Résumé

What is Wrong at the CRA: and How to Fix It is based on interviews with 28 current and recently retired tax professionals at Canada's national revenue agency. It reveals serious issues and includes recommendations from Canadians for Tax Fairness to improve the integrity, credibility and effectiveness of the CRA.

The interviews reveal:

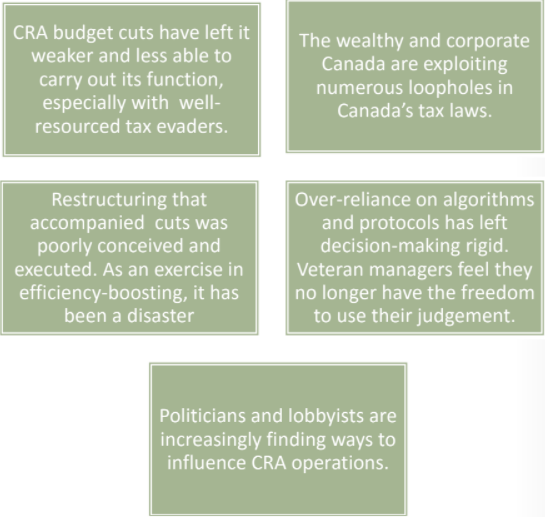

- Politicians and lobbyists are increasingly finding ways to influence CRA operations.

- Corporate lobbying to avoid prosecution is a reality.

- Employees are aware of political interference in proceeding with investigations.

- There are high attrition rates of experienced professionals.

- Reduction or shutdown of enforcement offices across the country.

- Concerns about capacity to carry out professional duties under the current structure.

The facts are that:

- The federal government and most provincial governments rely on the CRA to collect revenues to fund everything from healthcare to education.

- Simultaneous with the cuts to the agency’s capacity, $199 Billion in untaxed money has been shifted to tax havens, at a cost of at least $8 billion to Canada’s budget.

- The integrity of Canada’s tax system is taking a hit. There have been numerous media reports and information leaks that indicate mega-corporations and wealthy Canadians are increasingly emboldened to engage in offshore tax schemes.

The report recommends immediate actions to restore integrity in the process of raising revenue:

- Prioritize and prosecute big tax avoidance schemes rather than focussing on charities, non-profits and smaller cases.

- Proceed with a stalled court case against KPMG’s activities on the Isle of Man.

- Implement a Tax Gap report.

- Boost CRA’s capacity for investigation and enforcement of tax haven cases.

Rapport

A Short History: The 2013 Budget Speech by Jim Flaherty promised stepped up action on tax avoidance. This raised hopes that Canada would adhere to promises it made to its G8 partners to crack down on profit shifting and tax havens. Soon after, auditors and investigators received layoff notices. Federal revenues and the budgets of eight provinces rely on good management at the CRA.

INTRODUCTION

The Canada Revenue Agency plays a vital role in collecting revenue for the federal goverNment and many provincial governments. It should be doing that supported by fair tax policies and modern, effective methods.

But for years something has been very wrong at CRA. Whether it was lack of political will, intentional neglect, or failure to understand the role of good tax policy – the federal government has let the CRA falter. Systemic issues plague Canada’s tax system. Those issues have undermined equality. They have also resulted in the loss of billions of dollars of revenue that should be building and maintaining Canada.

This report was prepared by Canadians for Tax Fairness to provide evidence of problems which impact the CRA’s ability to do right by Canadians. Much of its preparation occurred before the election of a new government in October 2015. It incorporates the perspective of current and retired CRA auditors, investigators and managers. It takes on issues that received public attention but were dismissed by the previous Conservative government including Prime Minister Stephen Harper and successive finance and revenue ministers.

This insider look at the CRA helps us understand where the past decade has left us and where we should be headed.

Tax fairness is one of the most serious issues facing Canada and the global community. It is our hope providing this evidence and laying out solutions will help Prime Minister Trudeau carry through with his commitment to fair taxation.

Running a great country costs money. Whether it’s a national healthcare system, the TransCanada Highway, or food inspection, Canadians innately understand the wisdom in pooling resources to make good things happen. The Canada Revenue Agency plays a vital role in collecting that revenue for the federal government and many provincial governments.

As a democracy, we need fair tax policies and a well-functioning revenue agency that ensure everyone pays their fair share. Those things take attention and commitment.

That attention and commitment has faltered. Whether it was lack of political will, intentional neglect, or failure to understand the role of good tax policy – the result is the same. Systemic issues plague Canada’s tax system. Those issues have undermined equality. They have also resulted in the loss of billions of dollars of revenue that should be building and maintaining Canada.

And last, but not least, they are preventing Canadians who work at the CRA from doing the best job they can on behalf of the rest of us.

This report was prepared by Canadians for Tax Fairness to provide evidence of problems which impact the CRA’s ability to do right by Canadians. Much of its preparation occurred before the election of a new government with a stated commitment to undertake a major overhaul of the CRA, including combating international tax evasion.

It uniquely incorporates the perspective of current and retired CRA auditors, investigators, and managers. They take on issues that have received public attention but were dismissed by the previous Conservative government led by Prime Minister Harper and successive finance and revenue ministers.

Their input helps us understand where the past decade has left us and where we should be headed.

Tax fairness is one of the most serious issues facing Canada and the global community. It is our hope providing this evidence and laying out solutions will help Prime Minister Trudeau carry through with his commitment to fair taxation.

The Lay of the Land

It has been a tough decade for the CRA:

- Hundreds of millions of dollars in budget cuts

- Restructuring that has taken skilled and seasoned professionals out of key roles.

- A procession of inexperienced ministers with a vague understanding of its role in Canada’s economy.

- A cumbrous tax code made worse by annual additions of boutique tax cuts and loopholes from governments addicted to political expediency.

- Growing Canadian corporate profit shifting to offshore tax havens

- Misplaced priorities; going after small-time tax cheats, and harassing charities with politically motivated audits, while ignoring big-time tax cheats.

Were these and other “hits” on the CRA a result of a government that has failed to grasp the new fundamentals in a world of offshore havens, profit shifting and secret bank accounts? Or was it part of a deliberate plan to implement the anti-tax and small government philosophy of Prime Minister Stephen Harper?

Whatever the answer, this management by fracking has caused deep damage to the government agency tasked with collecting the money that funds our healthcare, education, safety and more. It was only a matter of time before the cracks began to show. And they have – with alarming regularity:

- Media reports about “reputable” tax firms like KPMG allegedly advising clients to push the limits on offshore tax haven laws.

- Outrage from Canadians about an $8 million audit program targeting not for profits and charities not aligned with Conservative policy.

- Public criticism from the Auditor General, the Parliamentary Budget Office, members of Canada’s Parliamentary Finance Committee about the CRA’s failure to ensure Canadian corporations and individuals were paying their fair share.

- Pushback from environmental and social policy organizations who had been targets of audits and investigations due to their criticism of the Conservative policies

Without exception, the Conservative government dismissed public concerns using the most generic of political platitudes. More explanation, they insisted, would breach taxpayer confidentiality.

End of discussion. Until now.

The Project

As Canadians for Tax Fairness gained more visibility in our work across the country we were approached privately by CRA staffers - current and retired. The first time it happened, it was a surprise.

Then it became a regular occurrence – they even called in when we participated in radio talk shows. The themes were constant and worrisome.

They expressed frustration at the state of affairs inside the agency and how that played out in creating a modern, efficient and smart organization. They recognized that CRA staff had to be on their game to fight the growing problem of profit shifting and tax havens.

Some expressed real dismay at the harsh treatment ordinary taxpayers received while many wealthy tax avoiders availed themselves of high-priced lawyers to negotiate out of court settlements and a voluntary disclosure process that allowed them to avoid penalties and potential prosecution.

They wanted Canadians to get value for the money and trust taxpayers to invest in the CRA. They wanted to put an end to the politicization of the CRA. We saw their faces and shook their hands. But always with a warning that they couldn’t share their names publicly. Those experiences inspired us to dig deeper.

In the late summer of 2015, Canadians for Tax Fairness spoke to 25 CRA staff. They included auditors, fraud investigators and veteran managers charged with overseeing audits of complex international companies. Their experiences were based in offices across Canada. Some were newly retired. Most still work there.

Temperamentally, this group of people plays by the rules. And they were very aware of confidentiality agreements and a Code of Ethics that threatens discipline for even the most general discussion of how well you think your agency is serving the public. Yet, they were willing to take this risk in order to blow the whistle on the serious problems they saw.

CRA employees are prohibited by law from disclosing taxpayer details to the public or the media. No tax taxpayer data was discussed and no comments about specific cases were solicited or given in these interviews.

This project reports on their assessment of the damage that has been done – and more importantly, a road map to fix it.

The picture that emerged was of an organization struggling to carry out its function in the face of government mismanagement. This includes major budget cuts, a poorly conceived restructuring effort, and targeting those who make tax filing mistakes rather than prioritizing big time tax cheats.

“I don't believe that any taxes are good taxes.”

- Stephen Harper, G8 Meeting, July 2009.

What Happened to the CRA?

During its time in office starting in 2006 the Conservative government applied the scalpel to much of the public service. It did so with particular vigour at the CRA, which had its budget slashed by more than $250 million from 2013 to 2017.

It happened under the “austerity” banner. But it was a false economy. Several studies have shown that for every dollar invested in hiring skilled auditors and investigators, Canada gets seven to ten dollars in return.

If CRA’s ministerial staff weren’t aware of this, it begs the question of good management. If they were, it begs the question of whether the Harper government was deliberately “reducing revenue” in order to justify cuts to government programs for ideological reasons. Whatever the motive, the impact on the front lines has taken a toll.

“They say they want to improve the CRA. When you look at what’s happening, it’s the opposite. They say they're going after high net worth tax evaders. But they’re really building structural barriers that make our job harder.”

Many respondents said that as the tax agency’s audit capacity is eroded, wealthy individuals and large companies have become bolder and more aggressive in their efforts to avoid taxes. They often succeeded because the CRA no longer earmarked financial resources to challenge them. They were critical of the level of training provided by the CRA, especially when it came to the handling of complex accounting issues. They said that while the necessary skills development courses were provided in years past, this is no longer the case.

“That’s just it. People still love the job they do, they still see it as vital. There’s a lot of meaning to the work. But there’s the restructuring and the budget cuts, changes in policy. They make the job harder, and the frustration of knowing you’re not respected, it wears you down.”

Expertise is now mostly acquired on the job. According to this group of professionals, the CRA’s performance has declined when it comes to administering Canada’s tax laws.

They said that despite the government's assurances that taxpayers are treated fairly, the CRA is anything but fair. They cited lack of agency resources, stacked up against behind-the-scenes lobbying by deep-pocketed corporations and wealthy, well-connected families.

The impact on the front lines has taken a toll on morale, leaving employees afraid for their jobs and sometimes reluctant to take on challenging assignments that could negatively impact performance reviews. Respondents covered a lot of ground in their comments, but five main points emerged.

Shortly after these interviews were completed, a CBC National News investigative report revealed that CRA investigators had built a case against accounting giant KPMG for a “pay no tax scheme” it promoted to clients with a minimum of $10 million in assets. The scheme seemed breathtakingly bold and aggressive to investigators. And they said so in court documents. The case stalled for three years because of apparent “negotiations” to secure an out-of-court settlement. But after media exposure Canadians for Tax Fairness helped to generate the case is now scheduled for hearings again.

Each of these points on its own paints a disturbing picture. They raise concerns that were not addressed specifically in either the tax section of the Liberal platform or in Prime Minister Trudeau’s open letter to the public service during the election campaign. That is why we call attention to them now.

This report examines each of the five points. It outlines the perspectives expressed by the CRA staffers. We have not attributed their direct quotes which are emphasized in boxes throughout the report. We have added context with publicly available information and outlined potential solutions.

DEATH BY A THOUSAND CUTS

Canadian tax law – and the system for regulating it – was designed in another era. Tax havens, the digital economy, and the explosion of offshore trusts present immense challenges to the revenue agencies of most countries.

Large accounting firms like KPMG embrace and profit from this new era. Bankers like HSBC hire people with a talent for sniffing out opportunities to capitalize on cracks in the system.

Meanwhile, the Canada Revenue Agency’s funding has been slashed by half a billion dollars over two years and the agency dismantled its dedicated capacity in key areas such as international tax avoidance

“This restructuring takes our best people away and the expertise they’ve developed goes with them.”

Publicly, Conservative Minister of National Revenue Kerry-Lynne Findlay attributed the cuts announced in 2013 to a reorganization plan. But if there was a plan, it was locked inside the Minister’s office rather than shared with those on the front lines. The result has been confusion, caution and frustration.

"The changes in the Criminal Investigations Program took out all those offices. It was 32 different offices across the country and they cut it down to six mega-offices. It took them over two years to staff up to the levels that they wanted. Meanwhile there were very few investigations going on because they didn't have the staff. Experienced staff ended up moving to other jobs."

Tracking and investigating complicated cases requires concentration, persistence and support. Professional methodologies that would flummox most of us are the lifeblood of a good tax practitioner or investigator. Some respondents saw firsthand how the organizational confusion imposed by cuts had impacted mission and effectiveness.

“We used to have enforcement divisions at almost every single office of the CRA...Now they call them Centres of Expertise. They have one in Toronto and another one in Calgary. Well, between Toronto and Calgary it’s a big area... and you have nobody in enforcement in that area.”

Respondents agreed that the budget cuts have had wide-ranging negative impacts, the most obvious being that there are not enough highly specialized employees to provide sufficient and appropriate audit coverage. Many have been left with more cases than they can process.

They worry that they might be missing clues. There is a concern that fewer high risk taxpayers will be audited, and that they won’t have the time or the training to identify complex tax transactions resulting in significant tax leakage.

CRA staff who participated in the survey were seasoned professionals, so their comments are typically restrained. Nevertheless, it was clear that many had strong feelings about the subject. This manager summed it up:

“Everyone seems to be scrambling. Four years ago I spent about 50% of my time actually helping with research, helping my auditors. But not anymore... now it feels like 25%.”

In tandem with the cuts, the Conservative government restructured with the ostensible aim of doing the job with significantly fewer staff. This included dismantling and merging highly specialized units focused, for example, on the mining and oil and gas industries. The changes forced staff with specialist skills to become generalists. It also involved closing regional offices.

Several respondents warned that the restructuring is having the opposite from the intended effect. It has resulted in the loss of expertise built up over years. They also voiced frustration that there is little consideration for input about restructuring from those with an intimate understanding of the CRA and the wider industry.

"They haven’t really consulted us, they haven’t asked our opinion on how we could do things better. There’s ... demoralization in the fact that we’re just being told what’s going to happen and we don’t have any say in it.”

One of the measures undertaken as part of the restructuring is a subtle imposition of revenue quotas. Staff are expected to audit a certain amount of new cases in a given period and to achieve a specified level of tax recoveries.

This is a cause for concern because tax laws are supposed to be applied equally, whether you’re rich or poor, a small business or a multinational. Quotas create incentive to pursue the easiest targets. Complex, time-consuming cases get ignored. Respondents pointed out that the quota system is “not official but.....”

"You have to bring back a certain amount of money every day, you have to find it. You’re basically forced to go after the lowest hanging fruit. Why would you spend your time in a long, drawn out detailed investigation when you can just go after mom and pop operations that can’t afford to fight back?”

That not so subtle message from the head office goes against the grain of a good auditor and impacts morale. As does poorly managed restructuring. Significant numbers of staff are leaving. Some because their positions have been declared surplus. Some opt for early retirement. Others have been recruited by some of the same tax law and accounting firms they investigated.

Succession planning within the agency is a non-starter resulting in the loss of a valuable store of knowledge. There is concern that “acting assignments” are being abused as a result. The number of acting staff and the length of time they work in those positions far exceeds the intent of the program. This is generally an indication of an organization under stress.

“As the old guard leaves, often no one picks up the torch. If new people don’t pick up the torch the institutional knowledge disappears.”

Whether government’s lack of vision and poorly managed change is intentional or as a result of incompetence – the impact is the same. The CRA is the federal government’s main revenue generator. The current situation has a profound impact on the government’s ability to fund public services and carry out its responsibility to Canadians.

Despite the government’s protestations that the cuts and subsequent restructuring have left the agency stronger and more efficient, the evidence tells another story.

One Toronto staffer said the CRA's Toronto enforcement division used to refer, on average, 15 cases a year for prosecution. Now it’s down to just three or four.

The CRA drastically missed its target (56% versus 90%) on the number of full-scale investigations that are referred to the Public Prosecution Service of Canada.

Addressing the Challenge: Money Talks

The men and women in this survey are numbers people. They felt that a primary step in boosting the CRA’s capacity would be to establish a funding formula that reflects the 21st century realities facing the agency.

And their thinking was reinforced by the government’s own math. The finance department’s numbers show a ten-dollar return for every dollar invested in combating international tax evasion and aggressive tax avoidance. And that number doesn’t include the gains that provincial governments reap from those investments.

The comments from respondents show the impact for all of us when half a billion dollars is cut from the agency’s budget in a two-year period.

The number of taxpayers using tax havens and the complexity of the country’s tax legislation continues to grow through this period of instability.

In addition, Canada has active tax conventions -- commonly known as tax treaties – with 22 governments. Many of these treaties are with countries that have been the “haven of choice” for high profile cases reported in the media – including the Isle of Man and Liechtenstein.

Signing a treaty and then failing to assign adequate – or any - resources for tracking, investigating and prosecuting sends a message that stopping wealthy Canadians from engaging in global tax evasion is not a priority.

POLITICAL MASTERS AND CORPORATE AGENDAS

“If the company you’re auditing is big enough, they might hire a lobbyist and try to get some influence in Ottawa... I had a case of that. Political heavyweights started coming in.... it was sort of suggested by headquarters that I drop certain things...”

Democracies rely on citizens to pay their taxes. And so far, Canadians have one of the best compliance rates in the world.

But wealthy individuals and multinationals are playing the tax avoidance game as never before. There is an explosion in the number of tax lawyers, accountants and financial advisors recommending questionable avoidance schemes.

Recently, a retired Alberta businessman was offered such a “product” in the Calgary office of a reputable tax specialist. When he questioned its legality, the underwhelming answer was that it was “not illegal at this point”. He walked away.

But that incident and media reports about similar schemes offered by the accountancy powerhouse KPMG shook his belief in the fairness of the system.

Would you be a chump not to buy in? Are all the smart guys skirting the system?

Fair question. And one that carries an undercurrent in CRA units across the country.

Their political masters have cut funds and dismantled key programs. The Canadian government signs tax treaties with known tax havens but doesn’t provide staff the resources to monitor tax exchange information. The former prime minister, finance, and revenue ministers accepted event sponsorship from accounting companies only after CRA staff had initiated court cases against them.

Do their political bosses in Ottawa care about the work they are trying to do on behalf of Canadians?

The reality is that many tax professionals outside the CRA earn at least triple the salaries of government employees. At informal case hearings, they show up with a sharply-dressed contingent that outnumbers the government employees on the other side of the table. And they bring an attitude.

“When you get to a certain level in corporate Canada, there is a reality that you can pay very little tax. Get a big enough company with enough lawyers, it’s just a matter ofargument.”

Influencing the Outcome

A number of respondents, including senior CRA auditors have experienced that confrontation first hand. It comes with the territory. They warn that big businesses aren’t shy about throwing their weight around when it comes to taxes.

Some government employees have received thinly-veiled job offers during the interactions with the people they are supposed to be investigating. It is common knowledge inside the agency that highly qualified staff members receive offers of employment on a regular basis.

Others have felt pressure to recommend an out-of-court settlement – even having a settlement cheque presented to them right at a meeting table.

“KPMG is nothing — you should see some of the stuff. It's the tip of the iceberg and it's been going on forever. You talk to some of these people and they're so cocky, because they've got someone in their pocket advising them."

Business owners, especially big employers, are well aware of the leverage they can bring to bear on politicians, according to one veteran auditor. They’re not shy to use it. He said it is common for business owners to lobby politicians for more lenient treatment by the tax authority. They’re sometimes successful.

“I had one company say... ‘stop the audit’”.

Another respondent said that it’s not uncommon for companies “to hire a lobbyist and try to get some influence in Ottawa.” He too had been “told to stop an audit” for what appeared to be political reasons.

Auditors are not privy to discussions at senior ranks of the CRA about the handling of major cases. But they do have the experience to know when a taxpayer is likely breaking the rules and when, and if, an audit should be completed.

“I am offended personally when a decision is taken not to challenge a certain tax plan that clearly broke the law”

CRA staff are at the front line of public service. Properly directed, the fruits of their work ensures a fair tax system and the revenues to fund the government that Canadians want. When their professional advice is regularly ignored, it goes beyond an issue of staff being demoralized. It sends a message about the objectives and purpose of the agency.

“The primary focus right now above anything else seems to be issues management. They are more concerned about anything embarrassing to the minister or the government than they are about actually collecting tax.”

Taking it to Court

When potential tax evasion has been uncovered, the typical trajectory is to involve the Department of Justice. The taxpayer can end up in court. Evidence from the CRA audit is used to make the case for a fine or other penalty.

But the Department of Justice tax unit is seriously understaffed. Decisions not to prosecute are made even though, under different circumstances, they would be deemed worthy of prosecution. Often there is an out-of-court settlement. Sometimes a decision is made to simply close the file.

That has serious consequences:

- Canadians never learn about what has gone on.

- The industry insider perception about a weakened CRA is reinforced.

- And it is likely that hefty amounts of potential government revenue are lost because of a series of austerity cuts that have hobbled the men and women who have agreed to be Canada’s revenue watchdogs.

Dropping the Ball

A number of senior respondents expressed concern that the federal government fails to follow through with cases when major corporate interests are at stake.

One expressed frustration at how, after careful investigation and reporting, subsequent court cases are either settled out of court with an undisclosed deal or lost by the CRA.

Lack of resources certainly accounts for some of those decisions. But it appears that intervention by treasury and finance department officials plays a role.

Decisions about how to pursue tax cheats are often taken by high-level government officials in the Department of Finance. As a result, even senior CRA staff are sometimes unable to determine the reasoning behind decisions about, for instance, whether to audit or prosecute a taxpayer.

“I don’t know specifically who [the officials are] but I know the officials or delegates from Finance discuss issues with the CRA... I don’t know how information is conveyed back and forth, I just know there is cooperation at some level above me.”

One respondent was convinced that his unit’s professional methodologies clearly laid out how companies were crossing the line with their tax strategies. His superiors could see that as well. He suggested decisions not to proceed were based on an argument the companies and their lobbyists made about competitiveness. Whether they had broken the law was secondary.

Who Calls the Shots?

Tax competitiveness is a legitimate issue. But decisions made about Canada’s tax competitiveness should be a matter of public record and policy. Altering the rules at the enforcement level sets a dangerous precedent worthy of a notorious tax haven.

So here’s the question: Is it the people of Canada or corporate Canada making the tax rules and setting the effective tax rate?

The aforementioned incidents raise serious questions about how the law is applied to Canadian companies. What message does it send if a company breaks the law but has a team of lawyers and lobbyists successfully argue that they did so in the interest of competitiveness? What message does that send to regular taxpayers and smaller companies with less money to spend on legal teams or lobbyists? And what message does it send to auditors about applying the rules evenly?

There is no shortage of evidence that Canada brings in less tax than it should. In 2014, Canada fell markedly below the OECD average when it came to “tax burden.” The OECD unweighted average is 34.2% of GDP while Canada's was 30.8%. Tax revenue has fallen dramatically over the past decade. In 2000, taxes collected by the CRA were 35% of GDP.

Many developed countries experienced a sharp recession following the 2008 financial crisis. It is not surprising that they experienced a corresponding drop in tax revenue. But Canada was one of the lucky few to emerge from the crisis mostly unscathed, suffering only a very brief economic dip that reversed itself in 2009 on the back of soaring commodity prices. So why the drop in tax revenue?

Canada has the lowest corporate tax rate in the G7 – mostly due to tax cuts implemented by the previous Conservative government. Combined federal and provincial tax rates average 26.5%. Yet a growing number of publicly traded companies like First Capital Realty, Gildan Activewear, BCE and Manitoba Telecom pay less than 10 per cent. There is currently more than $199 billion of corporate Canadian money in tax havens. That is just the official amount – and it increases annually seemingly in tandem with cuts to CRA capacity.

Measuring What Canada Loses

Has there been an increase in tax cheats not getting caught? Canada currently has no grip on that answer. But it is well worth finding out.

As a way to expose tax avoidance and evasion, countries including the U.S. and Britain calculate what’s known as the Tax Gap. That’s the difference between the amount of tax they should be collecting and what they actually collect. Many governments find it a useful tool. Almost half of OECD countries produce tax gap estimates every three to four years.

According to the CRA’s website, figuring out the tax gap is an expensive and time-consuming exercise they contend is not worth the effort. “The high degree of difficulty and resources required to measure the tax gap and the uncertainty of the estimates are widely acknowledged,” it argues.

So instead, Canada has chosen an alternate approach. “The Government of Canada has invested its resources where they can deliver results - in helping taxpayers understand and meet their tax obligations before costly errors or non-compliance occurs, and in identifying and pursuing tax evasion and aggressive tax avoidance when they do occur.” (CRA website)

In other words, tax cheats only break the rules because they don’t understand them. Do a better job of explaining the rules and the problem goes away — at least, according to the CRA.

CLOSING LOOPHOLES

"Everybody's been doing it... Our income tax act is so big, it's just addendum after addendum, and it’s out of control. I've been to meetings put on by different accounting firms. They have monthly meetings for potential clients on how to get

around this tax law and that tax law. They have their own crew of people whose only job it is to figure out how to get around the law."

There was general agreement among the respondents that wealthy individuals and corporations using tax havens to hide income is a major challenge for the CRA.

Given recent media reports about wealthy Canadians stashing money in offshore bank accounts, it’s easy to conclude that the tax avoidance requires a complicated dishonesty to cunningly avoid detection.

While this is the case with many wealthy individuals, many large corporations have been avoiding taxes in plain sight. That’s because what they’re doing in many cases is legal in this country. Many respondents pointed this out, arguing that if Canadians feel the system is broken they should urge the government to fix the tax legislation.

“The CRA does a good job with [the bad rules] they’ve got,” said one auditor. “The rules are such that money can be put offshore and it's not against the law. We're a free country. If you want to keep a bank account in a foreign country, you can do that. All we require is that you report it.”

Respondents predicted that changing the law to close loopholes would be a major undertaking that would face big opposition from interest groups affected — the wealthy and the business community.

Some suggested that the reason the loopholes are there is to provide a boost for Canadian companies that must compete against foreign rivals that benefit from tax breaks

“From our limited perspective we can see that this company does this or this company does that. But the Department of Finance sees the big picture. They can say, we're okay with companies that do this because it’s good for the Canadian economy.”

There will always be countries willing to offer a better deal to the wealthy. Tax fairness advocates, the OECD and even the UN are struggling to find a solution to what is a multi-trillion dollar tax evasion epidemic. It ultimately becomes a race to the bottom.

When the Canadian government ignores this, it is a breach of trust with those who do pay tax. And it creates an unfair playing field for smaller companies who don’t – or more importantly won’t - create shell companies in tax havens.

It’s well known that while Canada’s statutory tax rate for corporations is around 26%, very few actually pay anything close to that. Indeed, half the members of the TSX-60, which includes 60 of the biggest companies in the country, enjoy an effective tax rate of less than 10%. It’s technically legal. The reason is loopholes.

Weak Laws

When companies cross the line, it can be extremely difficult for the CRA to successfully prosecute, due to weak rules on profit shifting under Canadian law.

Lack of transparency on beneficial ownership also creates problems with tax enforcement. Companies can be registered federally or in any of the 10 provinces and three territories. But fewer than half of these jurisdictions require companies to disclose beneficial ownership information.

Indeed, according to the U.K.-based Tax Justice Network, Canada is the 17th most secretive country in the world when it comes to financial information. Canada is ahead of two well-known tax havens, the British Virgin Islands and Mauritius at 19 and 20. According to the Tax Justice Network, financial secrecy is the refusal to share information with legitimate authorities such as tax agencies and the police.

This secrecy makes it easier to move wealth offshore without fear of probing questions from the CRA. The CRA has received a treasure trove of information about Canadian tax cheats using offshore banks to hide their money. The data arrived courtesy of the U.S., France and other governments, who acquired it from whistleblowers. In all there were more than 2,000 Canadians on these lists.

The first, arriving in around 2007, contained the names of 106 Canadian clients of a private Liechtenstein bank with more than $100-million in assets. None of the tax dodgers was prosecuted. Instead, the agency relied on its voluntary disclosure program under which tax payers can avoid prosecution if they agree to disclose foreign holdings and pay the taxes owing.

In his report to parliament in the spring of 2013, Canada’s Auditor General revealed that the CRA conducted only 46 audits of the account holders — less than half the 106 names on the list, for total reassessments of $24.7-million. But there’s a big difference between sending out a tax bill and actually collecting the money. What’s not known is how much of that $24.7-million was returned to the people of Canada.

The Auditor General advised that lists of offshore bank customers are “a new audit area” for the CRA but “it is not prepared for the growing workload.”

More recently the CRA has received similar lists of Canadian account holders at London-based HSBC, UBS and Credit Suisse. The HSBC list alone contained 1,784 Canadians.

Senator Percy Downe, an advocate of tougher enforcement of tax rules, noted that the CRA took about six years to complete its audit process on the Liechtenstein list, and at that rate it will take just over 118 years to deal with the HSBC list.

Australia, which has taken a more aggressive approach to the offshore lists, has already collected more than $750-million from tax dodgers and publicly charged more than 73 of them, according to Downe.

Taken together, these anecdotes suggest that the CRA is hampered not only by massive loopholes in tax legislation but also by a government that seems happy to turn a blind eye to tax evasion.

Despite the Auditor General’s carefully chosen words, the tax authority is for all practical purposes unable to cope with well-resourced tax dodgers. Instead of doubling down, it is focusing its efforts on those least likely to mount a defense: small mom-and-pop businesses, the self-employed and the middle class.

Federal and provincial governments have been promising to review and revamp the loophole rabbit-hole for many years urged on by academics, professional accounting organizations, and tax fairness advocates. With a few exceptions, there has been little headway. That indecision costs Canada more than $20 billion annually.

Trust, Innovation and Ethics

The men and women who spoke with us are experienced public servants. They thrive in a profession that places a lot of emphasis on rules and process. They have signed on to a crusade where everyone is supposed to pay their fair share. But many felt they have been cannon fodder in a war on public servants.

“They’ve created an environment where employees are so worried about losing their job that they fear they might make waves if they push too hard on files.”

Where they were once encouraged to use their knowledge and trust their judgement, they now have cases assigned to them based solely on computer algorithms.

Where they were once respected for their commitment to public service, they are now subject to surveillance of near Orwellian proportions.

Employees are subject to standard criminal and police record checks. But it has gone beyond that.

"Security regulations have changed massively. They look at the internet to see if you’ve said anything negative about CRA or the government. I know people who were fired for saying the wrong thing. Everybody feels like they're being probed or they're guilty of something, or their bosses are looking for something. It's not a good environment."

Ethics and safeguards are of particular importance in an area of the public service that deals with money and power. But such treatment does much to explain the concerns and morale on the front lines.

RECOMMENDATIONS

Seven immediately doable measures

This inside look at the Canada Revenue Agency is by no means comprehensive or scientific. But it is the first time that anecdotal evidence from inside the CRA has been publicly presented.

It outlines the undermining of the work of key CRA professionals and the subsequent costs and consequences to us all. It will require the Liberal government to follow through with its promises for the CRA. But as is evident, the solution goes well beyond those promises.

It will take consultation, creativity and political will to change the status quo. History teaches us the consequence of ignoring calls for fair taxation. Canadians can deal with it now or they can deal with it later.

1. Boost Capacity

Canadians would get a good return on their investment by boosting the CRA’s capacity. Canadians for Tax Fairness estimates that spending an additional $50 million a year would raise $1 billion annually. Historical experience backs this up. In 2005, the Liberal government invested an additional $30 million for increased enforcement. This resulted in an additional $2.5 billion over 4 years. Australia, France and U.S. have achieved good results from enhanced enforcement efforts targeted at tax haven related tax evasion.

2. Prioritize and prosecute

“We don’t go after the high rollers, we go after the easy stuff. That’s because the mandate is to collect X dollars so you go for the easier stuff.” More revenue can be recovered from a few big tax cheats than going after many small time tax cheats. The CRA needs to develop and publicize a comprehensive, multi-year plan for going after offshore tax schemes. This will require a change of priorities and more efforts in training and assigning experienced staff. It also requires a boost in capacity at the Department of Justice. Prosecuting more cases will create a greater deterrent than the current situation. Even when the CRA uncovers a scheme, tax cheats can settle out of court or take advantage of the Voluntary Disclosure Program. There are no punitive fines.

3. Investigate complex cases

Tax havens, profit shifting, double-non taxation – this is not the tax landscape of a few decades ago. CRA is losing experienced staff and needs to create a robust system and the political will to deal with 21st century challenges. The United States’ Internal Revenue Service has developed a reputation for recruiting and providing ongoing professional training for auditors and investigators.

4. Close Loopholes and Fix Laws

Raising the corporate or top tier tax rates is ineffective if those Canadians are availing themselves of a multitude of tax loopholes. And that is exactly what is happening. Canada has the lowest corporate tax rate in the G7 (27% avg) – but only four of the top 60 publicly traded corporations paid 25 per cent tax or more between 2007 and 2011. More than 30 of them paid less than 10 percent. A good beginning would be to amend corporate tax rules to require that offshore subsidiaries have a legitimate economic reason to be considered as a separate entity for tax purposes.

This was proposed during the last Parliament by Bill C-621, An Act to Amend the Income Tax Act (Economic Substance). It would make it easier to convict corporations using offshore subsidiaries to shift profits. Deterring this single practice could increase revenue by an estimated $400 million. One respondent put it this way: “It takes more than just the CRA to achieve fairness. You need the Department of Finance, you need the Tax Court of Canada. You need the businesses themselves, the lobby groups, the politicians.”

Other tax loopholes exist that mainly benefit the wealthy. These include such as the Stock Option Deduction, current treatment of capital gains income, the business entertainment tax deduction, income splitting for families. They make the tax system unfair. They also complicate tax filing and enforcement. Taxpayers and the CRA would benefit from a simpler and fairer tax system.

5. Produce a Tax Gap Report

Half of OECD countries produce a tax gap report to assess how well they are doing in collecting the taxes they are owed. Tax gap also identifies revenue lost due to tax evasion. It is a solid tool to prioritize enforcement efforts. Previous CRA ministers have refused to cooperate with the Parliamentary Budget Office to develop a Canadian Tax Gap. Much of the groundwork has already been done by the PBO. It is time for the government to direct the CRA to provide the information needed to finish the job. The result would be easier identification of problems with evasion and collection. It would also help prioritize resources effectively.

6. Bring the KPMG aggressive tax planning case to court

The CRA has gathered strong evidence that mega-accounting firm KPMG facilitates tax evasion by setting up off-shore accounts to help wealthy individuals hide their wealth from the CRA. This situation is not unique. The Canadian government should proceed with the court case that had been stalled for three years. It sends a strong signal to players in “wealth management”, accounting, and banking. The U.S. government has been assertive in going after “facilitators”. It has convicted and fined KPMG $500 Million in a similar case. The super-rich and multinationals have relied on these facilitators. This sends a message to stop.

7. Lead global efforts to tackle tax havens and reform corporate tax rules.

Much can be accomplished in Canada to stem profit shifting and the flow of tax dollars to tax havens. But ultimately global solutions are needed. The Canadian government has lagged, not led, in global corporate tax reform and transparency rules to curb tax havens. It is time for Canada to lead in these global efforts, including championing tax justice in developing countries. Canada has much to gain from stricter international corporate taxation rules. At least $23-billion in profits that should have been declared in Canada were shifted to tax havens. While Canada loses massive amounts of revenue, it is poor countries that are hardest hit with little influence in determining tax rules. With diminishing flows of aid dollars, developing countries are desperate for reforms that can manifest tax revenues to tackle poverty and inequality.

The OECD BEPS process has moved us several steps forward. But results are limited. Some of the most promising initiatives, such as the Country by Country Reporting, would not benefit many developing countries because the information will not be available to them unless they have tax information sharing agreements with the governments where multinationals are headquartered. While some of the larger developing countries that are represented in the G20 have these arrangements in place, many medium sized and smaller countries do not. BEPS reforms do not deal with the problems of the arm’s length rule, which is difficult to enforce and has undermined Canadian government attempts to challenge corporate profit shifting. The BEPS process has failed to address the urgent challenge of digital economy taxation. We urge that Canada champion the interests of developing countries on tax justice issues in global fora.

Ultimately we would recommend that the UN take on the effort to negotiate a multilateral tax treaty that would implement unitary taxation for multinational corporations. Only the UN can ensure effective participation in decision-making by developing countries.

Copyright 2015 by Canadians for Tax Fairness