Summary

Canada is being marketed to transnational tax-dodgers and criminals as a great place to incorporate shell companies for tax avoidance schemes. Russian ads, for example, suggest using Canada’s positive global image to “use more complex structures” and “completely legally optimize taxes.”

Tax dodgers, including Russian oligarchs linked to Vladimir Putin, know that Canada is actually weak on financial crime, and our financial transparency laws haven’t kept pace with changes in global finance. These schemes have no economic benefit to Canada, and our upstanding reputation is simply being used to deprive other countries of their own tax revenue.

Canadian entities are attractive as shell companies because:

- Private companies can be owned anonymously.

- They can be set up and run from abroad with no concrete ties to Canada.

- There is no oversight, such as requirements to file financial reports or tax declarations, or even submit ID, and none of the information disclosed is independently verified.

Recommendation: Fast-tracking of Canada’s proposed beneficial ownership registry, scheduled for 2025, and for quickly establishing provincial ownership registries, since most companies are registered at the provincial level.

Report

[This report was originally published on the website of Transparency International Canada, in collaboration with Publish What You Pay Canada. Our three organizations collaborate as The End Snow-Washing Coalition to fight tax-dodging, money-laundering, corruption and financial crime.]

1. INTRODUCTION

Canada enjoys a positive global reputation as a stable, affluent democracy with strong rule of law. Yet it is also among the most opaque jurisdictions when it comes to the ownership of companies and partnerships. Ownership information is not public and entities can be set up and controlled from abroad. Some entities have no reporting requirements or domestic tax obligations, yet they can hold bank accounts and enter contracts. These structures are particularly attractive to bad actors in need of fronts for their misdeeds. As a result, Canada has become a sought-after place to incorporate shell companies.1

A cottage industry of consultants - many with no apparent links to Canada - has emerged promoting Canadian entities as fronts for opaque offshore company structures. Framed through the lens of ‘tax optimization,’ these structures appear intended to conceal ultimate ownership and leverage Canada’s strong reputation to access the global financial system.

Excerpts from offshore consultant websites

- ‘Canada is a new player in the world of offshore companies ... it has no negative offshore reputation and no association with tax avoidance or evasion. It is by far one of the best neutral jurisdictions, providing offshore benefits without any of the traditional offshore drawbacks.’2

- ‘A Canadian company can be used to act on the behalf of offshore companies or can be used to receive and remit money to offshore companies to avoid with- holding taxes...’3

- ‘Canada LLP - A Tax-Free and Highly Reputable Offshore Company’4

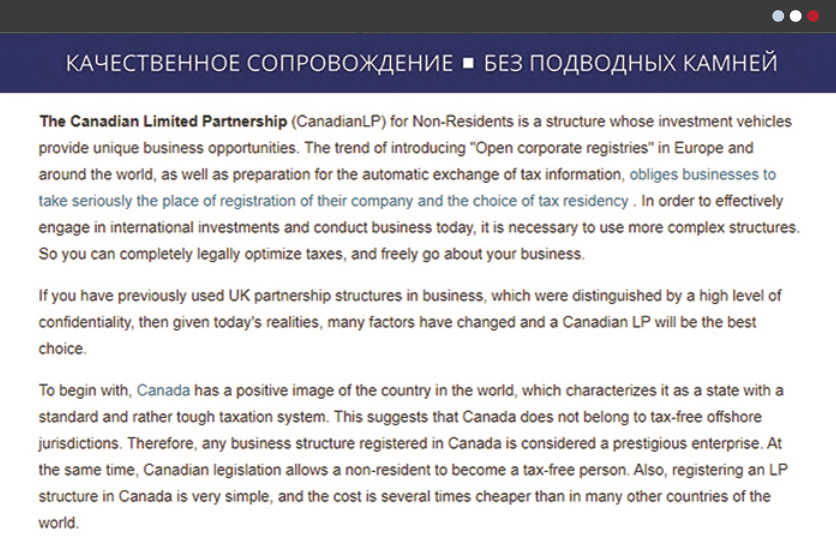

- ‘If you have previously used UK partnership structures in business, which were distinguished by a high level of confidentiality, then given today’s realities, many factors have changed and a Canadian LP would be the best choice.’5

These offshore consultants promote Canadian entities as ‘flow-throughs’ whose value lies in their Canadian identity, which serves as a cover for offshore structures. These shells are unlikely to generate much if any tax revenue or local employment, and may not have any economic benefit to Canada beyond the nominal fees charged by the government to incorporate them and renew their registration.

In the absence of open company data, it is impossible to know just how widespread the use of Canadian shells has become. Canada’s corporate registries are antiquated and have limited search functionality, and the companies they administer disclose little about themselves. In order to demonstrate how a transparent registry can be used to investigate wrongdoing, we used the UK’s open data on companies and beneficial owners to flag instances where Canadian entities were used in suspicious corporate structures. Among the Canadian entities in the UK’s beneficial ownership registry are: a group of Albertan Limited Partnerships that media and experts claim form part of a complex web of shell companies used to launder billions of dollars from Eastern Europe; a BC Limited Liability Partnership fronted by a prolific nominee whose companies have been identified in media reports as having been used to commit fraud and channel bribes; and two Quebec companies linked to dubious oil deals in post-Soviet states.6 These cases, identified through another country’s beneficial ownership database, are likely just the tip of the iceberg.

Companies and partnerships are powerful tools with many legitimate uses. With some relatively simple reforms, we can strip them of the attribute that appeals most to bad actors: their anonymity. It begins with collecting beneficial ownership information and making it available to the public in an open data format. This must be accompanied by changes to company law to require resident directors, identify nominees and those they represent, and verify the data submitted to corporate registries. We must also deter bad behaviour through sanctions and enforcement.

Open data allows journalists, civil society and other stakeholders to investigate wrongdoing. This is particularly important for Canada, where law enforcement and regulatory authorities have limited capacity to investigate domestic crime, let alone criminal activity beyond our borders.7 Transparent company data also enables law enforcement and regulators to conduct investigations more effectively, without cumbersome mutual legal assistance requests or the risk of tipping off the very entities they are investigating. Beyond that, it makes due diligence more effective and helps reporting entities8 meet their compliance obligations.

Canada has long been perceived as weak on financial crime.9 Encouragingly, however, the federal government recognizes these risks, and in April 2021 proposed to implement a public beneficial ownership registry over the next four years.10 This is a significant development, and it is vital that the provinces and territories now follow suit. It is time for a unified approach to deter money laundering and transnational organized crime and address the threat snow-washing poses to Canada’s hard-fought reputation for integrity and fairness.

2. WHAT IS SNOW-WASHING?

The term “snow-washing” refers to the misuse of Canadian legal entities to commit financial crime, by concealing suspect transactions under the cover of Canada’s reputation for financial integrity.11

While snow-washing has only been reported on since the Panama Papers scandal broke in 2016, it is not a new phenomenon. In an investigation by The Toronto Star and CBC-Radio Canada published in January 2017 under the title, “Snow Washing: Canada is the world’s newest tax haven,” reporters found more than two dozen corporate service providers outside Canada that promoted Canadian companies “as vehicles to avoid tax in a reputable ‘offshore destination’”.12 Among those service providers was the disgraced Panama-based firm, Mossack Fonseca, which began to promote Canada as a tax haven in 2010.13 As this report shows, little has changed since then, and there are still many dubious service providers that pitch Canadian entities as fronts for offshore company structures.

Global efforts to deter financial crime have tarnished many ‘traditional’ offshore jurisdictions (ones that conjure up images of sleepy tropical islands and bank vaults in the Alps) putting up hurdles for those jurisdictions to access the global financial system through stigma and regulation. Tax haven and money laundering blacklists published by public bodies such as the European Union14 and the Financial Action Task Force (FATF)15 inform risk management processes at financial institutions, which subject customers from those jurisdictions to greater scrutiny or ‘de-risk’ them by closing their accounts.16 This has made it expedient to have entities in perceived low-risk jurisdictions - such as Canada - that can serve as fronts for offshore networks.

Bad actors have identified Canada as one country where they can exploit a wide gap between perception and reality. Canada enjoys a reputation as an affluent and stable country with good governance, robust democracy and rule of law.Yet it is also among the most opaque jurisdictions globally, where it is possible to set up and operate companies from abroad with little risk of being held accountable for wrongdoing due to vast shortcomings in Canada’s financial crime detection and enforcement mechanisms.17

3. WHAT ARE SHELL COMPANIES?

Shell companies are entities that carry out no discernible business activity and have no public information on who ultimately controls them. Like empty shells, there is nothing inside. They merely exist on paper.

Laundromats are professional money laundering operations comprising vast networks of companies under common ultimate control, which transfer money between one another to conceal its origins.

Financial crime is booming, facilitated by readily available legal structures that provide cover for perpetrators and enable them to launder their ill-gotten gains.18 Almost every financial crime involves the use of corporate vehicles.19 Anonymous companies are valuable tools for criminals because they can be used as cover to conduct business, buy and hold assets, and use the financial system. Many jurisdictions, including Canada, make it easy to set up a company without disclosing any details that could trace it back to the individual controlling it. Companies can exist only on paper, with no business operations or presence in the real world. These ‘shell companies’ have been dubbed the getaway cars of financial crime, as it is extremely hard if not impossible to track down the people behind them.20

As the head of the FATF, a multilateral institution and the architect of the global anti-money laundering regime, put it in a 2019 op-ed: ‘The shell company set-up often attracts criminals. Yes, many companies, foundations and associations with several layers of ownership are legitimate and legal. But secretive shell companies, or those with complex ownership structures, frequently allow drug dealers, arms traffickers and corrupt politicians to hide their ownership and conceal their ill-gotten gains ... Shell companies enable serious crime that harms society.’21

Those looking to conceal criminal activity can use shell companies to form complex corporate structures with layers of ownership spanning multiple countries. Doing so makes it harder to investigate and pursue legal action, and takes advantage of jurisdictional constraints facing law enforcement and regulators.

As one provider promoting Canadian Limited Partnerships to Russian clientele explains: ‘The future of offshore business lies in and depends on application of more complex and thoughtful structures, using not only classic offshore, but also midshore, as well as completely onshore entities, so that the situation of incriminating in relations with offshores and legal optimization of taxes does not cross even the most meticulous tax inspector’s mind.’22

An example of this type of hybrid offshore-onshore structure is included below, taken from an investigation by the Organized Crime and Corruption Reporting Project (OCCRP) into an alleged ‘laundromat,’ or large-scale money laundering operation. According to OCCRP’s investigation, some US$2.9 billion was channelled out of Azerbaijan between 2012 and 2014 using shell companies and their bank accounts at the Estonian branch of Danske Bank.23 Some of the funds were then used to acquire assets in the West and pay lobbyists and European political figures as part of a campaign to improve the international image of its regime.24 The apparent front company, a Scottish Limited Partnership (LP), has three tiers of ownership that ultimately end in offshore secrecy havens.

Embedded in that ownership structure is an Albertan LP, whose sole partner is a company registered on the island of Nevis - which has been described as ‘the world’s most secretive offshore haven.’25 Corporate records show that the Nevisian company is the parent of at least two entities in the structure (possibly more - the others are based in opaque offshore centres that do not disclose ownership information), suggesting the whole network is likely under common control. There are at least 20 other companies controlled through this specific structure. The ultimate beneficial owner, whose identity/ies remain hidden, could – in theory – use this diffuse network of entities to move money and obscure the source of funds, while avoiding the scrutiny of tax authorities and investigators.

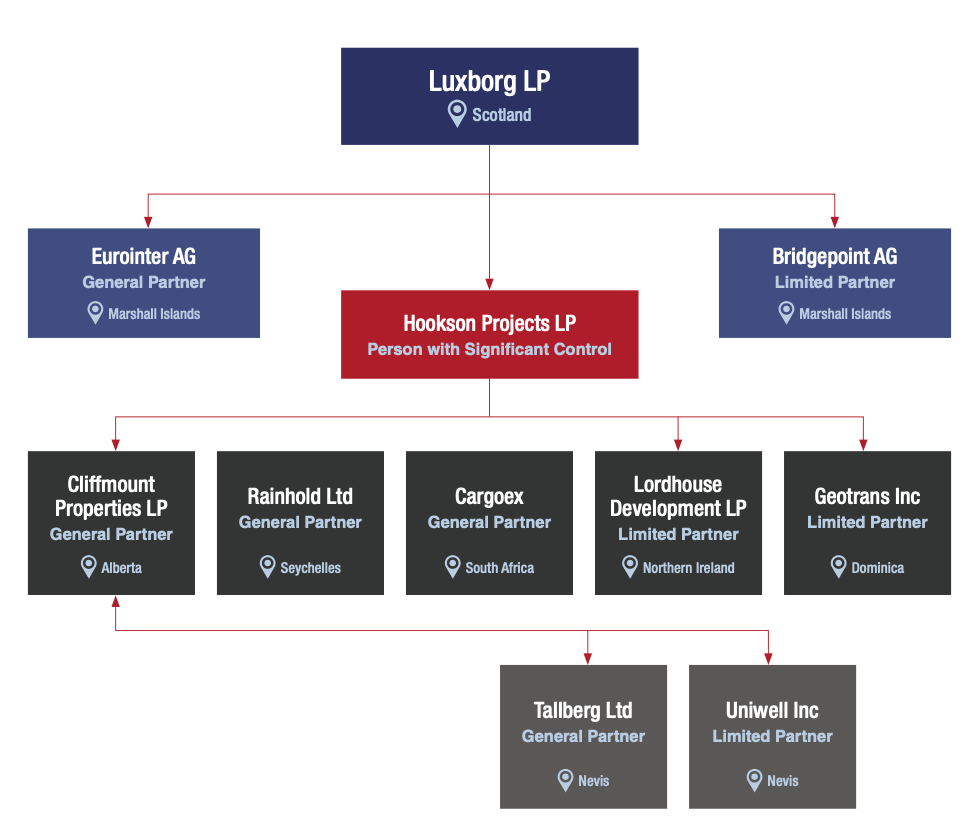

In evidence submitted to the Commission of Inquiry into Money Laundering in British Columbia (the ‘Cullen Commission’), financial crime expert Graham Barrow explained that he had found ‘dozens’ of other UK entities that “have utilised Canadian Limited Partnerships to obfuscate their ownership chain”.26 Barrow’s evidence included a structure chart, an adapted version of which is included below, that shows the chain of control for one Scottish LP used in the alleged laundromat network:

The structure chart provided above is adapted from evidence submitted by AML compliance specialist Graham Barrow to the Cullen Commission. The diagram depicts a small part of a vast network of shell companies used in a transnational laundromat.27 The chain of control in the diagram goes from top (subsidiaries) to bottom (parents), with each colour representing a different layer of ownership.

4. THE CANADIAN SHIELD: CONCEALING OFFSHORE NETWORKS

In contrast to offshore jurisdictions with large corporate services industries seeking to attract clients to their shores (often with the backing of their governments28), Canada’s emergence as a secrecy jurisdiction has not been by design. Rather, our corporate structures are being exploited because we have failed to update laws to keep pace with changes in global finance.

There are a few key characteristics that make Canadian entities attractive as shells:29

- Private companies can be owned anonymously. In most Canadian jurisdictions, there are no requirements to disclose the identities of shareholders or partners.30 There is no beneficial ownership disclosure.31 There are no rules barring nominees or requiring them to disclose that they are acting on behalf of someone else.

- They can be set up and run from abroad. Many Canadian jurisdictions do not require a resident director or partner. Entities can be formed and administered from abroad with no concrete ties to Canada. In some jurisdictions, partnerships only require one partner, which can be an offshore company.32

- There is no oversight. There is no requirement to file financial reports, and many entities do not need to file annual returns or tax declarations.33 Individuals associated with Canadian entities do not need to submit ID, and none of the information disclosed is independently verified.34

Though many Canadian entities exhibit these traits, one structure in particular - the Limited Partnership (LP) - appears to embody all of them. LPs have fewer reporting and disclosure requirements than most other entities in Canada, and unless they do business in Canada they need not engage with the tax authorities. They can also be established cheaply without any need for their owners or administrators to set foot in Canada or be represented by a Canadian. And crucially, although LPs are not considered legal persons in Canada, they can nevertheless be used to open bank accounts and conduct business transactions. These characteristics, and the cover of Canada’s international reputation, might present ‘unique business opportunities,’ to anyone engaging in such jurisdictional arbitrage, as the advertisement below ambiguously suggests, but it also makes Canadian LPs particularly vulnerable to exploitation for transnational financial crime.

Translated Russian-language advertisement for Canadian LPs:35

5. THE INTERMEDIARIES

In some places it is possible to set up a company directly with the registry - this is true of many Canadian provinces - but it is often necessary and much more convenient to use an intermediary. These corporate service providers, also known as formation agents, receive orders from clients, file the official paperwork and pay the fees to create a company.36 Many provide ongoing administrative support and complementary services such as registered addresses, mail forwarding, secretarial services, and serving as nominee directors or shareholders. The industry is varied - it includes large wholesalers, law and accounting firms, and an array of small consultancies and sole traders.37 Some are discerning and uphold high standards of record-keeping and know-your-client due diligence, while others are all too willing to provide cover to all sorts of unsavoury clients.38

Some providers set up thousands of companies each year and their nominees hold hundreds or even thousands of appointments.39 It is practically impossible for those appointees to know the details of the companies they are managing, despite having a duty to remain informed.40 Whether they are complicit or ignorant, nominees can stymie efforts to investigate the controlling minds behind shell companies used for wrongdoing. Those looking for anonymity can hire a nominee for as little as a few dollars a day.

Many corporate service providers also provide registered addresses for their clients - often nothing more than a brass plaque or post office box. There are, of course, many legitimate uses for this service, though it is also vital to those concealing crimes through anonymous shell companies. Data leaks from offshore financial centres and analysis of the UK’s open corporate registry have made it possible to identify numerous ‘company factories’ - properties that house tens or hundreds of thousands of entities - which have served as the registered addresses of shell companies used for crimes ranging from fraud to arms trafficking to grand corruption.41 Company factories are particularly useful for laundromats, as having common addresses and nominees streamlines the paperwork and administration required to keep networks of hundreds of companies running.

In Canada, there does not appear to be a proliferation of company factories as in the UK, some US states, and offshore centres. Though little research has been done in the area, available sources suggest that Canada’s most active company service providers and registered addresses are linked to law firms.42 Unlike administration agents in some other jurisdictions, members of the legal profession in Canada have ethical standards to uphold and are expected to comply with know-your-client due diligence obligations. However, lawyers are exempt from statutory anti-money laundering (AML) reporting and services they provide to clients are generally protected under solicitor-client privilege, which the FATF and other financial crime specialists have argued leaves a gaping hole in Canada’s financial crime defences.43 Academic studies and undercover investigations from the US have shown the willingness of some lawyers to help clients conceal their identities behind shell companies.44 While the federal government and law societies have been working on a ‘constitutionally compliant’ solution to this problem for several years, it is unclear how much progress has been made beyond allowing the legal profession to self-regulate.45

6. INTERMEDIARY ADVERTISEMENTS

We conducted some basic online research and found a cottage industry of corporate services providers and self-styled tax consultants touting Canadian entities as fronts to provide cover for blacklisted offshore jurisdictions.46 Nearly all of the service providers we identified are located abroad and have no apparent links to Canada beyond the shells they are promoting. They are a diverse group, covering an array of jurisdictions and languages, yet their sales pitches all focus on the same key point: Canada is a reputable high-tax jurisdiction whose opaque entities can provide valuable cover for offshore companies that would otherwise attract unwanted attention.

Excerpts from offshore service provider websites:

- ‘Canada, as a high taxation country, is not a bad front at all, it is actually a very useful cover for almost all types of offshore companies..’47

- ‘Even though the image of an offshore company has taken such a battering over the years, this does not mean that an offshore company is all but useless ... but keeping a low profile is essential. Whilst the minute legal details call for specialist knowledge, the underlying idea is usually simplicity itself - it involves the use of a respectable onshore company to front transactions.’48

- ‘Canada is the most preferable destination for compliant tax planning since it has no negative offshore reputation and no association with tax avoidance or evasion. It is by far one of the best neutral jurisdictions, providing offshore benefits without any of the traditional offshore drawbacks.’49

- ‘Canada has become one of the ideal places for registration of Limited Partnerships... Canadian Limited Partnerships are a convenient, profitable and prestigious tool for doing business, which helps alleviate not only tax but also paper and documentary burdens.’50

For clients that are particularly concerned about anonymity, many of the service providers will act as nominee directors and shareholders,51 and some propose opening bank accounts for clients.52

The providers all frame their services through the lens of ‘tax optimization,’ with firms pitching aggressive tax avoidance schemes that, in at least one case, seem to push the limits of legality.53

Some regional differences were also identified, with some Chinese intermediaries pitching Canadian entities as a tool to skirt state currency controls54 and European providers describing how they can be used to avoid value added tax (VAT) obligations.55

Quotes:

- “Prestigious jurisdiction not ‘blacklisted’ anywhere”56 “Canada offers a high level of anonymity and privacy”57

- “attract less attention”58

- “Canada will not be considered as an offshore company ... No disclosure of beneficial ownership to authorities”59

- “Canadian companies have no tax heaven [sic] image and can be used as a well-respected instrument in international business”60

- “What are the nice things about an LP registered in Canada? Firstly, such LP’s are less popular than those registered in England or Scotland, and thus they attract less attention.”61

7. THE POWER OF AN OPEN REGISTRY: CASE STUDIES USING UK DATA

Due to the opaque nature of Canadian corporate registries, it is currently impossible to ascertain how widely Canadian shell companies are used as fronts for offshore networks, as the service providers in the previous section advertise. In the absence of Canadian data, we analyzed corporate and beneficial ownership data from the UK’s Companies House registry to identify cases where Canadian entities feature as part of transnational corporate structures with a UK nexus. We found multiple examples of these structures, including several that appear to have been used for dubious and potentially illegal purposes. Of course, this analysis only sheds light on a tiny subset of Canadian entities - ones that are used to control or direct UK companies or partnerships. One can only assume that similar structures exist using Canadian entities and other jurisdictions.

With open data we were able to filter the registry to identify entities with a Canadian address. Corporate registries often only make a few search functions available, so this analysis would not have been possible in many other jurisdictions (including across Canada).62

Canadian companies linked to alleged transnational laundromat:

“In money laundering it’s called layering. It’s having this incredibly complex structure which makes it really hard to prosecute - not only in terms of which country should do it, but it’s also really hard to get your head around what is going on”

- Graham Barrow, money laundering investigator and UK shell company expert63

Various media outlets have reported on what they describe as an industrial scale transnational laundromat that has been used to move billions in dark money out of Russia and the former Soviet Union. The network has Canadian connections, according to analysis of corporate records and reporting by the Globe and Mail, which identified six Alberta-based limited partnerships forming part of this system of interlinked companies.64 The network, which is alleged to have been managed by a group of intermediaries based mainly in Latvia, reportedly used a multitude of interlinked shell companies with bank accounts in Baltic states to hide the proceeds of tax fraud and obscure the source of bribes, among other crimes.65 It is reported that the network included structures fronted by UK entities, which had several layers of ownership that ultimately led to opaque offshore locales such as St Kitts & Nevis, the Marshall Islands and the Seychelles.

The six Albertan LPs sat directly above the UK fronts and seem to have been used to add another layer of complexity to the structures and circumvent beneficial ownership disclosure rules.66 Scrutiny by journalists and financial crime investigators suggests that the Alberta LPs are a key part of the laundromat’s infrastructure.

The Six Alberta LPs of the Russian Transnational Laundromat 67

• Yardmile Development LP is the general partner of a Scottish LP named Wallbridge Logistics LP (which itself controls 39 UK shells in the network and was cited by TI-UK and news outlet OpenDemocracy as an example of UK entities being used to conceal ownership68).Yardmile’s general partner is a shell company registered in the Marshall Islands, Bondwest AG, whose signatory claims that his identity was stolen and used to administer hundreds of companies in the network without his knowledge.69

• Cliffmount Properties LP is the general partner or shareholder of several UK entities in the network, which themselves act as partners or shareholders for dozens of entities in the laundromat.70 The general partner for Cliffmount Properties is a Nevis-based shell, Tallberg Ltd. Cliffmount Properties was cited by Graham Barrow as an example of Canadian shell companies featuring in ‘laundromat style company formations’ that was submitted as evidence in the Cullen Commission (see previous section).71

• Webholm Merchants LP is the general partner of Fortshield Inter LP, a Scottish LP that directly controls at least 34 other entities within the network.72 Albertan company records show that Webholm Merchants’ general partner is Tallberg Ltd, the Nevis shell that also controls Cliffmount Properties, whose signatory claims that his identity was stolen to administer these companies. Tallberg Ltd was also the former general partner of Fortshield, suggesting that the Albertan LP may have been added as a layer of obfuscation (as the ultimate control remained unchanged).

• Quadrotop Services LP and Edoran Services LP are the general partners of a UK partnership called Craftberg Consulting LLP. The supposed beneficial owner of Craftberg is Martins Rauda, a Latvian nominee associated with numerous shell companies in the laundromat, according to reporting by the OCCRP and others.73 Albertan company records list Martins Rauda as the general partner of both Quadrotop Services and Edoran Services.

• Telford Alliance LP serves as the secretary for Investexpress Ltd, a company whose directors have included two offshore shells (based in Cyprus and Nevis) and two individual nominees implicated in the alleged laundromat network.74 The Nevis shell was the company’s sole shareholder until 2017, when disclosure rules changed and the company stopped reporting shareholder information. Since then, Investexpress has identified a woman based in Tashkent, Uzbekistan, as its beneficial owner. Albertan company records show that Telford Alliance’s general partner is a Marshall Islands-based shell called Dartwill Ltd.

BC partnership controlled by dubious formation agent

We identified a BC-registered limited liability partnership called 3A Business Consultors LLP (3ABC LLP) as the beneficial owner of 10 UK-registered companies. The LLP was set up by a corporate ser- vices provider called TBA & Associates (TBA), which promotes Canadian entities on its website as ‘highly prestigious’ vehicles that ‘can be used as a nominee shareholder for other companies around the world.’75 3ABC LLP appears to have filled this role; it was set up in April 2017 and served as the sole shareholder of the 10 UK companies formed in September 2017.76

3ABC LLP and the UK entities were all listed for sale as shelf companies on the TBA website, at prices ranging from £1,335 to US$2,925 (C$2,315 - C$3,670).77

Unlike the transparent UK entities, 3ABC LLP is practically untraceable. Under BC’s opaque rules, the identities of its partners are not disclosed and the entity is registered to a post office box in a UPS Store.

The LLP’s registration documents and annual returns are signed by Joaquim Magro de Almeida, a prin- cipal of TBA who serves as a nominee for hundreds of companies spanning opaque jurisdictions such as Belize, Cyprus, Delaware, Estonia and the Seychelles, as well as countries like Canada, New Zea- land and the UK, which until recently have avoided much of the stigma associated with secrecy jurisdic- tions, becoming valuable fronts for offshore networks.79

TBA has formed and maintained hundreds if not thousands of entities, many of which have been used for legitimate business. However, some of those companies have been linked to alleged or proven criminality, including a Ponzi scheme targeting Asian investors,80 an Australia- based investment fraud,81 a suspected tax fraud by an Indian chemicals group,82 and a multimillion-dollar bribery scheme in Saudi Arabia involving a Spanish military supplier.83 Almeida has also set up and administered a company that runs extreme pornographic websites, which he also registered on behalf of the anonymous owners.84

Finally, a TBA affiliate, operating under the ‘Atrium’ brand name,85 posted profiles on its website of what appear to be fictitious executives whose bios and photographs were lifted from other websites. Reverse image searches identified the real people whose photographs were used by Atrium, none of whom appear to have connections to the business.86

Given the opportunity to comment ahead of this report’s publication, TBA - through an individual identifying himself as TBA’s Compliance Officer, George Hamilton87 - wrote that “all your information is untrue, improper and incorrect”, but did not address any of the specific allegations set out above. TBA followed up stating “All client due diligence and analysis properly processed whenever an order is received and placed by any client, whoever, and no responsibility or liability can fall upon us in case of any eventual illegal action or procedure by those and respective clients...”. TBA’s representative also noted that the firm is registered as a Trust and Corporate Services Provider and is overseen by the UK tax authority’s Anti-Money Laundering supervision scheme.88

Shelf companies are shell companies that have been incorporated and maintained for years in order to give the appearance that they are operating businesses. As one vendor advertises: “The older a shelf company is [the] more credibility it will offer you!”

Canadian shells linked to suspect oil deals in post-Soviet states

Analysis of the UK Companies House data identified several other Canadian shell companies that may have been involved in corrupt schemes. These include the supply of fuel additives to a Russian state- owned oil company by a firm apparently controlled by one of its top executives; and the sale of a fuel storage facility in Kazakhstan owned by the daughter of Nursultan Nazarbayev, the kleptocratic former president.89 As with the other schemes identified in this report, these used the Canadian entities as fronts for offshore shells.

One might reasonably ask why oil deals in former Soviet states would involve intricate shell structures leading from the UK to Canada to offshore, if not to obscure the transactions and those benefiting from them. That remains an open question, however, as despite an abundance of red flags90 we could not definitively demonstrate wrongdoing.

8. THE ANTIDOTE: TRANSPARENCY

Financial crime depends upon opacity. Its mechanisms need to stay hidden from public view in order for it to thrive. This is why cross-jurisdictional corporate structures such as those detailed in this report are such useful tools for criminals. They obscure ownership and transactions, and ensure that efforts to investigate are met with tangles of red tape or hit dead ends. Making legal entities more transparent is critical to the fight against financial crime and the damage it causes to society. We have long advocated for a publicly accessible registry of Canadian entities and their beneficial owners, which is a critical component in the fight against financial crime. The federal government took a big step earlier this year when it proposed in the budget a public beneficial ownership registry by 2025, for which it should be applauded.91

The devil will be in the details, as the saying goes, though there is helpful guidance to draw from as Canada’s registry takes shape. The particulars of what a registry should include are covered in our 2020 report, Implementing a publicly accessible pan-Canadian registry of beneficial ownership.92 It suffices to say here that the registry should include partnerships, and beneficial ownership disclosure must go beyond the immediate parents of Canadian entities to identify the people who ultimately control them. This includes identifying the people behind offshore entities that serve as shareholders or partners of Canadian entities.

Ottawa cannot go this alone. As this report shows, many shell companies are being registered at the provincial level. The federal, provincial, and territorial governments must work together to ensure that reforms are applied to the same high standards.

As well as rolling out a public registry of beneficial owners, we need to make several other changes to our company laws. These reforms must be introduced in conjunction with that public registry if it is to be effective in deterring the abuse of legal entities:

- Nominees should be required to disclose that they are acting on another’s behalf, and should identify that person.

- Companies should have at least one resident director to ensure that there is someone accountable within the jurisdiction.

- Partnerships should disclose their partners and file annual returns. They should also file declarations with the Canada Revenue Agency even if they have no taxable activities.

- Sufficiently dissuasive penalties should be introduced and enforced to deter false declarations and other non- compliance. Sanctions should apply to intermediaries as well as directors, officers, partners and beneficial owners. Enforcement should be prioritized to make up for years of inaction.

- Registries should be empowered to independently verify information, collect and securely store ID, and pursue cases of non-compliance. This can be paid for by marginally increasing the cost of registering and maintaining companies.

There is a clear global trend toward more transparency.93 As other jurisdictions enact reforms, Canada needs to move with speed and precision to make our companies less vulnerable to abuse. Doing so is vital to maintaining Canada’s robust international reputation and addressing persistent problems with tax evasion and transnational crime.

REFERENCES

1 In the context of this report, shell companies include partnerships as well as corporations.

2 https://web.archive.org/web/20210124095628/https://world-fiduciary.com/… (accessed March 25, 2021)

3 https://www.tba-associates.com/canada-incorporation-introduction/ (accessed March 25, 2021)

4 https://en.liberated.blog/business/tax-free-and-highly-reputable-biz/ (accessed March 25, 2021)

5 https://internationalwealth.info/offshore-company-formation/canadian-pa… (accessed and translated using Google Translate on March 25, 2021)

6 These case studies are expanded upon later in this report, with the relevant media articles and supporting evidence cited in endnotes 63 to 74, and footnotes 83 to 86.

7 “Ottawa, RCMP have yet to add resources in money-laundering fight, BC Attorney-General says”, Globe & Mail, November 23, 2020; “Casino investigation boss lacked confidence in RCMP financial crime unit”, Business in Vancouver, February 8, 2021; “The RCMP is shutting down its financial crimes unit in Ontario. Here’s why former top Mounties says it’s a mistake”, The Star, January 15, 2020

8 Organizations and individuals covered by the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA)

9 “U.S. is steps ahead of Canada in fighting financial crime, Globe & Mail, February 26, 2021; “Not just B.C.: Most provinces in Canada fail to secure convictions in money-laundering cases”, Global News, February 10, 2019; “Corruption and financial crime have tarnished Canada’s reputation”, CPA Pivot Magazine, April 27, 2020

10 https://transparencycanada.ca/news/civil-society-coalition-enthusiastic…- federal-budget

11 What is snow-washing?

12 “Canada is the world’s newest tax haven”, Toronto Star, January 25, 2017

13 “Canada is the world’s newest tax haven”, Toronto Star, January 25, 2017

14 EU list of non-cooperative jurisdictions

15 FATF High-risk and other monitored jurisdictions

16 OXFAM, “Understanding Bank De-Risking and its Effects on Financial Inclusion: An exploratory study,” November 2015; Council of Erope, “‘De- risking’ within MONEYVAL States and Territories”, April 2015

17 As documented in previous reports, Canada has a startlingly low conviction rate for money laundering and other financial crime offences. FINTRAC, Canada’s financial intelligence agency, gathers intelligence but lacks enforcement capabilities. Though thousands of intelligence reports are disclosed to law enforcement each year, police and prosecutors are ill-equipped for pursuing complex financial crime cases. Hurdles to successful prosecutions, such as time limits (R. vs Jordan) and until recently the Criminal Code requirement to link money laundering with a predicate crime, further impede enforcement efforts.

Transparency International Canada, “No Reason to Hide: Unmasking the Anonymous Owners of Canadian Companies and Trusts”, 2016; FATF, “Anti-money laundering and counter-terrorist financing measures: Canada Mutual Evaluation Report”, September 2016 (pp. 3, 31-36); Report of the Standing Committee on Finance, “Confronting Money Laundering and Terrorist Financing: Moving Canada Forward”, November 2018 (pp. 45- 54); Dentons, “Criminal Code changes affecting money laundering in Canada: What your company needs to know”, July 25, 2019.

18 COVID-19 and Emerging Global Patterns of Financial Crime; PwC’s Global Economic Crime and Fraud Survey 2020

19 OECD, “Behind the Corporate Veil: Using Corporate Entities for Illicit Purposes”, 2001

20 “Cracking the shells - The war on money-launderers’ vehicle of choice intensifies”, The Economist, June 29, 2019

21 “Anonymous shell companies are a menace to the financial system”, Financial Times, November 12, 2019

22 https://lawstrust.com/en/company-formation/canada-lp (accessed on March 10, 2021).

23 TI Canada has not independently reviewed the material used in OCCRP’s investigation but has trusted in its thorough editorial review process.

24 “The Azerbaijani Laundromat; OCCRP, The Influence Machine”, OCCRP, September 4, 2017

25 Oliver Bullough, “Nevis: how the world’s most secretive offshore haven refuses to clean up”, The Guardian, July 12, 2018

26 https://ag-pssg-sharedservices-ex.objectstore.gov.bc.ca/ag-pssg-cc-exh-… Involved%20in%20Global%20Laundromat%20Formations%202020.pdf

27 Graham Barrow, “Canadian entities involved in global laundromat style company formations”, submitted as evidence to the Commission of Inquiry into Money Laundering in British Columbia, December 2020

28 Oliver Bullough, “Nevis: how the world’s most secretive offshore haven refuses to clean up”, The Guardian, July 12, 2018

29 Canada comprises 14 distinct jurisdictions, which are not uniform in their requirements for forming and maintaining legal entities. A detailed

breakdown of the different types of entities in each jurisdiction is beyond what we can cover in this report, though it would be a worthwhile exercise.

30 Shareholders are disclosed for companies registered in Quebec and voting shareholders are disclosed for companies registered in Alberta.

31 In 2020, the BC Government began a phased implementation of its Land Owner Transparency Register, which includes beneficial ownership information on companies that own real estate in the province. Quebec has also recently tabled legislation that would require the disclosure of beneficial ownership information for companies registered in that province, though it is unclear at this stage whether that information will be made public.

32 https://www.blaney.com/articles/the-benefits-of-limited-partnerships-to…

33 Entities without any taxable business activity in Canada do not need to file with tax authorities.

34 Corporate registry staff in Canada do not collect ID for directors, officers or partners, nor do they check the veracity of information provided by applicants for new companies or partnerships.

35 https://internationalwealth.info/offshore-company-formation/canadian-pa… (accessed and translated using Google Translate on March 25, 2021)

36 Financial Action Task Force, “FATF Guidance for a Risk-Based Approach for Trust and Company Service Providers”, June 2019

37 “Company formation - Shells and shelves”, The Economist, April 7, 2012; “The incorporation business - They sell sea shells”, The Economist, April

7, 2012

38 Michael Findley and JC Sharman, “Global Shell Games: Testing Money Launderers’ and Terrorist Financiers’ Access to Shell Companies”, 2012; “The Panama Papers: Exposing the Rogue Offshore Finance Industry”, ICIJ, April 2016-February 2019

39 “#29LEAKS: Inside a London Company Mill”, OCCRP, December 4, 2019; “The Secret World Of Sham Directors”, Süddeutsche Zeitung, April 18, 2016; “Sham directors: the woman running 1,200 companies from a Caribbean rock”, The Guardian, November 25, 2012; “Panama Papers: Signatures for sale”, Toronto Star, January 26, 2017

40 Directors and officers - Corporations Canada; UK Companies Act 2006, sections 171-177

41 Transparency International, “Hiding in Plain Sight: How UK companies are used to launder the proceeds of corruption”, November 2017; Global

Witness, The Companies We Keep, August 2018; “How Delaware Thrives as a Corporate Tax Haven”, New York Times, June 30, 2012

42 Exhibit showing top incorporators of BC companies since 2010, Commission of Inquiry into Money Laundering in BC, December 2020; Exhibit showing top directors and officers of BC companies since 2010, Commission of Inquiry into Money Laundering in BC, December 2020. This research only appears to have been done in BC and may not be representative of other provinces and territories.

43 “Money-laundering investigators stymied by legal loophole”, The Province, August 8, 2015

44 Global Witness, “Lowering the Bar”, 2016 (In this undercover investigation, 12 of 13 New York law firms contacted by an investigator posing as an agent for a corrupt official provided advice on how to move money into the US without detection using shell companies.); Michael Findley and JC Sharman, “Global Shell Games: Testing Money Launderers’ and Terrorist Financiers’ Access to Shell Companies”, 2012 (This study found that only 35% of Canadian corporate service providers - primarily lawyers - were compliant with FATF standards on collecting ownership information.)

45 Assessment of Inherent Risks of Money Laundering and Terrorist Financing in Canada, Department of Finance Canada, 2015 (p. 32)

46 Research was conducted on Google and other mainstream search engines using combinations of keywords such as ‘shell company,’ ‘anonymous,’ ‘confidential,’ ‘tax evasion,’ ‘tax avoidance,’ ‘tax optimization,’ ‘offshore,’ ‘launder’ and ‘Canada’ or the names of Canadian provinces and territories. Searches were conducted in Chinese, English, French and Russian.

47 https://tax-free.today/blog/registering-a-business-in-canada/ (accessed March 25, 2021)

48 https://www.tba-associates.com/offshore-incorporation/new-offshore-solu… (accessed March 25, 2021)

49 http://www.trueoffshore.com/product/63/Canada+PLC (accessed March 25, 2021)

50 https://bizonaire.com/en/blog/article/all-about-canadian-limited-partne… (accessed March 25, 2021)

51 https://www.afinex.net/services/establishing-and-managing-companies-abr… (accessed March 25, 2021)

52 https://www.atrium-associates.com/offshore-company/register-company/com…- columbia-company/ (accessed March 25, 2021); https://www.offshore-pro.com/registering-lp-in-canada-with-a-corporate-…- top-canadian-bank.html (accessed March 25, 2021)

53 https://www.nexus.ua/sostavnyie-shemyi (accessed March 25, 2021)

54 http://www.acius.org/col_cl0bd9e.html (accessed March 25, 2021); http://www.hkrr.com/ca-co.shtml (accessed March 25, 2021) (see: “reasonably

avoid currency controls,” 合理避开外汇管制); http://www.tannet-group.com/Group/370/8433/20160913103335/ (accessed March 25, 2021)

55 http://www.ibccompanyformations.com/en/offshore/territorial-tax-regimes… (accessed March 25, 2021); https://www. confiduss.com/en/services/solutions/trading/canada-lp/ (accessed March 25, 2021)

56 http://www.offshore-sfi.com/offshore-in-canada (accessed March 25, 2021)

57 https://www.sfm.com/canada-company-formation (accessed March 25, 2021)

58 https://www.offshore-pro.com/registering-lp-in-canada-with-a-corporate-… (accessed March 25, 2021)

59 https://www.icd-fiduciaries.com/en/offshore-company/canada/ (accessed March 25, 2021)

60 https://www.uniwide.biz/offshore-jurisdictions/canada/ (accessed March 25, 2021)

61 https://www.offshore-pro.com/registering-lp-in-canada-with-a-corporate-… (accessed March 25, 2021)

62 Transparency International’s UK chapter and Global Witness have done some creative analysis of Companies House that shows some of the many ways the data can be analyzed to identify non-compliance, suspicious activity and financial crime. Global Witness, “The Companies We Keep”, 2018, TI UK, How we uncovered the UK businesses entangled in major corruption and money laundering cases, 2019

63 Jane Bradley and Oliver Bullough, “The ghost companies connected to suspected money laundering, corruption, and Paul Manafort”, Buzzfeed News, August 22, 2018

64 Mark MacKinnon, “’Snow-washing’: What leaked banking records show about Canada’s role in money laundering”, The Globe & Mail, March 4, 2019

65 “The FinCEN files: The billion dollar a month money trail”, Irish Times, September 20, 2020; “UK companies accused of money laundering in Magnitsky probe”, The Telegraph, April 29, 2013; “The Global Laundromat: how did it work and who benefited?”, The Guardian, March 20, 2017; “The Azerbaijani laundromat: a new money laundering machine in a familiar guise”, Anti-Money Laundering Centre (AMLC), April 24, 2019; “Report on the Non-Resident Portfolio at Danske Bank’s Estonia Branch”,Bruun & Hjejle, September 19, 2018 (pp.33, 73-76).

66 Filings for the UK entities claim that there was no beneficial owner. This is often achieved by splitting control between four or five entities so that none held a stake above the 25% disclosure threshold. However, Alberta records show that some of those LPs had the same general partners as the UK entities beneath them, meaning that their offshore parents surpassed the 25% disclosure threshold.

67 TI Canada delivered letters to all six LPs and followed up with phone calls to provide an opportunity to respond to claims made about them. No LPs responded.

68 These are all registered to the same address, a ‘company factory’ in Glasgow that serves as the address for several hundred entities, many

of which are part of the laundromat networks. https://suite.endole.co.uk/explorer/postcode/g41-3ja https://opencorporates.com/companies/gb/ SL030433 (accessed March 25, 2021); https://mobile.twitter.com/bencowdock/status/1440301491953143809 (accessed December 30, 2021); https://www.opendemocracy.net/en/odr/the-mysterious-scottish-shell-comp… (accessed December 30, 2021).

69 Bondwest AG used a nominee, Ali Moulaye, to sign accounts in the UK. Moulaye is a dentist based in Belgium who claimed to have nothing

to do with the hundreds of companies he signed for. Interviewed in the course of a BuzzFeed News investigation, he said his name and signature were used without his consent, and explained that he used to live in Latvia where “some people do some money laundering” (the service providers that set up the network of companies linked to Moulaye were based in Latvia). Jane Bradley and Oliver Bullough, “The ghost companies connected to suspected money laundering, corruption, and Paul Manafort”, Buzzfeed News, August 22, 2018; Inside scandal-rocked Danske Estonia and the shell-company ‘factories’ that served it - ICIJ; “The FinCEN files: The billion dollar a month money trail”, Irish Times, September 20, 2020

70 Wallingford Projects Ltd, Sellberg Networks LP, Hookson Projects LP and Walkstreet Organization Ltd. https://opencorporates.com/companies/ gb/08957498/statements/control_statement_subject (accessed March 25, 2021)

71 Graham Barrow, “Canadian entities involved in global laundromat style company formations”, submitted as evidence to the Commission of Inquiry into Money Laundering in British Columbia, December 2020

72 https://opencorporates.com/companies/gb/SL026031/statements/control_sta… (accessed March 25, 2021); https://www.linkedin. com/pulse/never-ending-beginning-like-ever-spinning-reel-graham-barrow/?trk=related_artice_Never%20ending%20or%20beginning%20 like%20an%20ever-spinning%20reel%E2%80%A6_article-card_title (accessed December 30, 2021).

73 “Latvian prosecutors open probe into bank links to Magnitsky case”, BNE Intellinews, October 4, 2013; “Behind the Proxies”, OCCRP, March 14, 2012; “Erik Vanagels – the extent of a money laundering supermarket”, Economic Crime Intelligence blog, February 23, 2012

74 The individuals, Danny Banger and Youngsan Kim, have 567 and 486 appointments, respectively. The companies, Fynel Ltd and Starwell International Ltd, are deeply embedded in the laundromat network and were used in an alleged US$230 million tax fraud orchestrated

by senior officials in Russia’s Interior Ministry in 2007. “At least 63 million dollars laundered through Latvian banks in the Magnitsky case”, Re:Baltica, September 28, 2012; “Latvian prosecutors open probe into bank links to Magnitsky case”, BNE Intellinews, October 4, 2012; http:// www.billbrowder.com/sergei-magnitsky; “A Farm of Directors”, Re:Baltica; October 4, 2012. (accessed March 25, 2021); Letter from Hermitage Capital Management to Latvian general prosecutor requesting a criminal investigation into money laundering network, 30 July 2012 (accessed December 30, 2021).

75 https://www.tba-associates.com/company-fomation-canada-for-non-resident…

76 The UK entities are: Oscar Professional Ltd, Custom Dundee Ltd, Aberdun Ltd, Acorn Fishing Ltd, Aberdow Ltd, Southeast Unicredit Partners Ltd, Prosight Trade Network Ltd, Financial Services Corporation Ltd, United Resources Systems & Technologies Ltd and First Union Capital Ltd. These shelf companies were controlled by 3ABC LLP but appear to have been sold separately from the parent entity.

77 https://www.tba-associates.com/shelf-and-aged-companies/shelf-companies… (3ABC no longer appears on the TBA website. The screenshot was taken January 22, 2020.)

78 https://www.tba-associates.com/canada-llp-british-columbia-canada-bc-li…. Many of these companies, including 3ABC LLP, were no longer listed for sale at the time of publication.

79 A search of the OpenCorporates database identified 451 appointments for Joaquim Magro de Almeida. This is not a comprehensive list, as it does not include appointments in jurisdictions that do not have open company registers or where that information is not collected.

80 “How British firms built a pyramid scheme in China that lost millions”, Reuters, August 12, 2016; Gareth Vaughan, “The misuse of NZ companies, Part III. Backdoor access via the UK - a classic cross jurisdictional regulatory arbitrage play”, Interest.ca.nz, December 17, 2017; “Companies with NZ ‘licences’ offering ‘investment expertise to global clients’ linked to alleged major international fraud”, Interest.co.nz, July 30, 2015; Progress report by court-appointed liquidator for Euro Forex Investment Ltd, October 15, 2018.

81 “Kiwi ‘shell’ spurs huge fraud probe”, The Star Times, May 18, 2014.; “ASIC and the $3m ‘prophet’”, Sydney Morning Herald, July 30, 2012; https:// prophetmaxreceivership.com/; US CFTC v IB Capital FX LLC et al consent order, October 14, 2016.

82 Almeida served as a director of the company for several years while another TBA principal, Luis Correia, served as the company’s auditor. “IT dept raids UPL’s offices in Mumbai, Gujarat”, The Economic Times, January 22, 2020; United Phosphorus Ltd annual accounts for 2015.

83 “Operación Cabo Verde: la vuelta al mundo para ocultar los sobornos de España a Arabia Saudí”, El Mundo, January 10, 2020; “Anticorrupcion desvela que Espana ha estado 25 anos pagando sobornos en Arabia Saudi”, El Mundo, January 9, 2020..

84 https://website.informer.com/JOAQUIM+MAGRO+DE+ALMEIDA+PANTEL+DELUXE+S.L… (accessed August 12, 2021)

85 TBA and Atrium have separate legal entities: TBA & Associates - Tax Business Advisors Ltd and Atrium & Associates (TBA) Ltd, respectively. However, they have common management and ownership, their websites have much of the same content, they share the same domain registrant and administrator, the source code on the TBA website makes multiple references to Atrium, and listings for Atrium in online business directories have been changed to TBA - all of which indicates that they are part of the same business.

86 “Groundhog Day for NZ FSPs: Bryan Cook of Asia Finance Corporation is a Crook, but Does NZ’s FMA Care?”, Naked Capitalism blog, June 29, 2015. The executive profiles appear in archives of the Atrium Incorporators website from 2015 . The webpage includes profiles of: Philip Simon, managing director; Bernard Johnson, partner; Christopher Ducanes, partner; and Beatrice Duvois, development manager. The profiles of ‘Philip Simon’ and ‘Bernard Johnson’ were lifted from another corporate service provider, OCRA Worldwide. ‘Christopher Ducanes’ is the name of a former general counsel for a Dallas software company, whose profile was plagiarised for the website, while the ‘Beatrice Duvois’ profile appears to have been taken from a template CV for a chartered accountant. Reverse image searches for their headshots offer further evidence that the Atrium Incorporators executives are false identities; the photographs correspond to other individuals whose identities were confirmed through some basic online research and who have no apparent links to Atrium Incorporators or TBA.

87 Extensive efforts were made to identify George Hamilton through online research but we found no record of an individual by that name being linked to TBA or its affiliated companies.

88 TBA registration number XWML00000128543.

89 Alexander Cooley, JC Sharman, “Blurring the line between licit and illicit: Transnational corruption networks in Central Asia and beyond”, Central

Asian Survey, 2015, “The secret scheme to skim millions off central Asia’s pipeline megaproject”, The Financial Times, December 3, 2020.

90 Examples of these red flags are set out in guidance by FINTRAC on suspicious financial transactions, available at: https://www.fintrac-canafe.

gc.ca/guidance-directives/transaction-operation/Guide3/str-eng.

91 https://transparencycanada.ca/news/civil-society-coalition-enthusiastic…-

federal-budget

92 “Implementing a publicly accessible pan-Canadian registry of beneficial ownership”, TI Canada, PWYP Canada, C4TF, 2020

93 Worldwide commitments and action — Open Ownership

ACKNOWLEDGEMENTS

Transparency International Canada, Publish What You Pay Canada, and Canadians for Tax Fairness are grateful to Open Society Foundations for supporting the research and writing of this report. The ideas, opinions, and comments within this publication are entirely the responsibility of its authors and do not necessarily represent or reflect the

Open Society Foundations. We are grateful to the experts and journalists who provided guidance for this report. Every effort has been made to verify the accuracy of the information contained in this report. All information was believed to be correct as of January 2022. Nevertheless, TI Canada cannot accept responsibility for the consequences of its use for other purposes or in other contexts than those intended. Policy recommendations reflect TI Canada’s opinion. They should not be taken to represent the views of any external stakeholders unless otherwise stated.

ALL RIGHTS RESERVED / REPRODUCTION OF THIS REPORT

Reproduction in whole or in parts is permitted, provided that full credit is given to Transparency International Canada and provided that any such reproduction, in whole or in parts, is not sold or incorporated in works that are sold. Written permission must be sought from Transparency International Canada if any such reproduction would adapt or modify the original content.