Summary

Canadians had at least $682B stashed in tax havens in 2024, a 165% increase since 2014. The use of tax havens has accelerated because Canada has continued to sign tax agreements that incentivize corporations to shift profits to tax havens. We estimate that the signing of five tax information exchange agreements with tax havens in the early 2010s led to $47.1B being shifted to tax havens over the next five years.

Due to a lack of financial transparency, the cost of tax havens to the public purse is difficult to estimate, but it is likely at least $15B annually. The members of the S&P/TSX 60, an index of many of Canada’s largest publicly-traded corporations, alone avoided $7B in taxes due to lower corporate tax rates in foreign jurisdictions in 2024. All these taxes were avoided by corporations that have subsidiaries in tax havens, of which there are at least 46.

While negotiations at the OECD and G20 over the last ten years have taken some meaningful steps, these bodies have ultimately failed to develop a global framework to prevent the use of tax havens by multinational corporations looking to avoid paying taxes in the countries where they make their profit.

In order to ensure Canada has the revenue to fund public services and infrastructure, Canada must immediately end tax agreements with known tax havens, require corporations to have a genuine business reason to set up subsidiaries in tax havens, and support the UN’s push for a global tax convention that puts a stop to tax avoidance by the ultra-wealthy.

Report

Introduction: Canada has a big tax haven problem

In 2024, large corporations and wealthy Canadians had at least $682B invested in 15 tax havens, more than the value of all machinery and equipment in Canada. This figure is the culmination of decades of large corporations and wealthy Canadians shifting their assets to tax havens to avoid paying taxes. Unfortunately, government policy over the years has legalized and normalized this tax avoidance rather than cracking down on it. In this report, we explain what this is costing us, how we got here, and what we can do about it.

What are tax havens?

Tax havens are jurisdictions that provide corporations and wealthy individuals with various tax benefits. Most commonly, this involves low or zero tax rates, especially on corporate income and capital gains. They also often provide other benefits, such as the ability to set up corporations secretly without the corporation being traceable to its true owner, lack of financial regulation, and lax criminal laws. In this report, we use the Tax Justice Network’s Corporate Tax Haven Index to identify tax havens. The top 14 countries from this list, plus Barbados, which was not assessed by Tax Justice Network but has long been considered one of Canada’s wealthy elite’s favourite tax havens, and Delaware, when data is available at a sub-national level, are considered tax havens for this report. The full list is: The Bahamas, Barbados, Bermuda, The British Virgin Islands, The Cayman Islands, Cyprus, Delaware, Guernsey, Hong Kong, Ireland, Isle of Man, Jersey, Luxembourg, Netherlands, Singapore, Switzerland.

How much does the use of tax havens cost Canadians? The best estimate of lost tax revenue is from the Tax Justice Network, which estimated that Canada loses over $15B per year in tax revenue because of tax havens, or enough to entirely fund a full pharmacare program and the Canadian Dental Care Program. This includes $12.3B lost due to multinational companies shifting their profits to tax havens and $2.8B lost from wealth being hidden in tax havens. A 2019 report from the Parliamentary Budget Office suggested the figure could be anywhere up to $25B a year ($30B in today’s dollars). Unfortunately, due to a lack of public country-by-country reporting of financial information in Canada, this figure is very difficult to pin down.

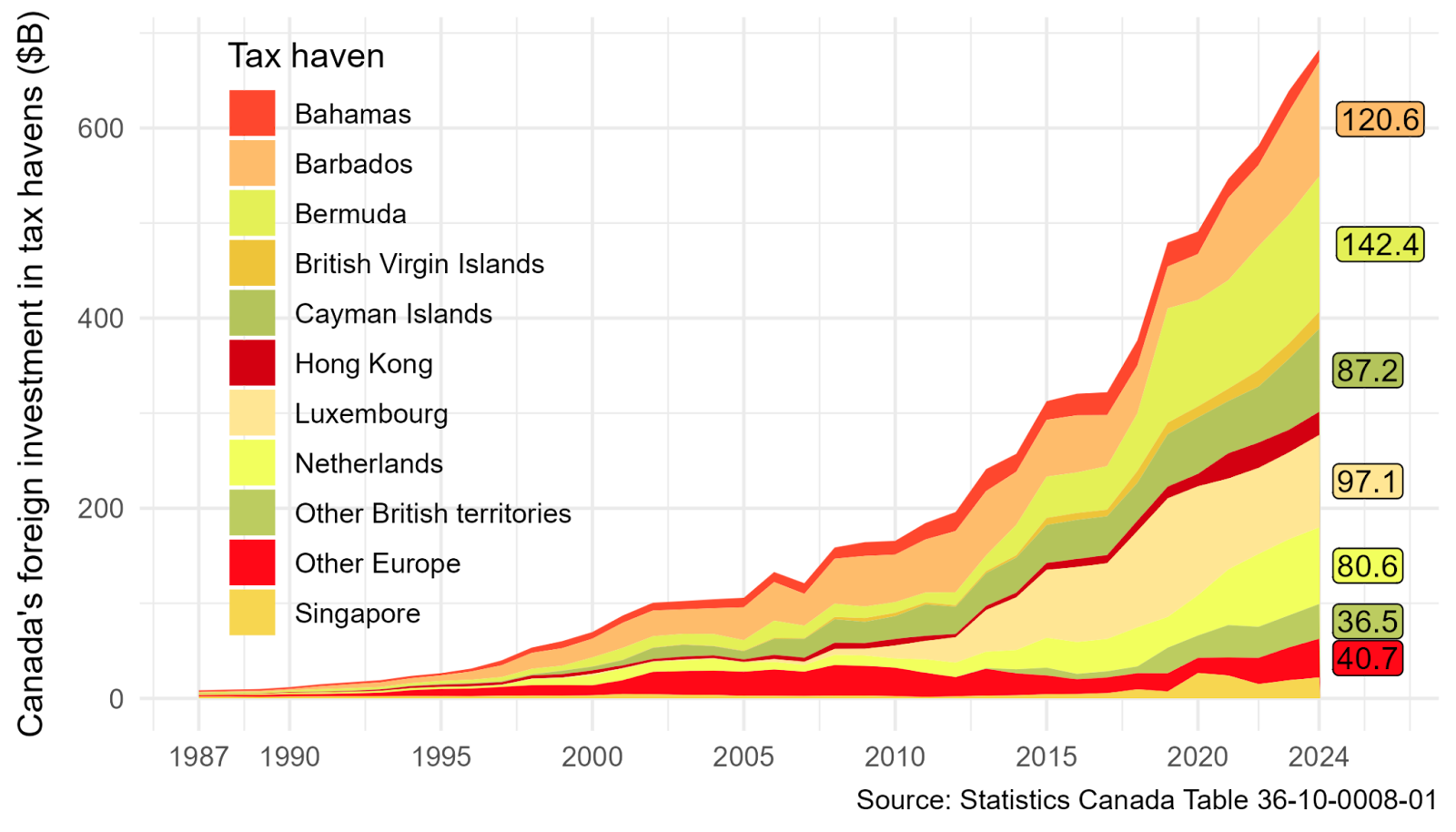

The shifting of assets offshore to avoid taxes, with the support of the Canadian government, is a long tradition in Canada that can be traced back to the 19th century (see “How did we get here?” section). Reliable data on Canadian assets in tax havens, however, only exists since 1987. Canadian foreign direct investment in 15 tax havens since 1987 is displayed in Figure 1. Over this period, Canadian assets in tax havens have grown consistently at rates of 10-30% per year each decade.

The 15 tax havens include countries and territories in the Caribbean, Europe, and Asia. In 2024, the most used tax havens by Canada’s large corporations and wealthy elite include Bermuda, with $142.4B in assets, Barbados with $120.6B in assets, Luxembourg with $97.1B, the Cayman Islands with $87.2B, and the Netherlands with $80.6B.There are many factors that determine in which country Canadian companies and wealthy Canadians will choose to stash their assets. These include the country’s local tax rates, local transparency regulations, and, importantly, whether the country has any tax agreements with Canada. This last factor has an outsized importance because of a unique quirk of the Canadian tax code.

Figure 1. Canadian FDI in top 15 tax havens, 1987-2024.

Note. Other British territories include Guernsey, Isle of Man, and Jersey. Other Europe includes Cyprus, Ireland, and Switzerland.

Profits of foreign subsidiaries of Canadian companies are exempt from Canadian taxation only if Canada has a tax treaty or, as of 2009, a tax information exchange agreement (TIEA) with the country in which the subsidiary resides. As of 2024, this benefit has been reduced, although by no means eliminated, by the Global Minimum Tax Act, Canada’s implementation of the OECD/G20 agreement on base erosion and profit shifting. Nonetheless, there is still a large incentive for corporations to shift assets to jurisdictions with which Canada has a treaty or TIEA. Today, Canada has tax treaties or TIEAs with all of these top 15 tax havens. However, this was not always the case.

In the early 2000s, only 7 of these tax havens had treaties in force with Canada. During this period, the most used tax havens by large corporations and wealthy Canadians included those with whom Canada had a tax treaty – namely, Barbados, Ireland, and the Netherlands.

In 2009, the law was altered so that companies in countries with which Canada had a tax information exchange agreement (TIEA) could also benefit from the exemption. Despite the knowledge that providing this exemption to tax havens gave companies a huge incentive to shift profits to those countries to avoid taxes, under pressure from the OECD, the Harper government signed new TIEAs with tax havens, including the Bahamas, Bermuda, Cayman Islands, Jersey, Isle of Man, Hong Kong, Guernsey, and the British Virgin Islands between 2010 and 2014. Today, Bermuda and the Cayman Islands are two of corporate Canada’s favourite tax havens.

Estimating the impact of new tax agreements

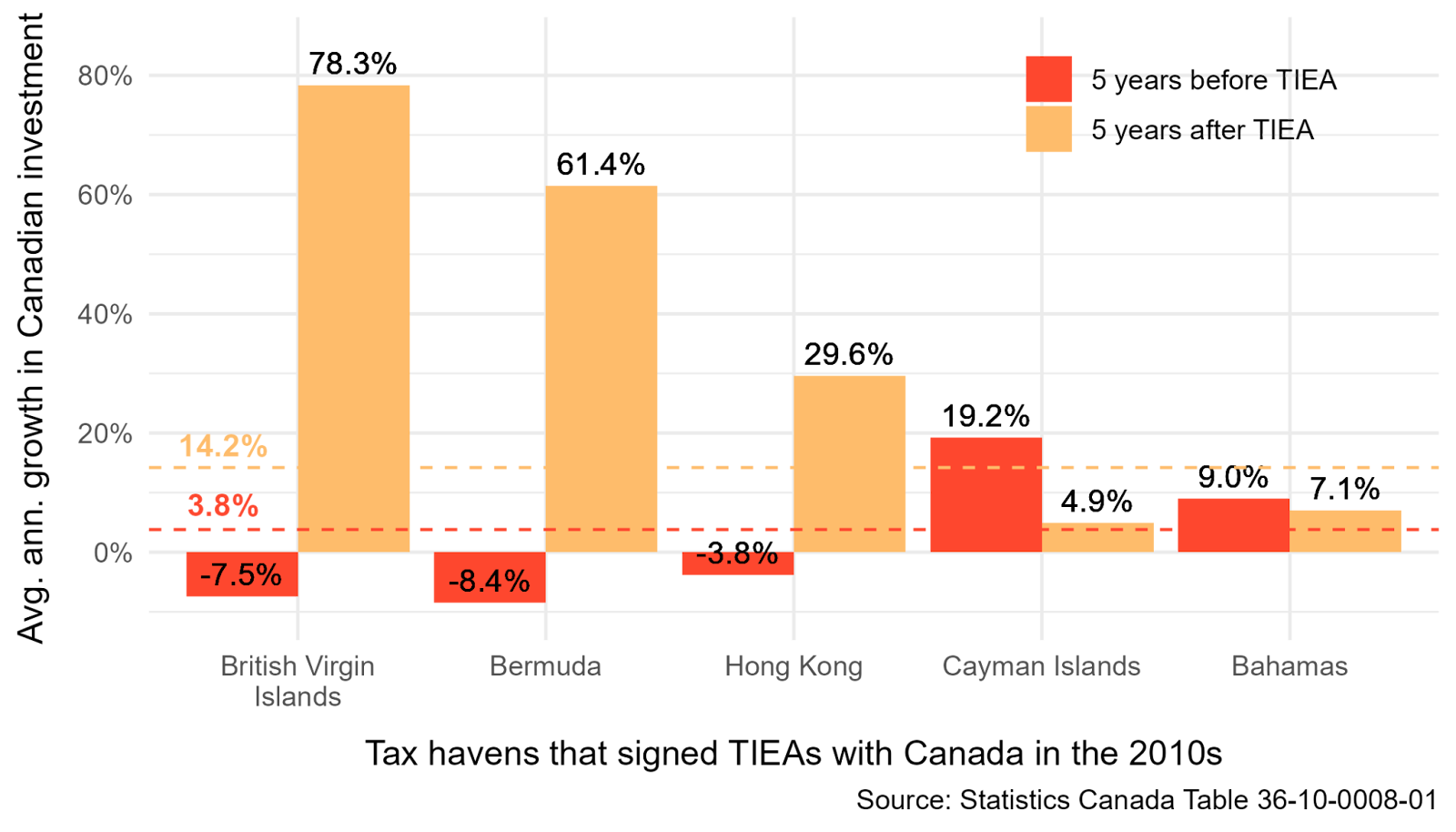

To understand the impact of the proliferation of tax agreements with tax havens, we examined Canadian foreign investment in five countries before and after signing tax information exchange agreements (TIEAs). Figure 2 displays the results. There were massive increases in Canadian investment in the British Virgin Islands, Bermuda, and Hong Kong following the signing of TIEAs. Canadian investment in the Cayman Islands and the Bahamas did not increase (there were already significant Canadian assets stashed in these two countries – although the foreign subsidiary exemption is one incentive for the use of tax havens, it is not the only one).

We estimate that the signing of these TIEAs increased the growth in Canada’s foreign investment in these five tax havens by over 10 percentage points per year. In the five years before signing these agreements, Canada’s foreign investment in these tax havens was increasing by 3.8% annually. After the agreement opened a new tax loophole, foreign investment in these tax havens increased by 14.2% annually. This suggests that the TIEAs led to an additional $47.1B being shifted to these five tax havens in the five years following the signing of these agreements.

Figure 2. Growth in investment in tax havens exploded after Canada signed tax information exchange agreements (TIEAs) with them.

The main purpose of Canada’s investment in tax havens is tax avoidance

Canadians’ assets in tax havens are not “investments” in the typical sense of the term. When we hear about Canada’s foreign investment, we typically think of a new infrastructure or natural resources project. These types of projects can generate real economic activity and benefit local populations and foreign investors. However, investment can also include purely financial transactions – these types of investment do not provide any real service or good but rather simply shift financial assets for the purpose of increasing profit (in the case of tax havens, this is typically through lowering taxes).

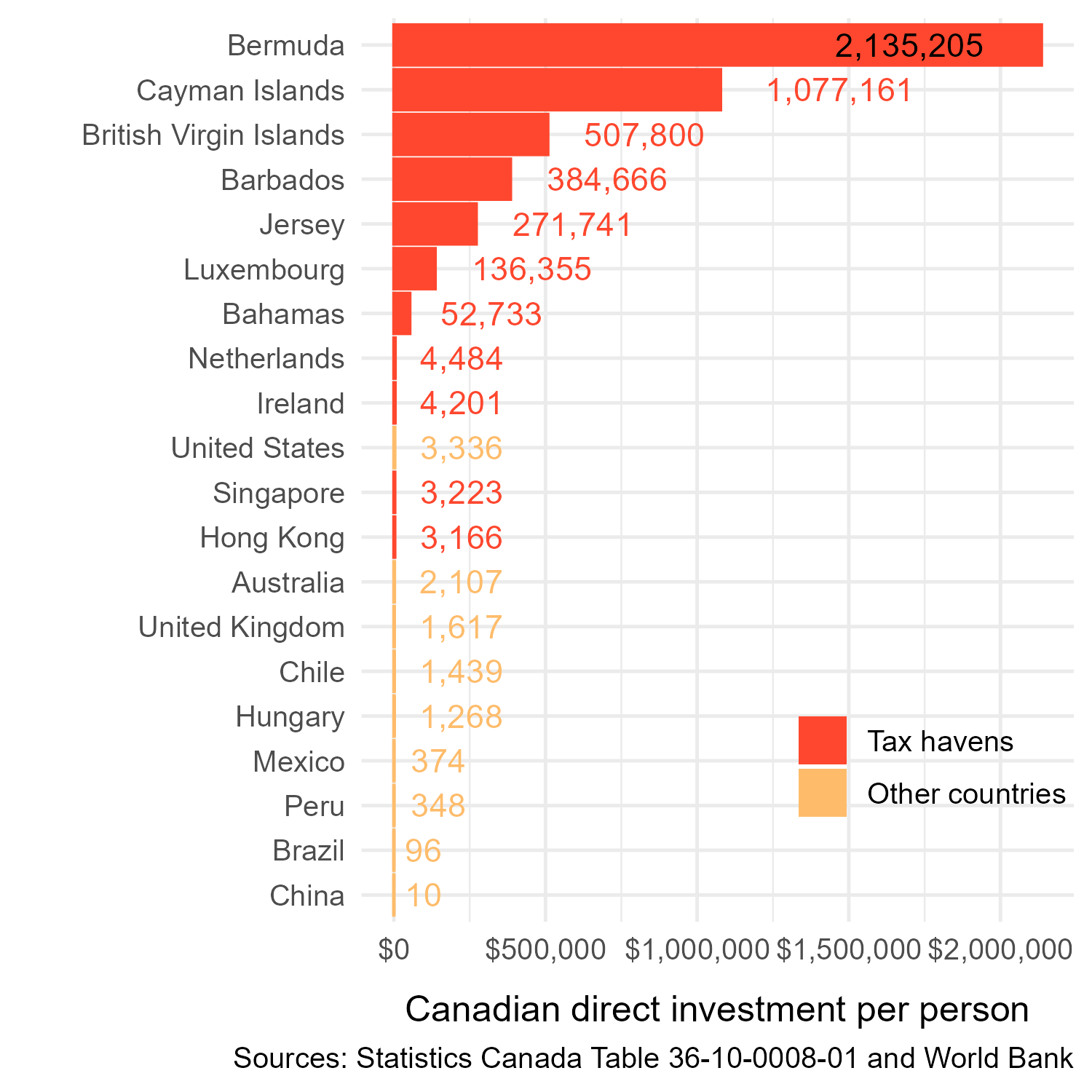

One way to assess whether investment is “real” or purely financial is to look at investment per capita. If the level of assets owned by Canadians in a country is completely disproportionate to the population of a country, it is likely that much of the investment is for purely financial purposes. A good benchmark for what a reasonable level of real investment per capita looks like is Canada’s level in the United States, Canada’s closest trading partner. It is highly unlikely that Canada would own significantly more real assets per person in small nations with little natural resources than in the US.

Figure 3 shows Canadian investment per person in each of the top 20 countries in which Canada has foreign investment (11 of which are tax havens). In the United States, where it makes sense for Canadians to own a lot of assets, Canada has $3,336 of investment per US resident. In other closely allied countries like the United Kingdom and Australia, Canada has $1,617 and $2,107 of investment per resident, respectively.

Figure 3. Canadian direct investment per person in top 20 countries, 2023.

Let’s compare that to Canadian investment per person in tax havens. In Luxembourg, a well-known European tax haven, Canada has $136,355 per resident. In Barbados, Canada has $384,666 per resident. And in Canada’s newest favourite tax haven, Bermuda, Canada has a whopping $2,135,205 in investment per resident. That’s as if every Bermudan resident rented a luxury home in Bermuda from a Canadian.

It is simply not possible that Canada has invested so much in real assets in Bermuda. Indeed, Brookfield’s investment in Bermuda is clearly little more than a PO box above a bike shop. Canada’s elevated level of assets in Bermuda and all the tax havens in which Canada has absurd levels of investment per person have more to do with avoiding taxes than any form of real investment.

The use of tax havens by large corporations in Canada

Among the corporations listed on the TSX 60 (an index of 60 of Canada’s largest corporations on the Toronto Stock Exchange), at least 46 have subsidiaries in tax havens. Brookfield Corporation leads the way with 44 subsidiaries identified in tax havens. These figures are likely underestimates since they are based on incomplete lists of subsidiaries. Corporations do not have to disclose all subsidiaries publicly due to a continued lack of transparency. For example, companies must report subsidiaries that meet certain size thresholds in annual reports but can choose to omit smaller subsidiaries. Clearly, the use of tax havens has become common practice among Canadian multinational firms.

In 2024, companies listed on the TSX 60 avoided $7.0B in taxes due to foreign tax rate differences. All of these taxes avoided were among the 46 companies that have at least one confirmed subsidiary in a tax haven. Unfortunately, because corporations are not forced to publish their financial statements on a country-by-country basis, we cannot say precisely how much of these taxes were avoided through tax havens in particular. Given that all of the avoided taxes were in companies with confirmed subsidiaries in tax havens, however, it is safe to say that a significant portion of this revenue was lost through the use of tax havens, including subsidiaries set up for the express purpose of reducing taxes.

Table 1. Taxes avoided by TSX 60 due to foreign tax rate differences, 2024.

|

Group |

Total profits ($M) |

Statutory tax rate |

Change in ETR due to foreign tax rates |

Reduction in taxes due to foreign tax rates ($M) |

|

TSX 60 with subsidiary in tax haven |

158,960 |

27.0% |

-5.1% |

-7,040 |

|

TSX 60 without subsidiary in tax haven |

35,940 |

24.5% |

0.3% |

50 |

|

TSX 60 |

194,900 |

26.5% |

-4.5% |

-6,990 |

Note. Corporations listed on the TSX 60 as of May 2025 are included. Four companies are excluded from these calculations - Brookfield Asset Management, Brookfield Infrastructure Partners, and Loblaws because they are subsidiaries of other companies on the TSX 60, and Canadian Apartment Properties REIT because it is not subject to corporate income tax in Canada. Figures rounded to the nearest $10 million. All figures reported in CAD. Where financial statements were in USD, figures have been converted to CAD at the average exchange rate in 2024 from the Bank of Canada, 1.3698.

On average, companies on the TSX 60 face a statutory corporate income tax rate of 26.5%. Yet, TSX 60 companies were able to lower their effective tax rate (the proportion of profits they are actually obliged to pay in taxes; ETR) by 4.5 percentage points through foreign tax rate differences. Among companies with a confirmed subsidiary in a tax haven, this was even higher, at 5.1 percentage points.

Loblaws created a Barbados bank to avoid millions in taxes

Loblaws has been known for price-gouging Canadians through the bread price-fixing scandal and doubling their profit margins during the COVID-19 pandemic. Although they have not publicly reported any current tax haven subsidiaries, they did use a Barbados subsidiary to avoid paying Canadian taxes for decades.

In 1992, Loblaw Financial Holdings, part of Galen Weston’s corporate empire (we’ll call it Loblaws for simplicity), opened a subsidiary offshore bank in Barbados, licensed by the Central Bank of Barbados under the name of Glenhuron Bank Ltd. Over the following decade, other Loblaws companies made sizable investments into Glenhuron. In 2013, Loblaws dissolved Glenhuron to use its assets to fund an acquisition.

Glenhuron used the funds provided by Loblaws to buy debt securities, manage assets, and perform interest and cross-currency swaps. Under Barbados law, Glenhuron’s tax rate would have been from 1-2.5%. Canadian tax law dictates that investment income from subsidiaries abroad is taxable in Canada unless the subsidiary qualifies as a foreign bank. In order to qualify for this exemption, the subsidiary must conduct business primarily with entities that are not affiliated with its parent company.

The Government of Canada argued that Glenhuron Bank’s business was indeed primarily conducted with entities affiliated with Loblaws and, as such, demanded that Loblaws include Glenhuron’s income in its taxable income, meaning it would owe over $100 million in taxes.

After a lower court had agreed with the Government, the Supreme Court ultimately sided with Loblaws, arguing Glenhuron’s primary business was conducted with persons that were at arm’s length from Loblaws because its income-earning investments were not in Loblaws (even though the vast majority of its funds came from Loblaws). This ruling essentially makes it legal for Canadian companies to set up subsidiary banks in tax havens to manage their investment assets to lower their tax rate – had Glenhuron been set up in Ontario, where Loblaws is headquartered, its investments would have been subject to the combined provincial and federal corporate income tax rate, today 26.5%.]

The companies that avoided the most taxes through foreign tax rate differences are Canada’s largest financial institutions – Canada’s big five banks, and three of the largest four insurance companies are all among the top 10, listed in Table 2. Canada’s large banks have long been dominant in the Caribbean and even helped establish many Caribbean countries as tax havens (see section “How did we get here?”). Certainly, some of the banks’ assets in the Caribbean are “real” in the sense that they provide banking services in these countries, but by allowing their tax haven subsidiaries to be taxed at much lower rates, Canadian law provides an incentive for them to shift income generated in Canada to their Caribbean subsidiaries.

Table 2. 10 TSX 60 corporations that avoided the most taxes through foreign rate differences in 2024.

|

Corporation |

# confirmed subsidiaries in tax havens |

Pretax income |

Statutory tax rate |

ETR |

Change in taxes due to differences in foreign tax rates |

|

Royal Bank of Canada |

8 |

19,900 |

27.7% |

18.2% |

-1,970 |

|

Manulife Financial |

11 |

7,090 |

27.8% |

17.1% |

-940 |

|

Bank of Nova Scotia |

7 |

9,920 |

27.8% |

20.5% |

-750 |

|

Bank of Montreal |

3 |

9,540 |

27.8% |

23.2% |

-360 |

|

Power Corp of Canada |

6 |

5,530 |

26.5% |

16.8% |

-360 |

|

Restaurant Brands International Inc |

14 |

2,480 |

26.5% |

20.1% |

-310 |

|

Canadian Imperial Bank of Commerce |

16 |

9,170 |

27.8% |

21.9% |

-280 |

|

Toronto-Dominion Bank |

9 |

10,830 |

27.8% |

24.8% |

-270 |

|

Sun Life Financial |

4 |

4,340 |

27.8% |

24.0% |

-250 |

|

Thomson Reuters |

10 |

2,070 |

26.5% |

-5.9% |

-240 |

Note. Dollar values rounded to the nearest $10 million.

The Royal Bank of Canada alone, which has subsidiaries in the Bahamas, Barbados, the Cayman Islands, Delaware, and Luxembourg, avoided $1.97B in taxes through foreign rate differences in 2024. One of their Cayman Islands subsidiaries is called “Investment Holdings (Cayman) Limited”. The name itself suggests that, rather than providing any real services or products in the Cayman Islands, the subsidiary exists to hold investments. RBC’s website displays a Canadian telephone number next to its Cayman Islands Branch Director, an individual whose location on LinkedIn is in Canada. In addition to using tax havens to avoid its own taxes, RBC has been accused of helping clients set up accounts in tax havens to avoid taxes. While perfectly legal under Canadian law, we must ask ourselves whether it should be legal for Canadian corporations to set up holding companies in tax havens to reduce taxes for themselves and their clients.

How does Canada’s tax system allow this?

Canada’s tax system makes the use of tax havens to reduce Canadian taxes legal. The main loophole that allows for exploitation is the taxation of dividends received by Canadian corporations from foreign subsidiaries. Active business income of the foreign subsidiary can be returned as dividends paid to the Canadian parent corporation without being subject to tax so long as Canada has a tax agreement with the foreign country. This provides a huge incentive for firms to shift profits to countries that have corporate tax rates lower than Canada’s (roughly 26.5%).

In theory, the lower tax rate in a foreign country should only be available to a subsidiary of a Canadian corporation if it is actively conducting business there – meaning it has employees, machinery, and is producing a product. Otherwise, income from foreign subsidiaries is treated as passive income and subject to Canadian tax in the year it is accrued. However, with the assistance of large accounting firms, companies have used many complex tax planning schemes to divert income earned in other jurisdictions through tax havens so that it can be counted as active business income in a tax haven.

For example, there is the intra-group debt strategy whereby capital is loaned without interest to a subsidiary in a tax haven, which then loans it at high interest rates to a Canadian subsidiary carrying out real economic activity. The interest payments to the foreign subsidiary are recorded as profit, wiping out the subsidiary doing the real economic activity’s taxable income. So long as Canada has a tax agreement with the country hosting the foreign subsidiary, the foreign subsidiary can then pay dividends to the Canadian parent company tax-free. Quebec’s Institute for Socioeconomic Research and Information (IRIS) has documented that Cenovus Energy used this strategy to shift $1.6B in profits to Luxembourg.

Using artificially low transfer prices is another strategy that can get around these rules. Transfer prices are prices of goods or services sold between related parties (e.g., a parent company and its subsidiary). By law, such transactions must use the same prices as if those goods or services were sold on a market. But for many types of goods and services traded between related parties, there is no market, leaving companies huge latitude to set the price that will allow them to shift profits to lower tax jurisdictions.

Wheaton Precious Metals, a company that purchases secondary minerals sourced from mines primarily owned by other companies and sells them at market prices, uses transfer pricing to allocate its profits to a subsidiary in the Cayman Islands. The CRA reassessed Wheaton for transfer mispricing in 2015, asking them to pay $353M in unpaid taxes and penalties, yet ended up reaching a settlement with the company in 2018 that resulted in only $11.4M in taxes and penalties. As of 2024, the company did not have any contracts for minerals from the Cayman Islands, yet it booked all of its net earnings there, totalling $1.04B (its total net earnings were only $725M, meaning it recorded a net loss in other jurisdictions). This demonstrates the complete failure of existing laws to address the problem.

Canada has a law called the General Anti-Avoidance Rule (GAAR), which, in theory, is intended to prevent activities like transfer mispricing and intra-group debt that result in tax avoidance. However, courts have historically interpreted the GAAR very narrowly, only enforcing it when a particular rule in the Income Tax Act was “abused”. If there was no particular rule that was violated, the GAAR does not apply. This has historically allowed companies huge latitude to structure transactions to minimize taxes.

In 2024, there was an update to the GAAR to strengthen it. The updated rule lowers the bar for transactions to be blocked under the GAAR. However, it is far less stringent than advocates were calling for. It leaves a lot of room for interpretation, and it remains to be seen how it will be interpreted by the courts. At this point, it seems likely that a lot of tax avoidance transactions will still be permissible under the new regime. It still places the onus on the government to prove that a transaction abused the Income Tax Act rather than on corporations to prove a business reason to use a subsidiary in a tax haven.

A better solution that has been suggested by tax experts is to use a tax credit system rather than a blanket exemption from taxation for foreign dividends. Importantly, a tax credit system is how personal income is typically taxed under tax treaties. Under most of Canada’s tax treaties, if someone earns employment income in a foreign country and pays tax on it there, they receive a tax credit against their taxes payable in Canada, but they are not exempt from paying income tax in Canada. For example, if someone earned $50,000 abroad and paid $5,000 in foreign income tax, they would receive a $5,000 tax credit, reducing their Canadian tax payable from $6,684 to $1,684. But the individual would still have to pay $1,684. This system applied to corporations would provide a tax credit for foreign taxes paid on business income returned to Canada as dividends but still require the difference to be paid.

How did we get here?

Recent research from IRIS argues that the use of tax havens has been normalized in the public sector in Canada. 20% of corporate directors of Canadian corporations that practiced tax avoidance through Luxembourg held positions in the public or parapublic sector at other times in their career. This includes high-level positions, including the Governor General and provincial ministers.

The tight link between government and corporate tax avoidance is not new. In the 19th century, Canadian bankers had enormous political power in Canada and were able to secure extremely lax banking regulations. This proved immensely useful for imperial investors. As the British and Americans expanded into the Caribbean in the 19th century, Canada’s lax banking regulations and alliance with both imperial projects made Canada’s banks a top choice to funnel investment into the Caribbean. Where American banks were tightly regulated, Canada’s had minimal regulatory oversight and were subject to little taxation. This led to Canadian banks (especially those that became the Bank of Nova Scotia, CIBC, and RBC) dominating banking in the British colonies in the Caribbean.

Many of these colonies are today Canada’s favourite tax havens. In fact, three of Canada’s top four and five of Canada’s top 11 tax havens are present or former British colonies in the Caribbean. Among the 15 defined as tax havens in this report, three more are small islands that are currently British Crown dependencies, and two more were British colonies until 1959 (Singapore) and 1997 (Hong Kong).

Canada played a huge role in establishing these British colonies as today’s tax havens. Post-World War Two, the creation of the eurodollar market led to an excess of capital in Europe looking for places to invest. With many Caribbean islands still under British imperial control and relatively underdeveloped, they were a top target for this excess investment. Canadian banks exploited their dominant role in the region to facilitate these deals. Canadian lawyers and bankers then used their powerful positions to ensure local banking laws and corporate taxes were extremely favourable to foreign investment. In the Cayman Islands, building on tax haven models already established in the Bahamas, Calgary lawyer Jim Macdonald “deftly turned the Caymans into the region’s preeminent tax haven.”

Canada’s excessive use of Caribbean tax havens today is not so surprising when viewed in this historical context – Caribbean tax havens were set up by wealthy Canadians to benefit themselves. Rather than a new frontier, then, the 1980 signing of a tax treaty which permitted Canadians to register assets in minimal-tax Barbados and then return them to Canada tax-free was merely the latest formalization of Canada’s long-standing facilitation of tax avoidance in the Caribbean.

It was immediately evident that tax treaties with tax havens would lead to tax avoidance, as raised by Bob Rae in the House of Commons in 1980. By 1992, the Auditor General had pointed out that Canada was losing hundreds of millions in tax revenue because of these treaties. Despite these warnings, tax treaties became even more central to Canada’s use of tax havens in the 1990s when Paul Martin changed the law so that dividends from foreign subsidiaries were tax-exempt in Canada only if Canada had signed a tax treaty with that country. This was extended to include tax information exchange agreements in 2009.

Since then, Canada has continued to sign tax agreements that allow corporations and the wealthy not to pay taxes when returning income to Canada, even when the other country does not tax that income abroad. Canada currently has a tax treaty or a TIEA with all 15 of Canada’s top tax havens. Many of these were signed as recently as the 2010s under Stephen Harper and do little aside from allowing multinational corporations to avoid taxes. As Alain Deneault puts it, “The government has legalized [tax haven] use even though it clearly violates the spirit of the law.”

The OECD/G20 Base Erosion and Profit Shifting process

In 2013, the G20 tasked the OECD with developing a plan to combat “base erosion and profit shifting” (BEPS) – in other words, tax avoidance through the use of tax havens. The OECD was well placed to combat this problem – because it played an integral role in creating the existing international taxation regime that led to tax avoidance. The OECD is an international organization developed by rich countries which has long played a role in developing regulations for international investment. For example, the tax treaties and TIEAs that Canada has signed with other countries are based on OECD model treaties. It was under pressure from the OECD to sign TIEAs that the Harper government extended the favourable tax treatment of foreign dividends to countries with which Canada had TIEAs.

The OECD embarked upon the BEPS initiative to address the tax avoidance problem it itself had helped to create. By 2015, they had developed a 15-point action plan to address the problem through domestic policy changes and changes to bilateral treaties. This resulted in a multilateral convention in 2017 that has been signed by over 100 countries – notably, however, the United States is absent from this list. Today, all 15 top tax havens have signed on to agreements on the automatic exchange of tax information and country-by-country reporting for multinationals, meaning the TIEAs signed under Harper have little further purpose.

In 2021, the OECD/G20 BEPS process resulted in a new agreement with two key pillars. Pillar One concerned the allocation of taxing rights of companies that operate in several jurisdictions. However, in part due to resistance from the US, agreement on implementation of this Pillar was never achieved, and it has yet to be implemented. The failure of this process is one reason Canada implemented a Digital Services Tax in 2024.

Pillar Two was intended to end the race to the bottom on corporate taxation by implementing a global minimum corporate tax rate. Yet, despite the Independent Commission for the Reform of International Corporate Taxation’s recommendation of a minimum 25% rate and Biden’s push for a 21% minimum rate, Pillar Two ended up suggesting only a 15% minimum corporate tax rate. Moreover, the rules leave out companies with less than 750 million euros (about $1.2B CAD) in annual income, many investment companies, and provide a “substance-based” carve-out for companies with employees or tangible assets in a given jurisdiction. Rather than preventing the use of tax havens, the EU Tax Observatory has argued that this last loophole actually incentivizes companies to move to tax havens.

Unlike Pillar One, Pillar Two has been implemented in 54 countries, including Canada, through the Global Minimum Tax Act. It has also been implemented in many of Canada’s favourite tax havens, including Bermuda and Barbados. The Cayman Islands, notably, has no plans to implement Pillar Two. The implementation of Pillar Two has resulted in increased tax revenue in Canada and foreign countries from some Canadian multinationals starting in the 2024 tax year. However, the weak rules continue to provide massive incentives for profit shifting. First, there is still a massive gap between Canada’s roughly 26.5% corporate income tax rate and the 15% that will be applied in most tax havens. Second, the loopholes for tax credits and the carve-out for “substance-based” economic activity in a jurisdiction will allow multinationals to lower their effective tax rate below 15% in tax havens while Canada’s tax agreements with them continue to allow them to return their profits to Canada tax-free. Third, smaller corporations and most investment firms will be completely untouched by these rules. So, while the Global Minimum Tax Act was an important step in the right direction, it will by no means end corporate Canada’s use of tax havens.

Conclusion and recommendations

Canada’s use of tax havens today is the result of decades of favourable policy towards large corporations and the wealthy. Recent changes to the GAAR and the implementation of the Global Minimum Tax Act will help but fail to address the root of the problem. This was acknowledged during the 2025 federal election when several parties put forward plans to address the use of tax havens. The Liberals, led by Prime Minister Carney, who helped facilitate tax avoidance through Bermuda at his previous employer, Brookfield, were the only major party that failed to address the issue. Now, we call on the government to take the following measures to end the international tax avoidance that disproportionately benefits the wealthy at the cost of our public services:

- End tax agreements with known tax havens. Canadian companies should not be allowed to use tax havens to make their profits earned in Canada tax-free. Ending tax agreements with countries that use low tax rates and lax regulations to entice companies would ensure dividends from foreign subsidiaries would not be tax-exempt. These agreements incentivize multinationals to shift profits to tax havens with no benefit for Canada. In the long run, Canada could implement a tax credit system, as opposed to its current exemption system, for profits returning to Canada from foreign subsidiaries.

- Require corporations to have a genuine business reason to open foreign subsidiaries. Canada must update its laws to put the onus on corporations to prove that their use of foreign subsidiaries is needed to produce goods and services. Existing laws have proven time and again to be insufficient to prevent tax avoidance.

- Support the UN tax convention process. Canada must stop inhibiting the democratic process to create an international tax convention through the UN. Instead, it should embrace this process and encourage others to support a truly democratic international convention that eliminates incentives for profit shifting and ensures the ultra-wealthy are taxed effectively.

- Increase transparency in financial reporting. Countries that have implemented the recommendations of the OECD BEPS process now require companies to submit country-by-country breakdowns of their financial information to tax authorities. This information is crucial for identifying companies that engage in profit shifting and taking action to prevent it. However, unlike the EU countries, Canada has not made this information publicly available.

Send a message to Ottawa to shut down tax havens here!