Résumé

A Narrative Report from Canadians for Tax Fairness as part of the Tax Justice Network’s Financial Secrecy Index 2020.

Rapport

Despite some positive developments since the last report, Canada continues to play a role in the offshore system. The country still offers a very low effective tax rate for businesses and acts as a regulatory haven for the world’s extractive industries. Canada has a long history in the development of tax havens, but today it is becoming better known as a destination for money laundering (or ‘snow washing’), due to Canada’s weak rules over corporate transparency and beneficial ownership. Transparency International ranked Canada at the bottom of the pack of all G20 countries in meeting G20 commitments on beneficial ownership and transparency. [1]

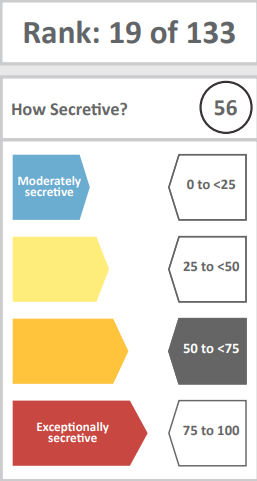

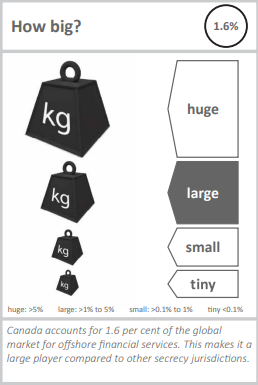

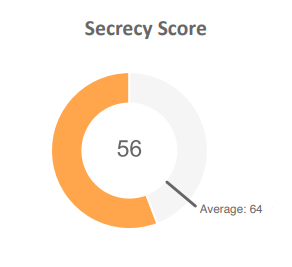

Canada is ranked 19th on the 2020 Financial Secrecy Index, based on a secrecy score of 56 combined with a large-scale weighting due to the fact that Canada accounts for 1.6 per cent of the global market in offshore financial services.

Notes: The ranking is based on a combination of its secrecy score and scale weighting. Full data is available here: http://www. financialsecrecyindex.com/database. To find out more about the Financial Secrecy Index, please visit http://www.financialsecrecyindex.com. The FSI project has received funding from the European Union’s Horizon 2020 research and innovation programme under grant agreement No 727145. © Tax Justice Network 2020 If you have any feedback or comments on this report, contact us at info@taxjustice.net.

HISTORY: CANADA IN THE CARIBBEAN

The history of trade relations between Canada and the Caribbean islands begins as far back as the development of New France [2] in the 17th Century. By the 19th century these relations were so close that Canada wanted to put British dependencies in the Caribbean under its own colonial administration. London rejected this but in 1837 the Colonial Bank of the Caribbean, the British banking authority for its dependencies in the region, signed an agreement with the Halifax Banking Company allowing it to develop there even before it had been registered in Toronto. At various stages Ottawa has wielded more influence than London on financial decisions affecting the Caribbean islands.

This helps explain the spectacular growth of Canadian banking in the Caribbean in the twentieth century. Particularly in the Bahamas and the Cayman Islands, Canadians were instrumental in the development of business districts and legislative initiatives that provided tax benefits for banks, businesses and private wealth holders. As the IMF noted in 2013: “Foreign banks, primarily Canadian, play a leading role throughout the Caribbean, accounting for about 60 per cent of banking system assets.” [3]

Since 1980, the most notorious Canadian-linked tax haven has been Barbados. A non-double taxation treaty between the two countries allows Canadian corporations to register assets in Barbados and then transfer them back to Canada, with income that has been realized in Barbados being almost completely untaxed.

Today, Canada is using this privileged tax relation as a model for tax information sharing treaties (known as “Tax Information Exchange Agreements”, or TIEA) [4] signed with other tax havens. TIEAs signed by the Canadian government are unusual. They are being enacted as non-double taxation treaties. According to Consolidated Regulation 5907(11) of the Canadian Income Tax Act, as soon as Canada has signed such an agreement with a tax haven, companies declaring international income in jurisdictions where taxes are close to zero are allowed to bring the money back home to Canada as dividends without paying Canadian tax. [5] So far, highly accommodating agreements have been established with the following, among others: Anguilla, the Bahamas, Bahrain, Brunei, Bermuda, the British Virgin Islands, the Cayman Islands, the Cook Islands,Curaçao, Dominica, Liechtenstein, Saint Lucia, Saint Vincent and the Grenadines, San Marino, St Kitts and Nevis, and the Turks and Caicos Islands.

In 2011 Canada also approved a free-trade agreement with Panama, [6] even though Panama is viewed by many crime experts as a leading centre for laundering the proceeds from drug trafficking.

The election of the Liberal Party government in 2015 and its re-election as a minority government in 2019 has made little change so far in Canada’s accommodating relationship with tax havens. Ottawa signed a new version of its very permissive TIEA with the Cook Islands, [7] as Conservatives had done before. The Liberal majority at the House of Commons also voted against a private member’s motion tabled by MP Gabriel Sainte-Marie, [8] which asked the government to amend “subsection 95(1) of Income Tax Act and section 5907 of the Income Tax Regulations to specify that no business that is entitled to a special tax benefit conferred by Barbados under the Canada-Barbados Income Tax Agreement Act, 1980, shall be exempt from taxation because of a tax treaty.” Voting against this proposal was a way for the House to endorse, for the first time, a very controversial treaty [9] that the government had signed in 1980 without consulting Parliament in any way.

According to the latest Statistics Canada, Canadian corporations reported $353 billion Canadian dollars [10] in so-called “foreign direct investments” in the top 12 tax havens at the end of 2018. Topping the list was $90 billion that Canadian corporations have in Luxembourg and $65 billion in Barbados, followed by $47 billion in Bermuda and $40 billion in the Cayman Islands. Despite the 2016 Panama Papers leak, the amount officially reported by Canadian corporations in Panama increased by 9%; in the British Virgin Islands, another top tax haven for Canadians, it increased by 50%. These figures are at the lower end, as they include only what the corporations have reported.

With conservative assumptions of just a 5% return and an effective 20% tax rate, this means that Canadian governments are losing a minimum of $3.5 billion annually from corporate profit and tax shifting with these tax havens. Some international estimates are that Canadian governments lose in the range of $6 to $8 billion from international tax avoidance. A more recent estimate in June 2019 from Canada’s Parliamentary Budget Officer was that Canada could be losing from $1 billion to $25 billion in tax revenues due to multinational tax dodging through tax havens. [11] The range of estimates is wide because there is little transparency and information available on the financial status of multinational corporations on a country-by-country basis.

In recent years, the government also voted down proposed legislation to improve Canada’s ability to fight offshore tax avoidance. In May 2019, the Liberal-majority House of Commons rejected an independent Senator’s private member’s bill [12] that would have required the Canada Revenue Agency to report on Canada’s tax gap.

Just two months earlier, the country’s Parliamentary Budget Officer (PBO) had acknowledged that there isn’t enough data available to properly assess the cost of offshore tax havens or how best to fix the problem. [13] The senator’s bill would have provided a better picture of how much is lost to tax havens and strengthened citizens’ rights to know that their tax system is fair and transparent. Several years ago, another private member’s bill had proposed to add an economic substance requirement to Canada’s Income Tax Act, requiring corporations using tax havens to prove a transaction had economic substance, but this bill too was defeated by Canada’s then-Conservative government. [14]

The Canadian government has proceeded with a number of reforms associated with the OECD’s Base Erosion and Profit Shifting (BEPS) initiative. These include multilateral agreements with 52 other jurisdictions (as of September 2019) [15] for country-bycountry reporting by large multinational enterprise groups (BEPS Action 13), for automatic exchange of financial account information through the Common Reporting Standard, [16] and the ratification of the OECD’s Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (MLI), which will enter into force for Canada on 1 December 2019 [17] (BEPS Action 15).

In the 2019 election, both the Liberal Party and the NDP, which are expected to cooperate as a minority government, included limiting excessive interest deductions for domestic and multinational groups (BEPS Action 4) as part of their election platforms. However, the Liberal government has not agreed to make the country-by-country reports of financial information by multinational groups publicly available. Neither do Canadian governments publish, or require corporations to publish, details of their individual corporate financial and tax accounts on a jurisdiction-by-jurisdiction basis (with the exception of Extractive Sector Transparency Act reports, as discussed below).

CANADA’S ROLE AS A TAX HAVEN

Canada’s fairly low secrecy score shows that it is less opaque than many jurisdictions. One area where it trails behind its peers is the lack of transparency of beneficial ownership of corporations and trusts and the ease with which one can register anonymous shell corporations.

World Bank research summarized [18] by Canada’s National Magazine notes: “Canada and the U.S. are the two most lax jurisdictions in the world when it comes to the rules for preventing the incorporation of anonymous shell companies. What’s more, corporate service providers operating in those two countries are less compliant than those operating in Ghana, Lithuania, or Barbados, and follow laxer rules than those in Malaysia or the Cayman Islands.”

The Panama Papers leak also revealed that the Panamanian law firm Mossack Fonseca was advising its clients in 2010 that: “Canada is a good place to create tax planning structures to minimize taxes like interest, dividends, capital gains, retirement income and rental income.” [19]

Canada has developed a reputation as an attractive place to launder money due to its rule of law, strong economy, and the ease with which one can create a shell company. The global term “snow washing” was coined to describe how illicit funds can be washed clean like the pure white snow in Canadian real estate. [20]

The country’s weaker anti-money-laundering laws provide criminals with the anonymity to not get caught and likely not be prosecuted if they are caught. [21]

In May 2019, a Canadian expert panel report revealed that as much as $46 billion was laundered through the country in 2018. [22] The province of British Columbia on the country’s west coast called a public inquiry into the problem, which has also taken root in other regions across the country.

More than $20 billion entered the housing market in Canada’s largest city, the Greater Toronto Area, according to a March 2019 report by Transparency International Canada, Canadians for Tax Fairness and Publish What You Pay Canada. [23]

Experts have identified a public registry of beneficial owners as one of the single most effective ways to deter money laundering. In April 2019, the province of B.C. committed to a public registry of beneficial owners for real estate. The federal government confirmed in June 2019 that it would, along with the provinces, review options for combating money laundering. The government said it would begin consultations on a public registry of beneficial owners of companies but has not committed to implementing one. [24]

Despite changes in the Canada Business Corporations Act requiring corporations to track beneficial ownership themselves—but not yet to report it to anyone else— experts have cautioned that these half-measures still leave plenty of gaps. [25]

Tax dodgers have also benefited from Canada’s complex tax system.

A prime example is the city of Halifax, in eastern Canada, which for the past few years has been the headquarters of a development agency known as Nova Scotia Business Inc., [26] created by the Nova Scotia government and managed exclusively by private partners. The agency is in practice a place where tax advantages [27] can be obtained by hiring accountants working for firms involved in insurance and hedge funds in connection with the tax havens of Bermuda and the City of London.

KPMG’s Competitive Alternatives 2016 Special Report: Focus on Tax concluded that total business tax costs in Canada were the lowest in the G7, and 48 per cent lower than those in the United States. [28]

A study of 99 of the largest Canadian corporations from 2009 to 2011 revealed that on average, the effective tax rates paid by the corporations amounted to 19.5 per cent – though many enjoyed far lower rates. [29]

In 2009, the Canadian Department of Transport produced a document whose title says it all: Canada Tax and Duty Advantages: Enjoy the Benefits of Foreign Trade Zones... Anywhere in Canada! The programme, known as “Canada’s Gateways,” freely adopts offshore language and eliminates GST and customs tariffs on exports. The International Financial Centre of Montreal, [30] established in 1986, [31] says that [32] 75% of the net profits of foreign companies that register with it will not be taxed, and that other tax advantages will be provided for employees. Canadian companies can claim identical benefits through their offshore subsidiaries.

Canada has also been a tax and regulatory haven for the world’s extractive industries. According to government sources [33] in 2013, more than half of the world’s publicly listed mining companies are headquartered in Canada. The Toronto Stock Exchange is more favourable than others to speculation in this area, and tax benefits are specifically designed to encourage investment in the mining industry.

Since 2011, income trusts in Canada have been tax exempt as long as they manage no substantial activity within the country. This rule, originally established in 2006, has benefited owners of mining assets throughout the world: they can register trusts in Canada that own mining assets elsewhere. Keith Schaefer, publisher of the Oil and Gas Investment Bulletin, [34] wrote in 2011: “Last year, Eagle Energy Trust (EGL.UN) went public on the TSX, which was the first Canadian-listed oil and gas trust to launch since Flaherty’s Halloween surprise in 2006. The company holds only foreign oil-producing assets […], a loophole that excludes it from the new Canadian tax regime.”

Canada has not agreed to implement and join the Extractive Industry Transparency Initiative as a member, but it has agreed to similar reporting requirements, which were put into place with passage and implementation of the Extractive Industry Transparency Measures Act in 2015. [35]

At the federal level, corporate taxes have been aggressively cut by successive administrations. Between 1981 and 2012, the federal corporate tax rate dropped from 38 per cent to 15 per cent. Moreover, tax breaks, constantly deferred tax payments and the abolition of other business taxes have turned Canada into a tax haven. As a result, major corporations such as Burger King or Valeant Pharmaceuticals have decided to move their headquarters to Canada explicitly for tax purposes. [36] [37]

Politically, Canada tends to protect and lobby on behalf of the mining industry despite the industry’s sorry ethical record at the international level, to the point where Canada incurred a rebuke from the OECD [38] in a 2011 report on international corruption. In this report, an OECD working group explicitly asks why Canada has prosecuted only one company over a ten-year period, even though it is home to a majority of the world’s mining companies – companies which, according to the group, are known to be particularly likely to resort to influence-peddling – and despite Canada’s commitment to investigating and prosecuting any corporation registered on its territory that is suspected of corruption abroad.

Many oil and gas companies with operations in Canada have also been able to lower their tax bills. A 2017 report by Canadians for Tax Fairness found that 11 of the country’s largest companies in the sector had subsidiaries and related companies in tax havens. [39]

On the diplomatic front, Canada shares its seat on the Board of the World Bank [40] and the IMF with Ireland and a group of Caribbean tax havens consisting of Antigua & Barbuda, the Bahamas, Barbados, Belize, Dominica, Grenada, Guyana, Jamaica, St. Kitts and Nevis, Saint Lucia and Saint Vincent and the Grenadines.

The Canadian government has recently published “tax gaps” reports, with estimates of the revenues not collected due to tax evasion and other factors and, while not agreeing to enshrine it in legislation, did agree to produce these reports on a regular basis. [41] Federal and provincial governments have mostly targeted tax evasion within the small-scale domestic economy, while doing less to combat large corporations’ or high net worth individuals’ tax evasion. A 2018 report from Canada’s Auditor General found that the country’s revenue agency was tougher on domestic individual and smaller businesses than on offshore and corporate cases. [42]

The federal Liberal government has increased the capacity of the Canada Revenue Agency to go after wealthy individuals and corporations using tax havens to evade taxes and announced other measures to curb tax evasion, and says this has resulted in significantly increased revenue returns. However, there have been no charges laid, convictions or funds recovered related to Canadians exposed by the Panama Papers leak. [43] The Canadian government has also had little success in prosecuting corporations for international tax evasion cases.

Canada also issues relatively low penalties for tax avoidance and evasion. In the US, accounting giant KPMG paid US$456 million in penalties for its part in creating fraudulent tax shelters, [44] but there has been no prosecution of, or penalty for, KPMG for their role in this tax dodging scheme in Canada. In other cases, it is not known what if any punishment a corporation or individual has received due to settlements or write-offs that are not published.

In May 2019, an investigative journalist with Canada's public broadcaster, the CBC, discovered that the government had secretly settled with wealthy individuals in the KPMG Isle of Man scandal. [45] Canadians only learned of this information in the news.

Even where the government has taken action to prevent tax avoidance, investigative authorities then need to navigate the courts. A government consultation [46] on treaty shopping highlighted the frustration of the Canadian government in the lenient attitude the courts had taken to companies accused of abusing Canada’s tax treaty network. Canadian courts have already endorsed a type of transfer pricing process [47] that has been shown to be an abusive tax avoidance strategy throughout the world. [48] This may explain why the Canada Revenue Agency chose not to sue KPMG clients who were caught hiding funds on the Isle of Man, [49] as the CBC revealed in 2017: going to court would have been extremely costly, and the rules followed by the courts are unpredictable. Suspicions were raised when the same media discovered Canadian judges attending KPMG-sponsored cocktails [50] in Madrid.

FURTHER READING:

- Alain Deneault, with the Réseau Justice fiscale (Canada), Canada: A New Tax Haven. How the Country That Shaped Caribbean Tax Havens Is Becoming One Itself, [51] Vancouver: Talonbooks, 2015.

- Alain Deneault and William Sacher, Imperial Canada Inc.: Legal Haven of Choice for the World’s Mining Industries, [52] Vancouver: Talonbooks, 2011.

- Alain Deneault, Offshore: Tax Havens and the Rule of Global Crime, [53] New York: The New Press, 2011.

- Mario Possamai, Money on the Run: Canada and How the World’s Dirty Profits Are Laundered, Toronto: Penguin Books of Canada, 1992.

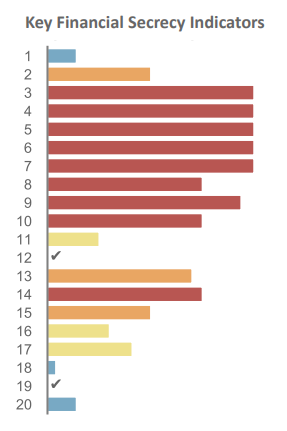

SECRECY SCORE

Notes and Sources:

- The FSI ranking is based on a combination of a country’s secrecy score and global scale weighting (click here to see our full methodology).

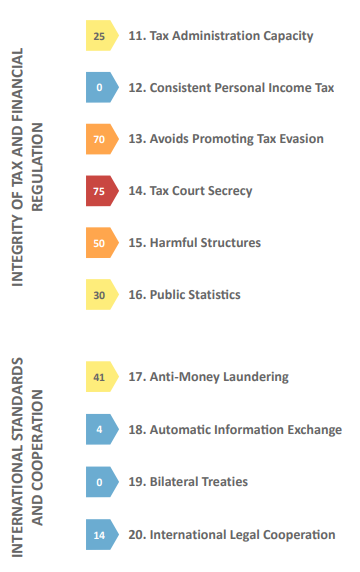

- The secrecy score is calculated as an arithmetic average of the 20 Key Financial Secrecy Indicators (KFSI), listed on the right. Each indicator is explained in more detail in the links accessible by clicking on the name of the KFSI.

- A grey tick in the chart above indicates full compliance with the relevant indicator, meaning least secrecy; red indicates non-compliance (most secrecy); colours in between partial compliance. This report draws on data sources that include regulatory reports, legislation, regulation and news available as of 30 September 2019 (or later in some cases).

- Full data is available here: http://www.financialsecrecyindex.com/database.

- To find out more about the Financial Secrecy Index, please visit http://www.financialsecrecyindex.com.

ENDNOTES

[1] Transparency International, 2018, G20 Leaders or Laggards? https://www.transparency. org/whatwedo/publication/g20_leaders_or_lag - gards; 04.02.2020.

[3]https://www.elibrary.imf.org/view/IMF001/20722-9781484307830/20722-9781484307830/20722-9781484307830_A001. xml?redirect=true; 30.07.2019.

[4]https://www.taxjustice.net/cms/upload/pdf/Tax_Information_Exchange_Arrangements.pdf; 30.07.2019.

[5] https://www.financialsecrecyindex.com; 30.07.2019.

[6]https://www.fin.gc.ca/n17/17-066-eng.asp?Mode=1&Parl=40&Ses=3&DocId=4855622& - File=0&Language=E; 30.07.2019.

[7] https://www.financialsecrecyindex.com/; 30.07.2019.

[8] https://openparliament.ca/de - bates/2016/4/14/gabriel-ste-marie-2/only/; 30.07.2019.

[9] www.imf.org/external/pubs/ft/wp/2013/ wp13175.pdf; 30.07.2019.

[10]https://www.taxfairness.ca/en/press_release/2019-04/canadian-corporate-cash-top12-tax-havens-increases-10-all-time-high-2018; 04.02.2020.

[11]https://www.pbo-dpb.gc.ca/web/default/files/Documents/Reports/2019/Preliminary-Findings-International-Taxation/Report%20final.pdf; 04.02.2020.

[12] https://www.parl.ca/legisinfo/BillDetails. aspx?billId=9264702&Language=E; 04.02.2020.

[13]https://www.ctvnews.ca/politics/pbosays-it-cannot-fully-measure-cost-of-tax-avoidancedue-to-incomplete-data-1.4365303; 04.02.2020.

[14]https://www.parl.ca/LegisInfo/BillDetails.aspx?Bill=C621&Language=E&Mode=1&Parl=41&Ses=2; 04.02.2020.

[15]https://www.oecd.org/tax/beps/country-by-country-exchange-relationships.htm; 04.02.2020.

[16]https://www.oecd.org/tax/transparency/AEOI-Implementation-Report-2018.pdf; 04.02.2020.

[17] https://www.fin.gc.ca/treaties-conventions/notices/mli-im-eng.asp; 04.02.2020.

[18]http://www.nationalmagazine.ca/Articles/June_2013/Shell_companies_Blinders_on.aspx; 30.07.2019.

[19]http://projects.thestar.com/panama-papers/canada-is-the-worlds-newest-tax-haven/; 30.07.2019.

[20]https://www.theguardian.com/world/2018/feb/14/canada-corruption-snow-washing-investigation-private-companies; 04.02.2020.

[21]https://business.financialpost.com/opinion/why-canadas-money-laundering-problem-isfar-bigger-than-we-think; 04.02.2020.

[23]http://www.transparencycanada.ca/wp-content/uploads/2019/03/BOT-GTA-ReportWEB-copy.pdf; 04.02.2020.

[25]https://www.cdhowe.org/intelligence-memos/denis-meunier-%E2%80%93-canada-business-corporation-act-changes-beneficial-ownership-half; 04.02.2020.

[26] https://www.financialsecrecyindex.com/; 30.07.2019.

[27]http://www.novascotiabusiness.com/en/home/invest/incentivesandtaxes/default.aspx; 30.07.2019.

[28]https://www.competitivealternatives.com/reports/compalt2016_report_tax_en.pdf; 30.07.2019.

[29] The research was carried out by the Laboratoire de recherche socioéconomique at the Université du Québec à Montréal (UQÀM). Their data included the following:

|

Company |

Before-tax profit (in millions of US $) |

Effective tax rate |

|

Cott Corporation |

193.20 |

-14.50 % |

|

Emera Inc. |

639.20 |

-7.00 % |

|

Canadian Pacific Railway |

2,199.00 |

-4.70 % |

|

Molson Coors Brewing Company |

2,420.70 |

-1.90 % |

|

Canadian Oil Sands Limited |

2,762.00 |

0.00 % |

|

TransCanada Corporation |

5,914.00 |

1.70 % |

|

Québecor Inc. |

1,822.20 |

3.80 % |

|

Rogers Communications Inc. |

6,192.00 |

5.10 % |

|

Enbridge Inc. |

4,764.00 |

5.30 % |

|

SNC-Lavalin Group Inc. |

1,567.70 |

6.20 % |

[30] https://www.novascotiabusiness.com/; 30.07.2019.

[31] http://www.finance-montreal.com/fr/mesure-cfi; 30.07.2019.

[32] http://www.taxfairness.ca/en/news/barbados-remains-canadas-top-tax-haven; 30.07.2019.

[33]http://www.international.gc.ca/trade-agreements-accords-commerciaux/topics-domaines/other-autre/csr-strat-rse.aspx?lang=eng; 07.02.2018.

[34] http://www.international.gc.ca/message. aspx?&mst=404; 30.07.2019.

[35]https://www.nrcan.gc.ca/mining-materials/resources/extractive-sector-transparency-measures-act-estma/18180; 04.02.2020.

[36]https://fortune.com/2014/08/28/is-burger-kings-move-to-canada-a-raw-deal-for-u-s-taxpayers/; 04.02.2020.

[37]https://www.forbes.com/sites/matthewherper/2014/07/19/can-anything-stop-drug-companies-from-fleeing-the-u-s-tax-system/#4c6dfb - c04a37; 04.02.2020.

[38] http://www.worldbank.org/en/country/ canada; 30.07.2019.

[39]https://thenarwhal.ca/enbridge-transcanada-among-11-canadian-oil-and-gas-firms-usingtax-havens/; 04.02.2020.

[40] www.taxjustice.net/topics/corporate-tax/ transfer-pricing/; 30.07.2019.

[41]https://www.canada.ca/en/revenue-agency/programs/about-canada-revenue-agency-cra/ corporate-reports-information/tax-gap-overview. html; 04.02.2020.

[42]https://www.ctvnews.ca/politics/cradoes-not-consistently-apply-auditing-rules-to-alltaxpayers-ag-1.4184565; 04.02.2020.

[43]https://www.taxfairness.ca/en/newsletter/2019-04/three-years-post-panama-paperswhat’s-changed; 04.02.2020.

[44] KPMG paid US$456 million; 04.02.2020.

[45] https://www.cbc.ca/news/business/ cra-kmpg-settlement-taxes-1.5154610; 04.02.2020.

[46] https://www.fin.gc.ca/activty/consult/tscf-eng.asp; 30.07.2019.

[47]https://www.theglobeandmail.com/globe-investor/supreme-court-backs-glaxo-in-transfer-pricing-dispute/article4620345/; 30.07.2019.

[48] http://www.taxjustice.net/topics/corporate-tax/transfer-pricing/; 07.02.2020.

[49]http://www.cbc.ca/fifth/episodes/2016-2017/kpmg-and-tax-havens-for-therich-the-untouchables; 30.07.2019.

[50] https://oilandgas-investments.com/2011/ investing/energy-income-trusts/; 30.07.2019.

[51] http://publications.gc.ca/collections/collection_2010/tc/T22-178-2009-eng.pdf; 30.07.2019.

[52]https://www.researchgate.net/publication/307638552_Imperial_Canada_Inc_Legal_Hav - en_of_Choice_for_the_World%27s_Mining_Industries; 07.02.2020.