Summary

- Canadian corporations pay so little tax that less than one week of revenues covers all their income taxes for the entire year.[i]

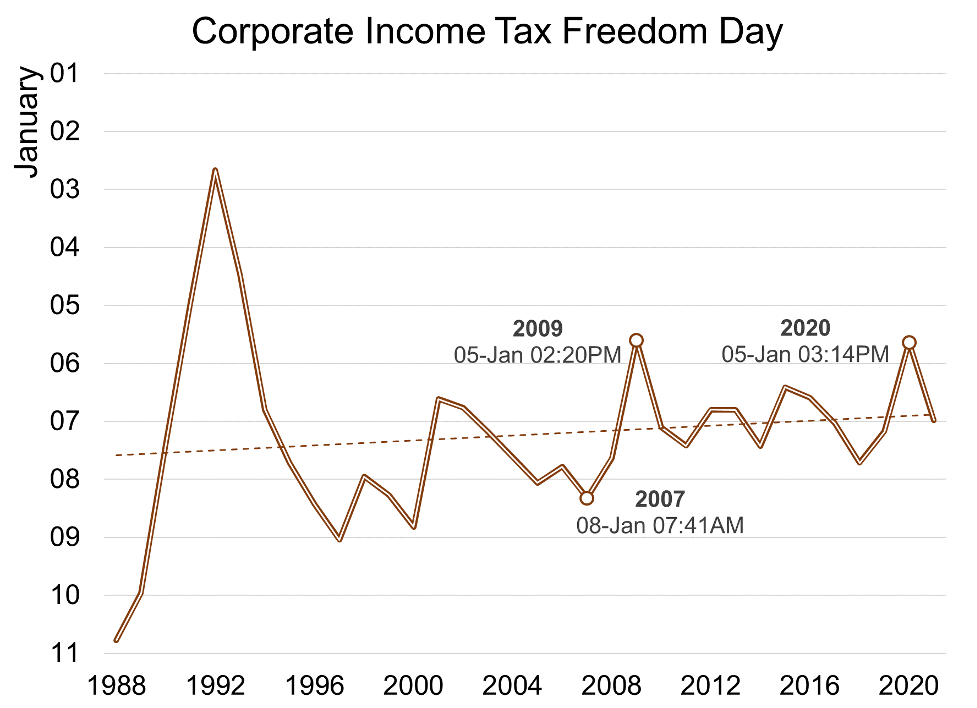

- Corporate Income Tax Freedom Day is coming earlier and earlier every year because corporate tax rates keep going down.

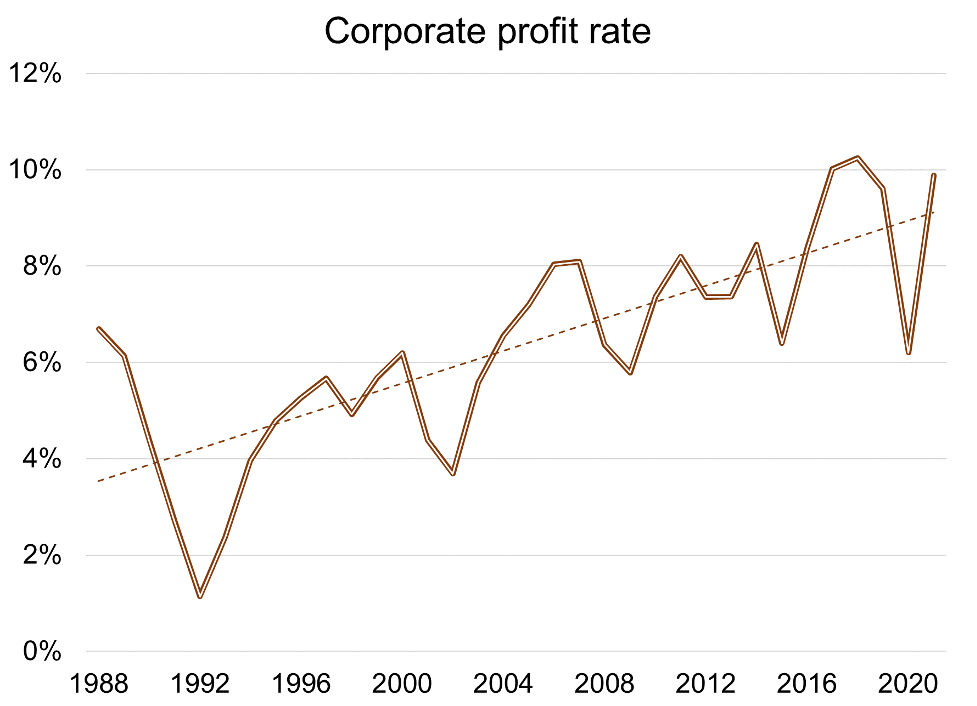

- In 2021, corporations enjoyed their lowest ever recorded income tax rate, despite having their third highest recorded profit rate, thanks in part to over $100 billion in federal pandemic support that found its way into corporate coffers.

- Falling corporate tax rates are the product of reductions in statutory rates as well as the use of tax loopholes and havens. This has shifted $1.1 trillion dollars from governments to corporations over the last two decades.

- Increased revenue from higher corporate taxation will a) recover public money accumulated by corporations during the pandemic, and b) improve the fiscal situation for all governments.

What is “Corporate Income Tax Freedom Day”?

Corporate Income Tax Freedom Day is the date on which Canadian corporations have accumulated the last tax dollar they will need to pay all of their taxes for a given year. Regular families pay a couple of months of income to governments for our healthcare, education, infrastructure, public services, and more. Despite relying on goods and services from Canadian governments, corporations are able to take advantage of low tax rates, tax havens, and tax loopholes, to cover their income tax costs in less than one full week! That’s why they get to celebrate Corporate Income Tax Freedom Day so early.

Report

Introduction

At 12:33am on January 7, Canadian corporations collected the last dollar needed to pay their annual corporate income tax bill.[ii]

Since 2010, Corporate Income Tax Freedom has arrived, on average, by 2:19am on January 7. However, the time has been trending earlier and earlier with corporations keeping an additional half hour or so of revenue each year. This trend is a direct result of falling corporate income tax rates and widespread use of tax loopholes, tax havens, and aggressive corporate accounting.

The pandemic brought an unprecedented level of government support for workers, families, and businesses that helped maintain corporate revenues and kept corporations flush with cash. In 2020, the pandemic also brought an extraordinary reduction in corporate taxes due to a decline in profits. It must be emphasized, however, that this decline was from record high levels. In 2021, corporate profits rebounded while corporate taxes did not.

Corporate Income Tax Freedom Day in 2020 and 2021 were both earlier than the recent average. Will 2022 be part of a new trend of Corporate Income Tax Freedom Day coming even earlier?

Why is Corporate Income Tax Day coming earlier?

The corporate profit rate has been trending upward since the mid-1990s. If the effective tax rate had remained the same, Corporate Income Tax Freedom Day would move later and later. In order to achieve earlier tax freedom, while also pushing up profit rates, corporations had to reduce their effective income tax rate.

Falling effective tax rates are the result of both reductions in the statutory rate and the increasingly sophisticated forms of tax avoidance used by corporations.

Why are low effective tax rates a problem?

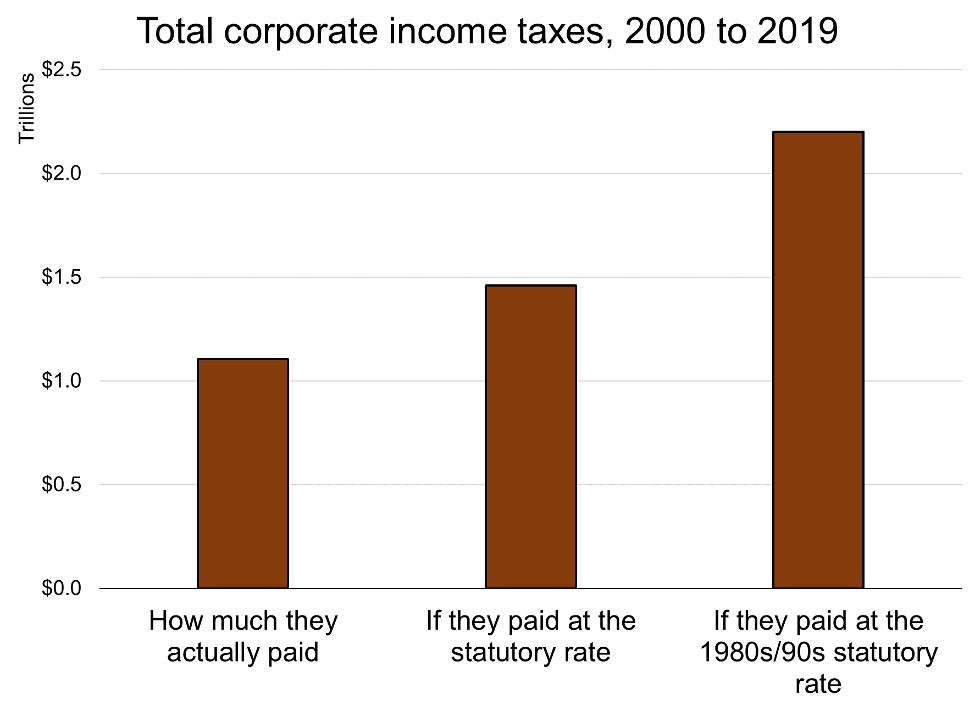

Most obviously, falling corporate tax rates deprive governments of revenue. The average statutory corporate income tax rate through the 1980s and 90s was 48%.[iii] If corporations had paid taxes at that rate for the last two decades, governments would have brought in an additional $1.1 trillion in revenue. Even if corporations had just paid at the actual statutory rate, governments would have collected $353 billion more.

DATA: Income taxes paid: Statistics Canada table 33-10-0007-01; Statutory tax rates: Finances of the Nation.

Proponents of corporate tax cuts claim that greater investment and jobs will follow. However, investment in productive assets by non-financial corporations has declined since at least 1990, even as taxes were cut. Rather than increased investment in productivity, savings from corporate tax cuts were fed into corporate cash pools, executive salaries, and distributions to shareholders.

During the pandemic, the trend of rising cash holdings was kicked into overdrive. Non-financial corporations have increased their cash-holdings by almost $200 billion. We estimate that at least $123 billion of that is from money injected by the federal government.

Rising corporate profit rates make everyday goods and services more expensive for households. A falling corporate tax rate increases the cost to households of government goods and services. Additionally, because corporate ownership is highly unequal, rising profits and falling corporate taxes exacerbate income and wealth inequality.

As concern about federal debt mounts, it is important to identify where the dollars put into the economy are ending up. Too many of them have settled in corporate coffers. This accumulation is not the result of socially-beneficial productivity and innovation. It is primarily the result of our trickle-up economy. Asset owners, simply by virtue of their ownership, syphon money out of the economy in the form of interest and profits. This can then be used to further increase their outsized asset ownership.

It is tempting to blame the corporations for this situation. However, they are simply taking advantage of a potent combination of misguided corporate tax policy and the government’s failure to close loopholes. Canada should follow the lead of our largest trading partners, the US and UK, which are moving to increase their corporate tax rates. Canada should also be leading at the OECD, which is looking at ways to stop international corporate tax dodging.

Reversing the long-term downward trend in corporate taxation does more than just increase the revenue of governments. It is a way to keep corporations accountable to the public. Corporations benefit from much government support. That support demands a high degree of transparency and accountability.

Measures that would help reverse these harmful trends include:

- A pandemic excess-profits tax

- Restoring the federal corporate income tax rate from 15% to 20%

- A minimum tax on profits recorded in foreign jurisdictions

- Greater investment in the Canada Revenue Agency

- Improved transparency, which can be achieved with a) public country-by-country reporting of corporate financials, including taxes paid; and b) a public beneficial ownership registry[iv]

- Closure of widely abused loopholes and tax avoidance schemes

Explainer: Taxing profits, analyzing revenues

Canadian corporations are taxed on their profits, rather than their revenues. However, there are a number of reasons for examining taxes as a share of revenue:

1. Taxes as a share of revenue is more comparable to the tax rate paid by households, which do not get to deduct most of their essential expenses.

2. Corporations depend on the goods and services that governments provide, and therefore, taxes should be considered an essential expense.

3. It is common practice to analyze the ratio of various corporate financial values to revenue. Because corporate revenue is used to cover different types of expenses—such as interest or pension obligations—a corporation’s ability to cover those expenses can be assessed by examining costs as a share of revenue.

4. It is harder to disguise or shift revenue via loopholes and tax havens than it is to shift profits. This is why revenue will be the tax base used for the planned digital services tax, which is intended to ensure that transnational digital giants are not able to escape paying taxes in Canada.

CORPORATE INCOME TAX FREEDOM DAY COMES EARLIER AND EARLIER

The date and time when corporate revenues cover the tax bill has been trending earlier since the late 1980s. From 1988 until 2009, Corporate Tax Freedom came, on average, by 9:37am on January 7. For 2010 to 2019, corporate income taxes were typically covered more than seven hours earlier at 2:19am. The last time it took over one week for corporations to gather enough revenue to cover their taxes was 2007.

Note that higher points are earlier. DATA: 1988-2019: Statistics Canada table 33-10-0007-01; 2020-1: Statistics Canada tables 33-10-0225-01, and 33-10-0227-01.

2020 had the earliest Corporate Income Tax Freedom Day since 2009, with the last dollar needed coming into corporate coffers at 3:14pm on January 5. The pandemic was an obvious factor, since it lowered total profits, which lowered taxes paid. Data for the first three quarters of 2021 show that Corporate Income Tax Freedom was likely achieved at 11:32pm on January 6.

If 2022 returns to the pre-pandemic trend, corporations will have collected the last tax dollar at 12:33am on January 7. However, if the pandemic performance has kickstarted a new trend, then corporations will have covered their meagre tax responsibilities almost four hours earlier, at 8:34pm on January 6.

How do we calculate when Corporate Income Tax Freedom Day falls?

Corporate Income Tax Freedom Day is calculated from the ratio of corporate income taxes paid (CIT) and operating revenue (SALE). This ratio can be expressed as the product of the corporate profit rate—profits (PROFIT) as a share of revenue—and the effective corporate income tax rate—income taxes as a share of profits.

Therefore, Corporate Tax Freedom Day will be later if either the profit rate or the effective tax rate increases, while the other term remains the same. Conversely, if either term falls, while the other remains the same, Corporate Tax Freedom Day will be earlier. (The CIT/SALE ratio is converted to a date and time as a percentage of 365.25.)

THE CORPORATE PROFIT RATE IS INCREASING

Corporate Income Tax Freedom Day is the product of a corporation’s profit rate and its effective tax rate.[v] The corporate profit rate has been trending upward for decades. While the pandemic resulted in a lower profit rate in 2020, its impact was surprisingly small given the scale of economic calamity caused. In 2021, the corporate profit rate rebounded to 9.9%, its third highest recorded level.

DATA: 1988-2019: Statistics Canada table 33-10-0007-01; 2020-1: Statistics Canada tables 33-10-0225-01, and 33-10-0227-01.

In 2017 and 2018, the Canadian corporate profit rate exceeded 10% for the first and second time on record, dipping slightly to 9.6% in 2019. The pandemic pushed margins down to 6.2% in 2020, the lowest level since 2009. However, this rate only appears low in the context of the recent highs. From 1988 to 2009, the average profit margin was 5.3%. Even if we exclude the extraordinarily low years of 1991 to 1994, the average was still just 5.8%. Despite a once-in-a-lifetime global economic shock, the 2020 profit margin was still the 9th highest over the 34 years analyzed.

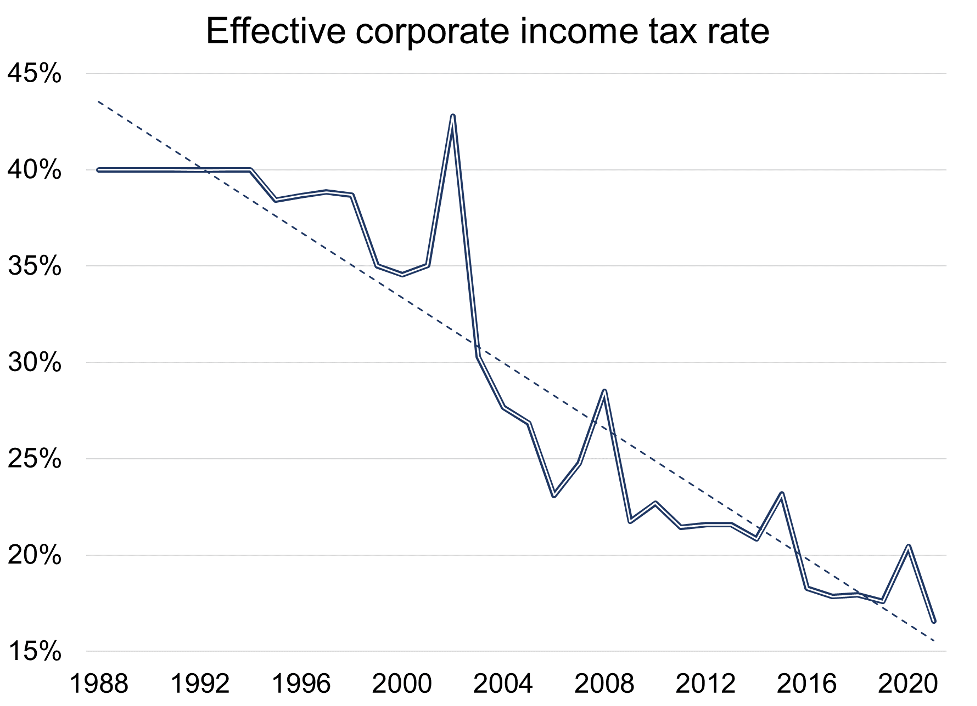

THE CORPORATE INCOME TAX RATE IS DECREASING

Corporations have been astoundingly successful at driving down their tax rates at the same time as they push up their profit rates. Pandemic-lowered profits caused the effective tax rate to jump slightly.[vi] However, this was promptly reversed and the effective corporate income tax rate for 2021 is set to hit a record low of just 16.6%.[vii]

DATA: 1988-2019: Statistics Canada table 33-10-0007-01; 2020-1: Statistics Canada tables 33-10-0225-01, and 33-10-0227-01.

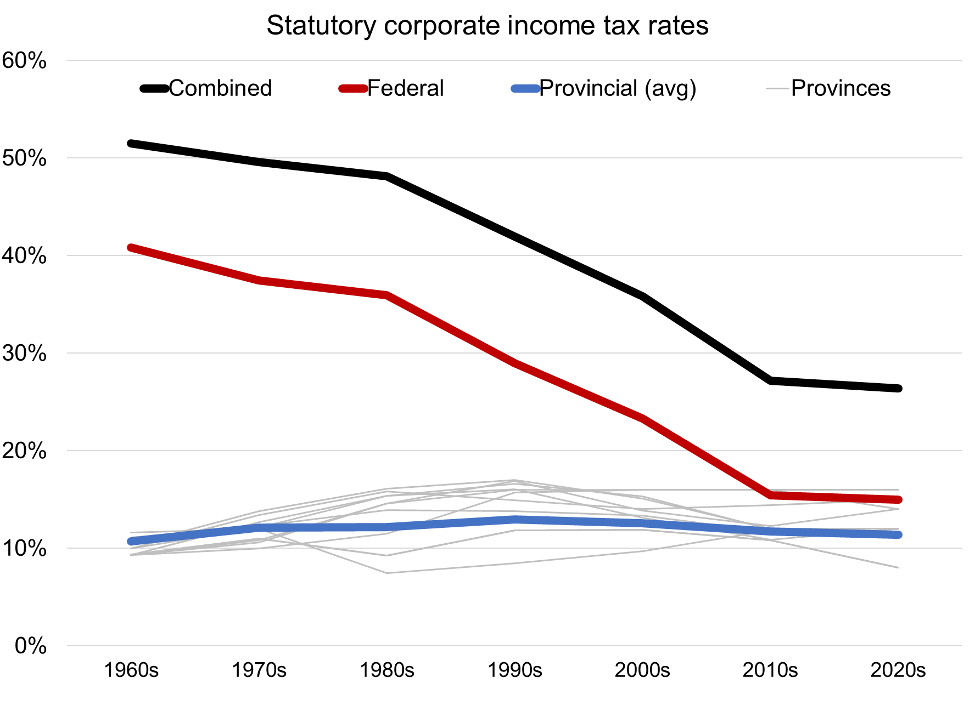

Corporations have benefitted from provincial and federal governments lowering statutory corporate income tax rates. The federal government has significantly reduced its rate since the 1960s. One justification for the reduction was to provide tax room for the provinces. However, while some provinces initially took advantage, most have since lowered their own statutory rates (visible in the light gray lines on figure below, ‘Statutory corporate income tax rates’. The result is a near halving of the combined average federal and provincial rate from 51.51% in the 1960s to an all-time low of 26.38% in 2020 and 2021.[viii]

What is the difference between statutory and effective tax rates?

Statutory tax rates are the rates set by government statute. For example, the statutory federal corporate income tax rate is currently 15%. However, most taxpayers—individuals and corporations alike—are able to lower their taxes with various kinds of credits, preferences, and exemptions. The effective tax rate is taxes paid as a percentage of income. For example, if a corporation had profits of $1 million, at the statutory federal rate they would owe $150,000. However, let’s say they get a $50,000 tax credit for research and development and only pay $100,000. That would make their effective federal tax rate just 10%.

If, for the last two decades, corporations had paid the average statutory income tax rate that prevailed through the 1980s and 1990s, Canadian governments would have collected an additional $1.1 trillion in revenue. To put this in perspective, that is more than the total amount of money given to the provinces through the Health and Social Transfer over the same two-decade period.

Corporations rarely actually pay the statutory amount of tax. First, governments provide numerous tax preferences, exemptions, and credits that allow corporations to reduce their tax bill. Second, through the use of increasingly sophisticated tax schemes that create and exploit loopholes, they are able to further reduce their taxes.

The gap between the statutory tax rate and the rate corporations actually pay has grown at an alarming rate. Through the 1990s, the effective tax rate averaged 7% below the statutory rate. That gap was increased to 18% in the 2000s, with a further increase to 25% in the 2010s. 2020 saw the largest gap on record at 37%. In other words, corporations kept more than one out of every three tax dollars that they would have paid at the statutory rate. This is thanks to both government tax preferences, tax credit handouts, and aggressive corporate tax avoidance schemes.

Table: Canadian Corporate Tax Rate Decline since the 1990s

|

|

Statutory rate |

Effective rate |

Difference |

|

1990s |

42.0% |

39.0% |

3.0pp (7.2%) |

|

2000s |

35.8% |

29.5% |

6.3pp (17.6%) |

|

2010s |

27.2% |

20.3% |

6.9pp (25.3%) |

|

2020 |

26.4% |

20.5% |

5.9pp (22.5%) |

|

2021 |

26.4% |

16.6% |

9.8pp (37.2%) |

Note: The difference is the statutory rate less the effective rate expressed as percentage points (pp). The value in brackets is the difference as a percentage of the statutory rate.

Even if corporations had just paid at the ever-falling statutory rate, government revenues from 2000 to 2019 would have been higher by $353 billion. In other words, of the $1.1 trillion in foregone government revenue, $353 billion is due to corporate tax avoidance with another $741 billion due to tax cuts.

CORPORATE CASH HOLDINGS ARE RISING

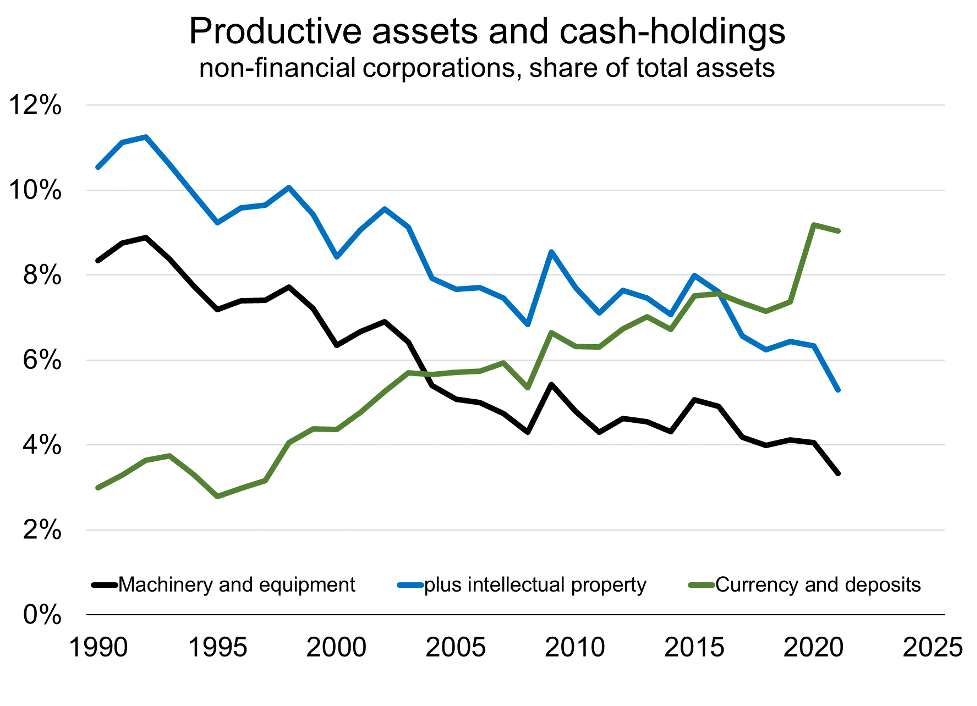

Advocates of cutting corporate income taxes through reduction of the statutory rate, as well as with lucrative tax credits, claim this will entice corporations to invest in productive capacity, creating jobs, and growing the economy. However, at the same time as corporate income tax rates fell over the last 30 years, so did corporate investment in productive capacity.

The share of machinery and equipment within the asset base of non-financial corporations has steadily fallen since 1990. Even if we accept that the economy is increasingly knowledge-based, and include intellectual property among productive assets, investment has still declined significantly. Meanwhile, the cash-holdings of corporations have increased. Tax cuts have gone to increasing the cash holding of large profitable corporations, and not to increasing investment, growing the economy, and creating jobs.

The pandemic has turbo-boosted the cash accumulation of Canadian corporations. In order to financially support Canadians during the economic turmoil of the pandemic, the federal government injected about $365 billion into the economy. Just over half ended up with households. Another one-third found its way into the accounts of non-financial corporations, which caused a 29% increase in their total cash holdings.[ix] While the federal government has begun to reduce the amount of cash it added to the economy, non-financial corporations continue to grow their cash pile. As of the third quarter in 2021, cash holdings by non-financial corporations were 51% higher than two years prior.

CONCLUSION

Corporations depend on public institutions for their existence and their ability to operate. They need a stable financial system, trustworthy macroeconomic information, predictable legal systems, safe and reliable physical infrastructure, a healthy and well-educated public, and much more that we provide or manage through governments. The pandemic put into stark relief this dependence of corporations on governments. Yet, corporations contribute less and less to these essential goods and services. While households provide a couple of months’ worth of income toward public goods and services, corporations provide less than one week’s worth.

Corporate Income Tax Freedom has come earlier and earlier over the last 30 years. This is a stunning accomplishment given the rising corporate profit rate. Corporations could only achieve this by pushing governments to lower the effective corporate income tax rate. Both a rising profit rate and falling corporate tax rate are cause for concern.

A higher corporate profit rate ultimately comes at the expense of workers and consumers through wage reductions and/or price increases. As concerns about inflation and affordability mount, the role of corporate profits should be part of the discussion.

The falling effective corporate income tax rate leaves corporations with more money and governments with less. That means governments seeking to keep deficits manageable must either increase taxes on the rest of us or cut important services.

Empowering corporations at the expense of governments would be a problem even if the promise of increased corporate investment in productivity had been fulfilled. But it was not. As governments cut corporate tax rates, and provided lucrative tax credits, corporate investment in productive capacity has declined. Instead, cash piled up, corporations increased their executive compensation even further, and inequality has worsened, as the wealthiest have got even richer from their corporate and business holdings. The pandemic has exacerbated corporate cash hoarding even more.

Instead, we need increased public spending on expanded health care, safe long-term care, affordable housing, sustainable infrastructure, and much more. The multi-decade experiment in cutting corporate taxes has failed, spectacularly. It has not produced its supposed benefits while it allowed corporations to grow more powerful. It has deprived governments of revenue that justified the under-funding of public goods and services.

How should we deal with the problem?

Measures that will help reverse the trend of growing corporate power include:

Create a pandemic excess profits tax. Early high-profile acts of corporate “generosity”—such as the grocery chains’ wage increases for essential workers—turned out to be cynical marketing ploys. Meanwhile, some of those chains have raked in record profits. The Parliamentary Budget Office (PBO) calculated that an excess profits tax for 2020 would generate $7.9 billion in revenue.

Increase in the federal corporate income tax rate to 20%. Provincial governments were unwilling or unable to take advantage of the continually reduced federal rate. The reduced rate has had none of the positive effects its proponents claimed. Ending the tax cutting experiment would add $7.7 billion to federal revenues.[x]

Impose a minimum tax on profits recorded in foreign jurisdictions. Corporations have taken advantage of financial globalization to seek advantageous tax regimes in other countries. The growth of the digital economy has made it even easier for corporations to book profits in low tax jurisdictions. We calculate that Canada could gain $11 billion or more from an international effort to implement a 21% minimum tax on foreign profits.

Increase investment in the CRA. During the most recent election, every party elected to Parliament expressed support for greater CRA funding to deal with tax avoidance by the rich and powerful. The Liberals promised to increase funding by $2.5 billion over four years, for an expected increase in revenue of $12 billion. With near consensus on the importance of increased funding, we expect the government to act quickly.

Improve corporate transparency:

- Disclose country-by-country reporting of financial statements and taxes. Currently, we do not know how much revenue or profit multinational corporations make in Canada, or how much income tax they pay. This information should be made publicly available.

- Create publicly accessible beneficial ownership registry. In order to shelter their wealth, the ultra-rich often create opaque webs of transnational, corporate inter-ownership. A public registry of beneficial ownership will help reduce this form of tax avoidance, with other benefits, including disruption of international networks of terrorism funding.

Close widely abused corporate tax loopholes:

- End double non-taxation agreements with tax havens. Wealthy Canadians and corporations have hundreds of billions in tax-exempt havens. The Department of Finance estimates that exempting non-residents from withholding taxes costs the federal government over $7 billion annually.[xi]

- Monitor the use of intangible assets to shift profits. The increasing importance of digital technologies has facilitated the use of tax havens. Corporations can much more easily shift intangible assets like algorithms and platforms to claim profits in low-tax jurisdictions.

ENDNOTES

[i] Unless otherwise noted, data used in this report comes from Statistics Canada tables 33-10-0007-01, 33-10-0225-01, and 33-10-0227-01. Statistics Canada changed its reporting of this data in 2020, so some caution must be taken comparing data for 1988 to 2019 with the data for 2020 and 2021. However, we are confident that the series used for this report are relatively comparable for our purposes.

[ii] See the box ‘How do we calculate when Corporate Income Tax Freedom Day falls?’.

[iii] This is the combined federal and provincial rate. Data on statutory rates comes from Finances of the Nation (https://financesofthenation.ca/statutory-tax-rates/). See the box ‘What is the difference between effective and statutory tax rates?’.

[iv] The government promised such a registry in the 2020 Budget. Although the registry was mentioned in recent mandate letters given to the ministers of finance and national revenue, the word ‘public’ was notably absent.

[v] The corporate profit rate is ‘profit before income tax’ divided by ‘operating revenue’. The effective tax rate is ‘income tax’ divided by ‘profit before income tax’. The profit margin is ‘profit before income tax’ divided by ‘operating revenue’. For 2020-2021, ‘profit before income tax’ has been relabeled ‘Income or loss before income tax’. Data on income tax for 2020-2021 is ‘current income tax expense’ plus ‘deferred income tax expense’. Deferred income taxes are those booked but not paid. Deferred income taxes are positive when taxes deferred in previous years are paid and exceed the value of newly deferred taxes.

[vi] The effective tax rate is taxes paid as a share of pre-tax income. Pre-tax income, as reported on corporate financial statements, is not exactly the same as the profit values used by tax authorities to calculate taxes owed. That means a sizable decline in pre-tax income will not automatically correspond to a matching decline in income taxes.

[vii] On average, the effective corporate income tax rate over four quarters is 0.3 percentage points higher than the rate over three quarters. Once outlier years with extraordinary fourth quarters are removed (2002, 2008), that figure drops to 0.1 percentage point. Even if the rate for 2021 is 0.3 percentage points higher than the three quarter rate, it will still be the lowest effective corporate income tax rate on record.

[viii] Between 2012 and 2019, the combined rate ranged from 26.41% to 26.94%.

[ix] This figure comes from the National Balance Sheet Accounts (StatsCan Table 36-10-0580-01). It is calculated as the change in currency and deposit liabilities of the Bank of Canada and the federal government between 2019Q4 and 2020Q4, less the change in currency and deposit assets of the federal government. Non-residents and other levels of government collected most of the remainder. The currency injected into the economy by the federal government cannot be fully mapped into the accounts of non-federal sectors because banks can also create currency through the issuance of loans. Typically, Canadian banks hold little currency or deposits as an asset. However, during the pandemic, the banks converted other assets into currency. This liquidity support was provided by the Bank of Canada.

[x] This is calculated using the PBO’s Ready Reckoner tool (http://www.readyreckoner.ca/?locale=en-CA).

[xi] See the Report on Federal Tax Expenditures 2021 (https://www.canada.ca/en/department-finance/services/publications/federal-tax-expenditures/2021.html).