield a better than 10 to 1 return.

4. Restrict corporations or consortiums that engage in tax evasion and aggressive international tax avoidance from obtaining federal government contracts, or other forms of federal public funding and support (including through the EDC), and take this into consideration when reviewing foreign takeovers, with a tax haven blacklist. A disturbing number of corporations that gain much of their revenue from public sources take advantage of tax havens and aggressive tax avoidance to reduce the taxes they pay in Canada: the taxes that are used to pay for the public services they profit from. This should explicitly be taken into account when awarding government contracts or other forms of support.

5. End double non-taxation agreements with tax havens. Canada has signed tax agreements and conventions with a number of different tax havens that enable individuals and corporations to bring their income back into the country without paying tax, either in the tax haven or back in Canada. Canadian corporations have over $200 billion in assets in tax havens in jurisdictions with which Canada has signed tax treaties and wealthy individuals have billions more. The OECD’s Multi-Lateral Instrument legislation to change tax treaties will help to prevent some abuses, but many holes will remain through it and Canada and other countries have long lists of reservations. Unless we achieve further progress Canada should end what have been double-non-taxation agreements.

C. Improve Corporate Transparency

1. Create a pan-Canadian accessible public registry of the real/beneficial owners of Canadian corporations and of foreign corporations doing business in Canada. Canada has the weakest corporate transparency rules among all G20 countries, which has made us into a haven for international money laundering, terrorist financing, snow-washing and other corporate financial crimes. The lack of a centralized and accessible registry makes it much harder for the RCMP and law enforcement agencies to investigate and enforce these types of criminal activities. The Yukon in particular has become notorious as “the Delaware of the north” with very weak and flexible rules that substantially weaken protections for shareholders and creditors. The federal government should take the lead in establishing a pan-Canadian public free and accessible registry as the UK has done and other European countries are doing (and as the BC government has now committed to) and should encourage other provinces and territories to join. The federal government should also require that any company that it does business with or that receives federal government funds also participate in this registry.

2. Modernize and strengthen anti-money laundering reporting requirements to high-risk sectors of the Canadian economy. Money laundering has shifted into real estate, casinos, trusts, and luxury goods. The federal government should expand anti-money laundering reporting requirements to these sectors to deter criminals from exploiting these sectors by remaining anonymous. These high-risk sectors should be required to collect and verify beneficial ownership information at the point of transaction, aligning these sectors with reporting requirements of banks and credit unions.

3. Publish how much large corporations (with total annual income of over $100 million) actually pay in corporate and other federal taxes, as is required in Australia and is increasingly required in other parts of the world and for different sectors. Incorporation provides significant privileges and the amounts reported in financial statements aren’t necessarily accurate of how much corporations actually pay in taxes. The international Extractive Sector Transparency Measures Act (ESTMA) requires multinational resource/ extractive industries to report these figures, while the Global Reporting Initiative (GRI) is also expected to require large multinationals to report this and other financial information.

4. Make the country-by-country reports of multinational enterprises public. The federal government now receives country-by-country financial reports from multinational enterprises with more than €750 million (or C$1.125 billion) in total revenues. These provide basic information necessary for determining tax obligations, including revenues, taxable income, taxes paid, capital assets and the number of employees. This information should also be made public.

5. Publish more detailed aggregate statistics of how much corporations, private family trusts and top incomes pay in taxes. The CRA publishes detailed aggregate information and statistics on what ordinary Canadians pay in personal income taxes, broken down by income, region and many other dimensions. However, it provides very little information on what corporations, those with top incomes and private family trusts pay in taxes, even at an aggregate level. The CRA should make more of this information available at an aggregate level while preserving confidentiality.

6. Require that the CRA publish estimates of the tax gap every three years and publish a list of all those convicted for tax evasion, including a separate list for those convicted of international tax evasion, and to share the data required to develop these estimates with an independent agency, such as the Parliamentary Budget Office. Canadians for Tax Fairness campaigned for the CRA to publish estimates of the tax gap—the difference between the amount of revenue it should receive and the amount it actually receives—and it has started to do so, but it is under no obligation to continue to do so. Liberal Senator Percy Downe sponsored Bill S-243 to require the CRA to do this by legislation. This bill received strong approval from the Senate and from opposition parties in the House of Commons, but wasn’t supported by the government majority in the House of Commons for technical reasons. With no objections to the actual substance of the bill expressed by Liberals, we hope all parties will support these changes after the next election.

7. Require that the CRA provide public information on the number and size of tax settlements and write-offs. The CRA agrees to tax settlements and writes off taxes owed with corporations and individuals, sometimes for millions of dollars and in one case for $133 million, but there’s little or no information provided on the magnitude of these. As these are effectively public expenses and write offs, the CRA should publish information about the extent of them, with some details about their numbers and size.

8. Introduce stronger protection for whistleblowers. The federal government needs stronger protection for whistleblowers and should implement the recommendations of the House of Commons government operations committee report on strengthening whistleblowing protections for federal public servants.

D. Combat climate change and support sustainable development: $5 billion+

We need to employ a wide range of tools to address climate change and to preserve a healthy environment, including by putting a stronger and progressive price on pollution instead of subsidizing it. Putting a progressive price on pollution can support this by directly reducing emissions, by raising revenues to invest in complementary environmental measures, ensuring a majority of households are better off, and supporting a just transition for workers and communities.

1. Strengthen the federal carbon tax framework, by eliminating the preferences for large emitters, and converting the cap and trade mechanism into a transparent carbon tax with border adjustments, so tariffs are applied to imports from countries that aren’t taking sufficient action on climate change, and rebates are provided to Canadian exporters to those countries. The federal government’s carbon price framework is progressive for households, with 80% of households—all except the top 20%—receiving more in rebates than the additional costs they will pay from the carbon tax. However the federal carbon pricing system for large emitters was substantially weakened so many will pay the carbon price on only 10% of their emissions, and in total large emitters are expected to pay less than 10% of the federal government’s total carbon revenues, despite the fact that they’re responsible for over 40% of Canada’s total emissions. Additional funds raised should be spent on complementary programs, green new deals and just transition measures, and to compensate communities and households for their additional costs. Applying the carbon price to all the emissions from large emitters would increase the federal government’s revenues by approximately $3 billion annually.

2. Eliminate fossil fuel tax subsidies. The federal government has committed many times to eliminate the tax subsidies it provides to fossil fuel production, which are at odds with its climate change strategy and carbon taxes. The federal government started to phase some out, but then it also introduced others, and many still remain. Canada has committed to review its fossil fuel subsidies along and following that, the federal government should move quickly to eliminate all of them. The value of these subsidies fluctuates considerably from year to year, as much on the state of the industry as on the state of the tax system. Estimated savings: About $2 billion annually, according to new estimates from the Parliamentary Budget Office.

ESTIMATED REVENUES

|

Measures |

Impact |

Sources, brief notes |

|

Close regressive loopholes |

$16 billion |

|

|

• Eliminate Stock option deduction |

$700 million |

Finance Canada, 2019 Tax Expenditure and Estimates (TEE) |

|

• Eliminate lower rate on capital gains for PIT & CIT |

$13.6 billion |

TEE, Assume 80% of total cost over $17 billion |

|

• Eliminate meals and entertainment deduction |

$500 million |

TEE, for CIT and GST cost |

|

• Reduce corporate dividend tax credit |

$1 billion |

Estimate 20% savings from $5.6 billion annual cost reported in TEE |

|

• Cap Tax Free Savings Accounts at $65,000 |

$200 million |

Estimate of initial savings from $1.6 billion annual, but rapidly growing, cost of TFSA program. |

|

• Others from review |

? |

|

|

Make Tax System more Progressive |

$16.3 billion |

|

|

• Increase general corporate tax rate to 18% |

$5.7 billion |

PBO Ready Reckoner tool |

|

• Increase small business tax rate to 11% |

$1.6 billion |

PBO Ready Reckoner tool |

|

• Increase top federal PIT rate on incomes over $750,000 to 37% |

$1.0 billion |

Based on Statistics Canada high income figures, using latest 3 year averages |

|

• Level the digital playing field |

$1.0 billion |

Lower end estimate based on various figures |

|

• Introduce a financial activities tax at 5% on profits and compensation of financial sector |

$5.0 billion |

Estimate from CCPA Fair Shares report, figures for 2010 |

|

• Limit amount corporations can deduct for exec compensation to $1 million each |

-- |

Would be relatively low |

|

• Reintroduce inheritance tax on high-wealth estates |

$2.0 billion |

Estimate based on U.S. revenues and Canadian figures, in CCPA AFB |

|

Tackle International Tax Evasion and Avoidance |

$6 billion |

|

|

• Overall estimate for all measures |

$6.0 billion |

Based on lower end estimates of Canada’s losses from int’l corporate tax shifting. |

|

Environmental tax measures |

$3.3 billion |

|

|

• Strengthen carbon tax framework by eliminating preference for large emitters |

$3.0 billion |

Estimate based on reported emissions from large emitters in affected provinces. Doesn’t include additional amounts for higher price or border adjustments |

|

• Eliminate remaining fossil fuel subsidies |

$2 billion |

Based on Sept 2019 estimates from PBO |

|

Total |

$41 billion+ |

Notes: The revenue figures included are based on static estimates mostly from Finance Canada, the PBO and Statistics Canada, without behavioural impacts. Behavioural factors could tend to reduce these through both real responses and tax shifting, reflecting their “elasticities”. However, with the closing of loopholes and increased enforcement, tax shifting would be reduced. Decreased revenues from behavioural factors would be offset by increased revenues from interactions of these measures. For instance, closing tax loopholes will lead to proportionately higher revenues from hiking top income tax rates and vice versa. Stronger stimulus impacts from public spending than from tax cuts would also lead to higher revenues.